From beta to alpha ?

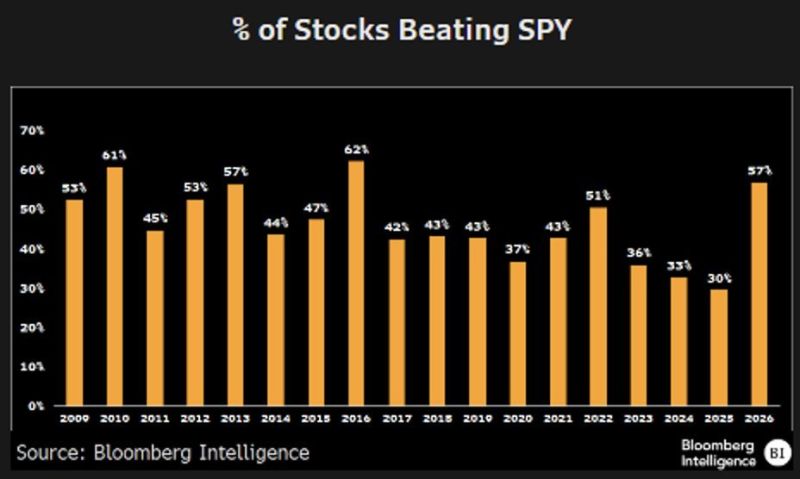

57% of S&P 500 stocks are beating the $SPX this year, the most in a decade. Source. Barchart, Bloomberg Intelligence

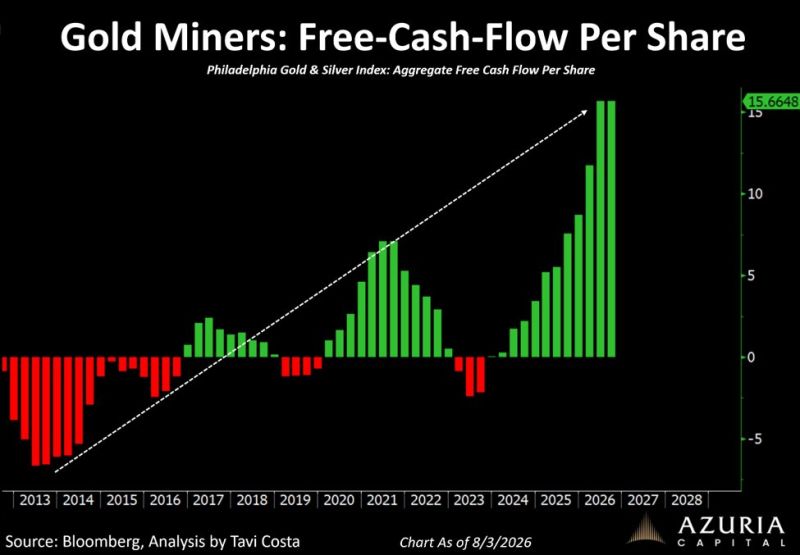

The most profitable period in the modern history of the mining industry?

Source: Tavi Costa

$8.3 Trillion is now sitting in money market funds, an all-time high

Source: Barchart

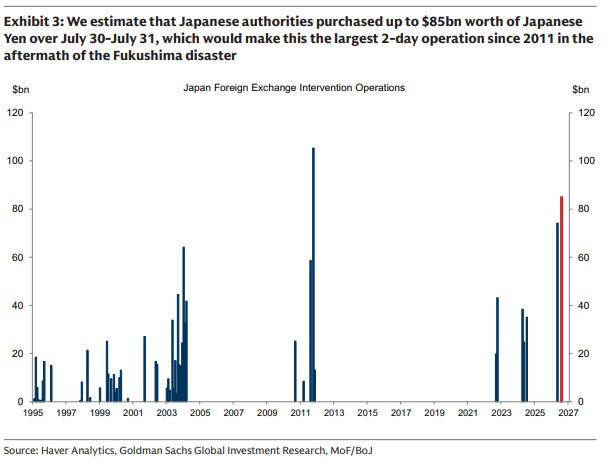

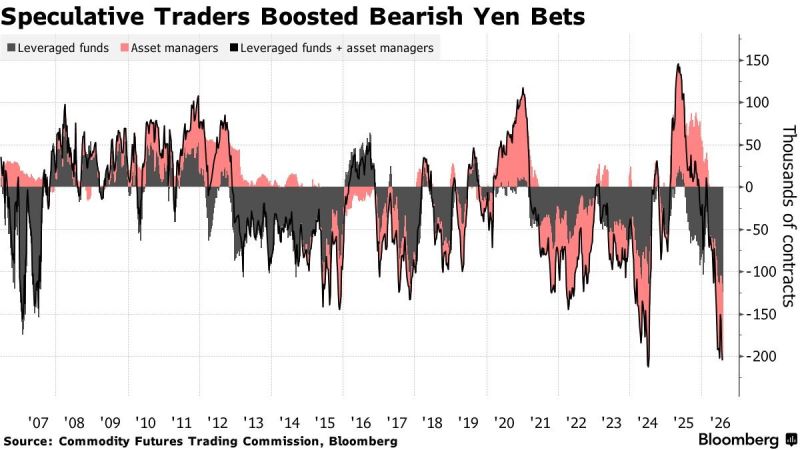

Japan's yentervention last week was the 2nd largest in history ($85BN) second only to Fukushima

