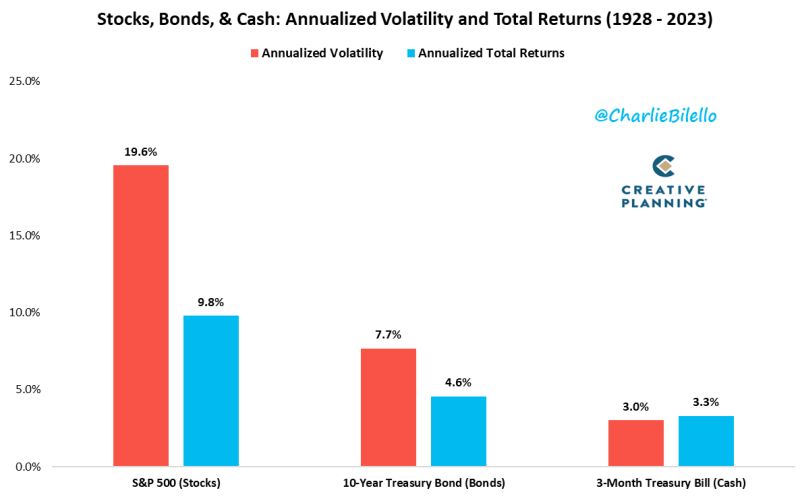

Why investors should embrace risk in one chart by Charlie Bilello:

Annualized Volatility since 1928... Stocks: 19.6% Bonds: 7.7% Cash: 3.0% Annualized Returns since 1928... Stocks: +9.8% Bonds: +4.6% Cash: +3.3%

Bank of America Corp. expects the Federal Reserve to announce plans to begin tapering the runoff of its Treasuries holdings in March, coinciding with its first 25 basis points interest-rate cut.

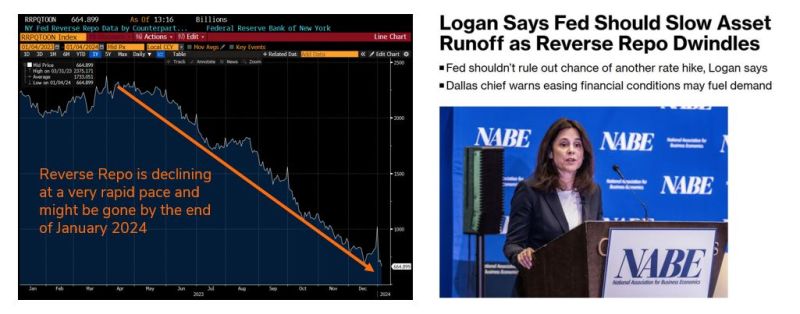

- The Reverse Repo ("RRP") is de facto QE-infinity $ printed during 2020-21 that was sitting dormant. It's now being used to buy up US Treasuries. Problem: it is declining at a very rapid pace and might be gone by the end of January 2024. - Something needs to be done to preserve QB / liquidity. - This is why the Fed is now thinking about slowing down the pace of QT. Over the week-end, Dallas Fed chief Logan said the Fed should slow Asset runoff as Reverse Repo dwindles - 2024 is an election year and we expect net liquidity to be supportive for the economy, bond markets and risk assets

BREAKING bitcoin spot ETF: the fee war has begun

Bitcoin ETF applicants are filing last-minute amendments to lower their fees 👀 BlackRock's lowered to 0.30% 👀 ARK lowered lowered to 0.25% 👀 Wall Street is competing to offer cheap access to $BTC... Source: The Kobeissi Letter, Bitcoin Magazine

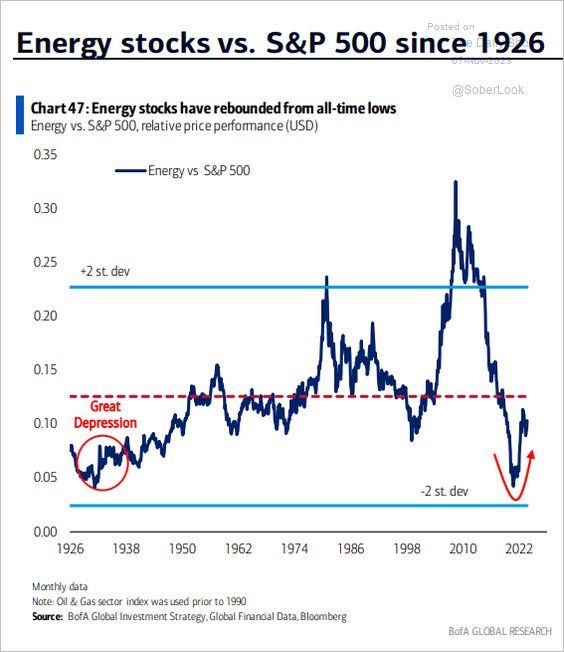

ENERGY STOCKS SINCE 1926 (relative to S&P)

