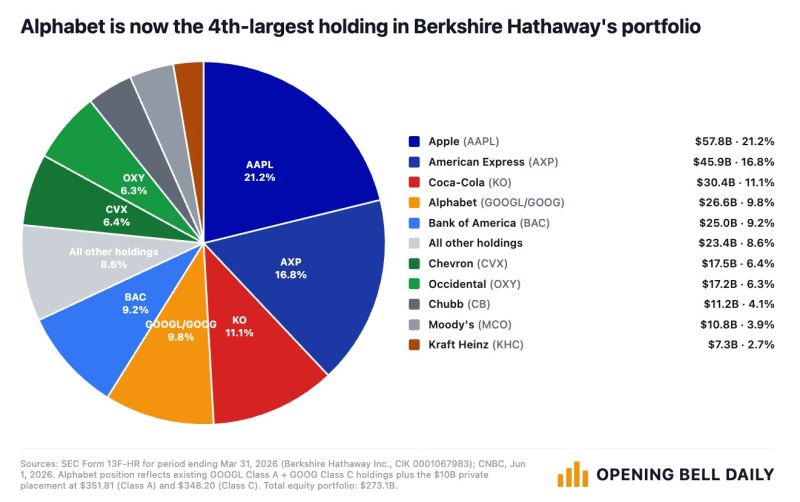

Berkshire Hathaway buys another $10 billion in Alphabet $GOOG to raise its stake to $26 billion.

Warren Buffett never would have guessed that Berkshire's 4th-largest holding would be a $4.5 trillion AI company just one year after he retires. Source: Phil Rosen @philrosenn

Yesterday, $377 BILLION of Market Cap were added to AI infrastructure stocks in a single session.

NVDA +6.19% MU +6.51% DELL +10.79% SNDK +3.72% WDC +3.70% STX +4.71% Every single one of these companies directly supplies the hardware that runs AI, chips, memory, servers, and storage. Demand from data centers is outpacing supply across the board. Dell booked $24.4 billion in new AI server orders in a single quarter. Micron is sold out through 2026. SanDisk and Western Digital are one of the two biggest suppliers of NAND flash memory used in AI storage. Seagate supplies the hard drives filling new data center being built. The market is repricing every company in the AI hardware supply chain at the same time. Source: Bull Theory

JENSEN AT COMPUTEX TAIPEI:

- Marvell will become the next trillion-dollar company - Marvell and Nvidia are strengthening their partnership to expand critical networking & connectivity to power AI data centers Jensen touch...plus 17% Source: amit