Source: zerohedge

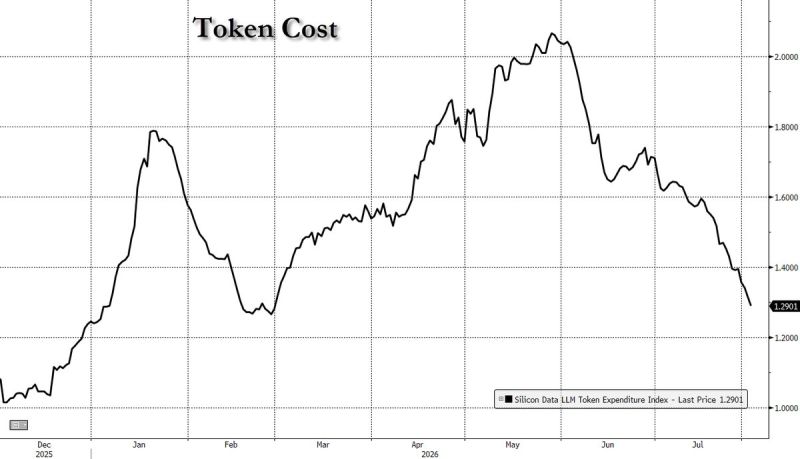

AI TOKEN COSTS ARE DOWN 40% FROM THEIR MAY PEAK.

The main reason? Chinese AI models are dramatically cheaper. DeepSeek, Qwen and Kimi are delivering increasingly competitive performance at 10–35x lower token prices than many U.S. alternatives — and already account for as much as 46% of usage in some enterprise segments. The pressure is spreading. OpenAI, Google and Anthropic have responded by cutting prices by as much as 80%. This creates an interesting dynamic: Cheaper inference → more AI adoption → more token consumption → more demand for compute. But at the same time, it is compressing margins and commoditizing the intelligence layer. The likely long-term winners could therefore be the hyperscalers and infrastructure providers: even if the price per token collapses, exploding volumes can more than compensate. AI intelligence may become a commodity. AI compute may not. And markets still seem far from fully pricing that shift. Source: Austral Research, zerohedge

TRADERS ARE BETTING AGAINST THE YEN AT THE SECOND HIGHEST LEVEL EVER RECORDED

And this is happening just days after Japan and the US spent an estimated $88 billion trying to stop the yen from falling. Combined net short positions from asset managers and leveraged funds hit -205,000 contracts as of July 28, just short of the 2024 record. Hedge funds alone are the most bearish since 2007. The intervention happened, and traders went right back to shorting. Source: Bloomberg, Bull Theory

Berkshire Hathaway hits highest price since Warren Buffett announced his retirement in May 2025

But there is still a huge gap that needs to be filled 👀 Source: Barchart

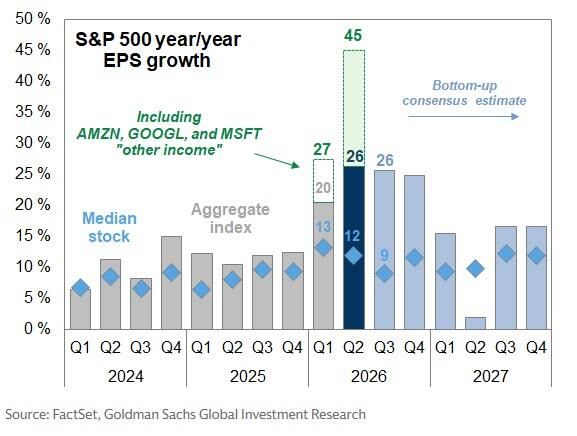

An important observation from Goldman which points out that half The S&P's "record" earnings growth is just "Big Tech" marking up its own stock portfolio.

Here it is, verbatim, from the desk of Goldman's Ioannis Blekos: "S&P 500 EPS growth is tracking at 26% year/year excluding the 'other income' from mega-cap tech's appreciating equity investments. Including those gains, the headline growth rate is 45%." i.e the "record" earnings season you have been told about - the one holding up the most expensive equity market in history - is running at 45% only if you count the gains that Nvidia, and its brethren, book when the stock portfolios they sit on go up. Strip out the mark-to-market of Big Tech valuing its own venture bets, and the number nearly halves, to 26%. Source: GS, zerohedge