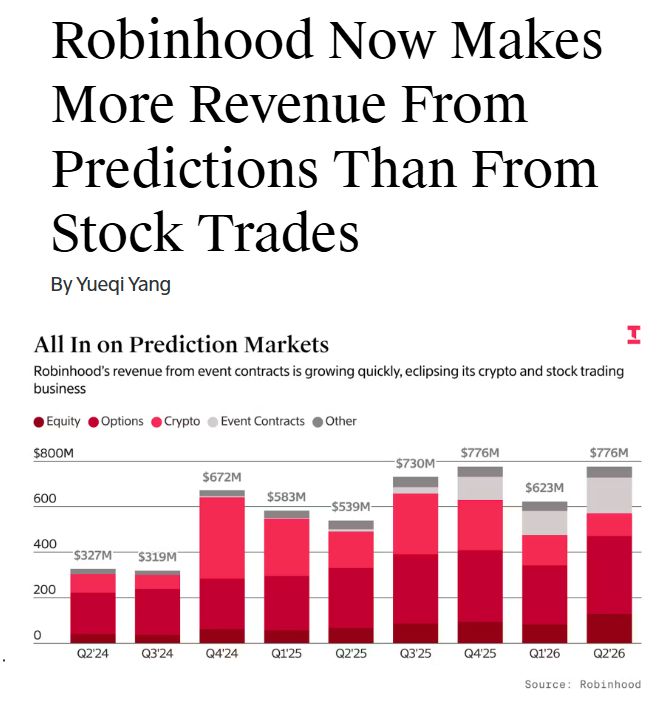

Prediction markets are bigger than stock trading with some brokerages.

Source: Wall Street Mav

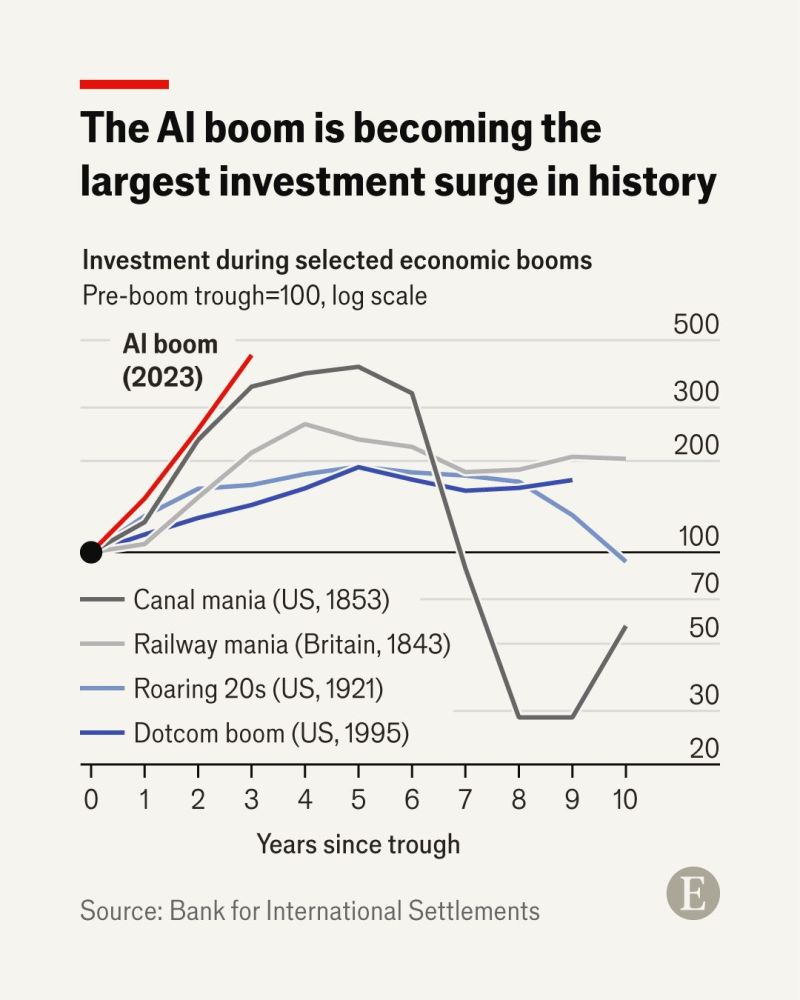

This chart shows how the AI capex boom is fast becoming the largest investment surge in history

compared with previous economic booms such as Britain’s railway mania and America’s dotcom bubble. But the spending could still generate disappointing returns Source: The Economist