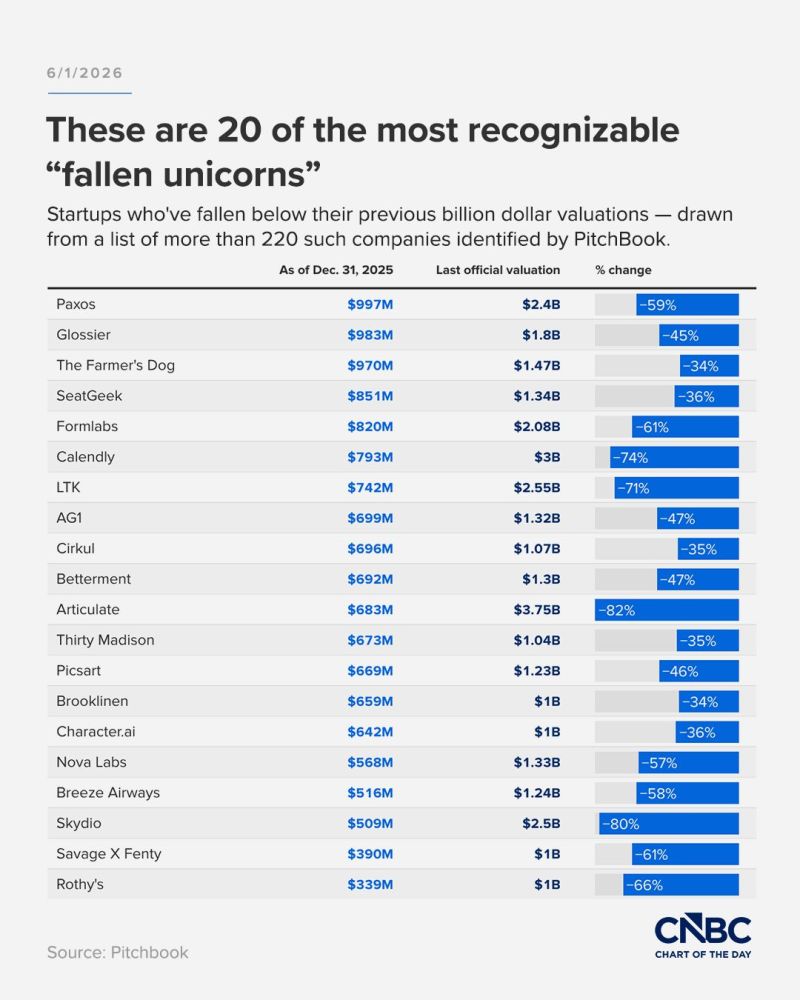

FALLEN UNICORNS

The AI boom that funneled more than $250 billion into OpenAI and Anthropic ahead of their expected mega-IPOs this year has left hundreds of startups built before ChatGPT’s arrival in 2022 stranded — effectively cut off from venture funding because of their inflated valuations and outdated technology, yet not profitable enough for the public markets. More than 220 companies that had reached billion-dollar valuations in the venture boom are now fallen unicorns, according to PitchBook, which provided a list of the companies exclusively to CNBC. The estimates are based on factors including head count growth and comparisons with public companies. Source: CNBC

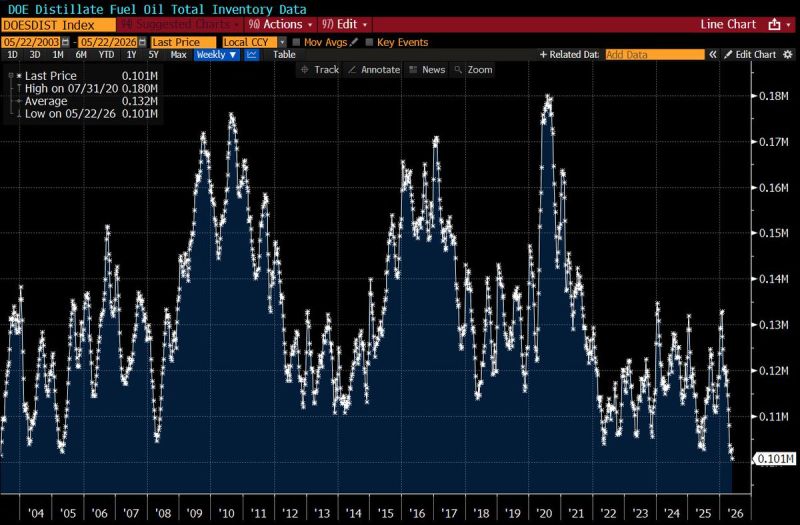

U.S. distillate fuel inventories fall to the lowest level since 2003

Source: Bloomberg, Hedgeye

One of the most striking charts out there: the SOX index has risen sixfold since 2020, while SOX earnings per share have climbed fivefold.

In other words, most of the rally has been backed by real earnings growth, not just higher valuations. The key question now is whether these profits will actually come through and whether they can keep rising. (HT Goldman Sachs) Source: HolgerZ, Bloomberg

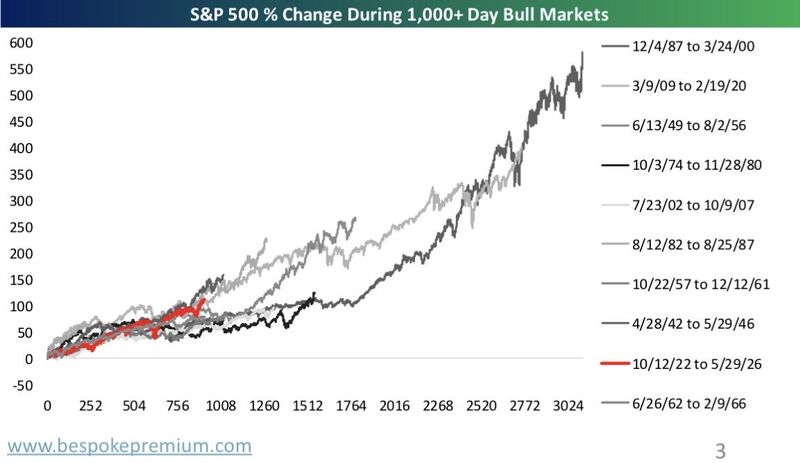

Here’s the current bull market (red line) charted against the nine other bulls since 1928 that lasted 1,000+ days:

Source: Bespoke

Nvidia will launch a PC “superchip” this year as the semiconductor giant goes head-to-head with Apple, Qualcomm, Intel and AMD for the first time.

Computer makers including Dell, Asus and HP will use what Nvidia claims is “the most efficient PC chip ever built”, paired with Microsoft’s Windows software, Nvidia chief executive Jensen Huang announced on Monday. The launch marks a major competitive shift in the consumer PC industry and a new business line for $5.1tn Nvidia. The company, best known for its dominance of semiconductors for AI infrastructure, is pushing beyond its traditional graphics cards into integrated chips that power the whole PC. Lenovo, Microsoft, Acer and Taiwan’s MSI will also use the product. Source: FT