Source: BofA, The Daily Shot

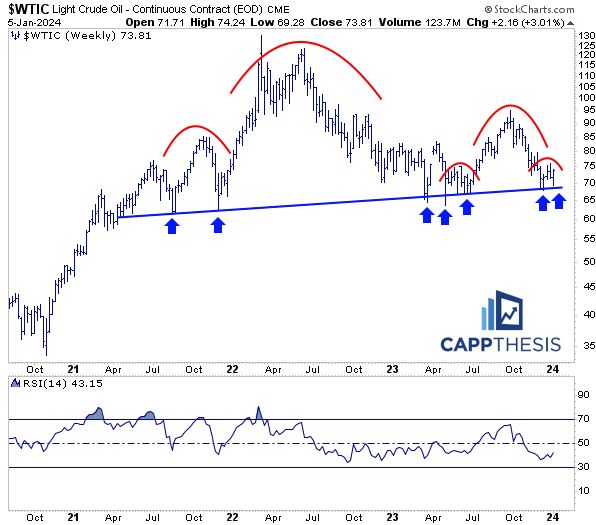

A topping pattern on crudeoil? Or simply finding support at a long-term trendline before a move higher? This one needs to be watched closely

A great chart from Frank Cappelleri thru Ryan Detrick, CMT.

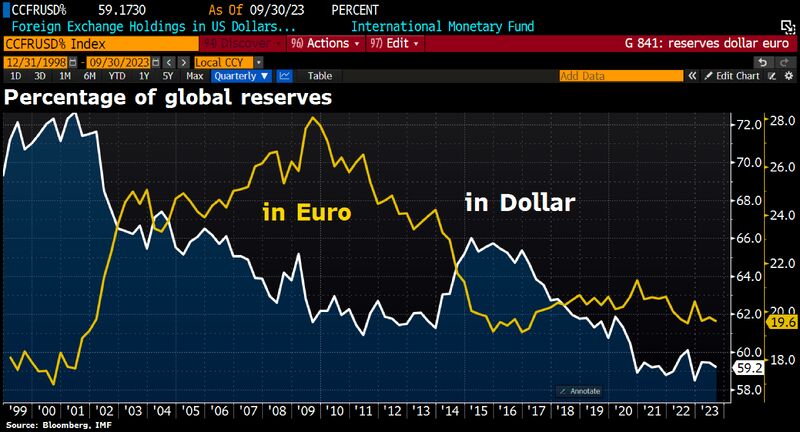

The "multipolar world" will remain a major topic in 2024 as the rewiring of the global commerce system creates geopolitical risks & business model shifts that will last decades

The Dollar’s & Euro's share in global CenBank reserves dropped. Greenback accounted for 59.2% of globally allocated FX reserves in Q3 2023, down from a revised 59.4% in Q2, lowest since Q4 2022. Euro’s share in reserves also fell to 19.6% from 19.7%, while the participation of Japan's Yen rose to 5.5% from 5.3%. Source: HolgerZ, Bloomberg

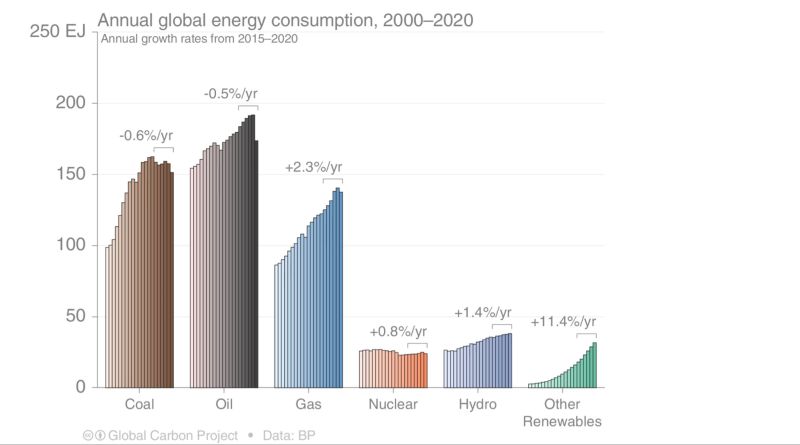

Global Energy Shock Graph (only till 2020 unfortunately) Life without fossil fuels is not for tomorrow

Source: Willem Middelkoop

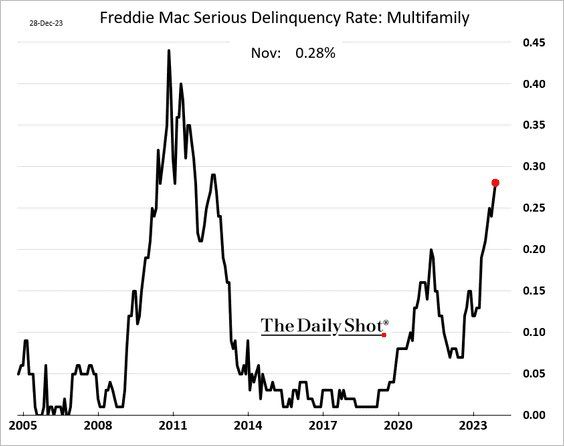

Freddie Mac Serious delinquency rate US multifamily homes

thru The Daily Shot