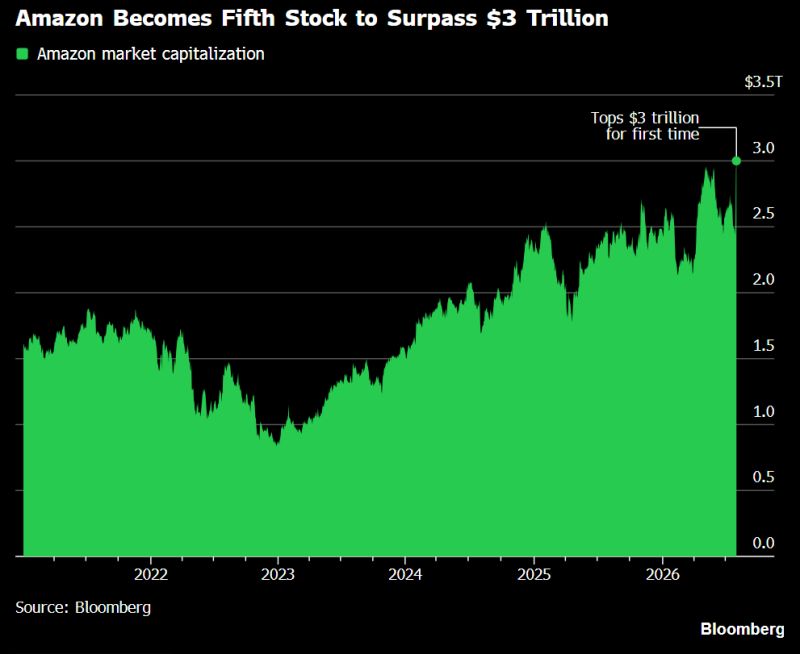

Amazon, $AMZN, becomes the fifth stock to surpass $3 trillion in market cap

Source: Hedgeye

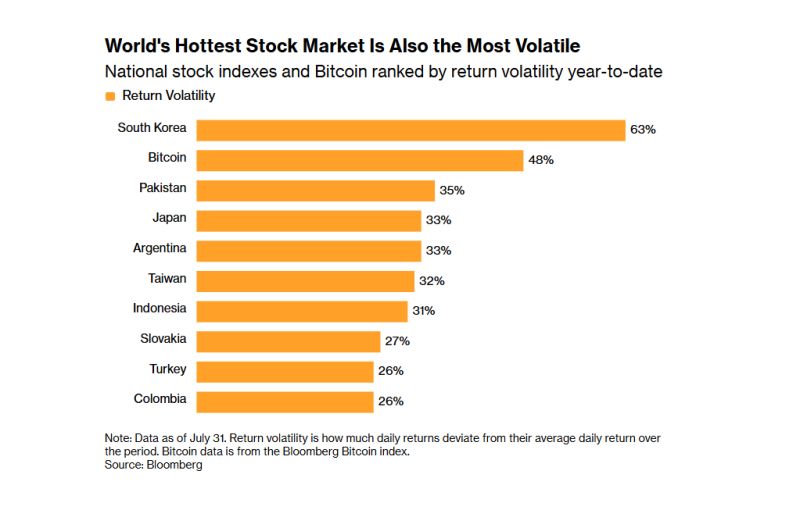

South Korea's benchmark index has seen annualized volatility surge above 60%, nearly twice that of Japan's Nikkei 225.

The Korea Exchange has already triggered emergency circuit breakers nine times this year—compared with just 15 over the previous 26 years. The concentration of Samsung Electronics and SK Hynix, which account for more than half the index, combined with a boom in leveraged ETFs, has amplified market swings. Assets in leveraged ETFs have jumped from $5 billion to over $40 billion in six months, with retail investors holding nearly 90% of them. In response, regulators and the central bank have introduced measures including ETF exposure limits and higher trading costs to reduce volatility. Source: Bull Theory

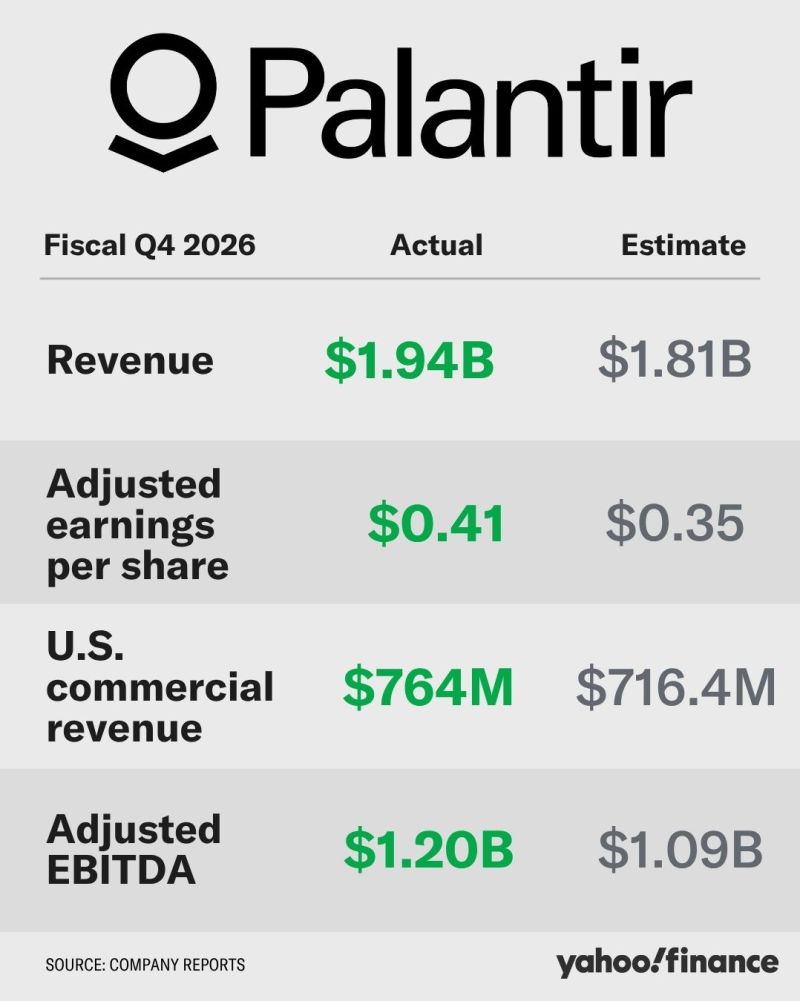

Palantir $PLTR was up 7% after market as they beat earnings estimates.

$PLTR Q2 visualized: • Revenue: $1.94B (+93%) • Gross profit: $1.64B (+101%) • Cost of revenue: $0.29B (+254%) • Net income: $1.06B (+225%) Source: Russ Faigen

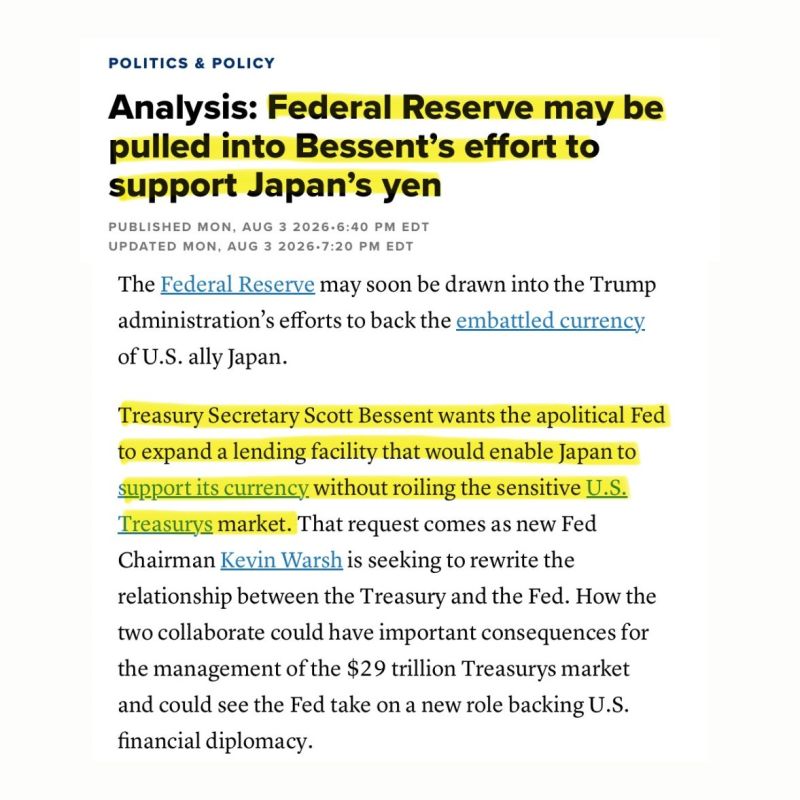

Treasury Secretary Scott Bessent is reportedly urging the Federal Reserve to expand support for Japan, allowing it to raise dollars without selling its massive holdings of US Treasuries.

Japan owns roughly $1.1 trillion in US government bonds. When it intervenes to support the yen, it needs dollars. Once its cash reserves are depleted, selling Treasuries becomes the most direct way to fund further intervention. That is a problem for the US. Large Treasury sales would increase bond supply, pushing prices lower and yields higher. With the 10-year Treasury yield recently climbing above 4.7%, Washington has strong incentives to avoid additional upward pressure. The solution is the Fed's FIMA Repo Facility. It allows foreign central banks to temporarily exchange Treasuries for dollars without selling the bonds into the market. Japan receives dollar liquidity, then later repays the funds and takes back its securities, leaving the bond market largely unaffected. The challenge is capacity. The facility is currently capped at $60 billion per day, while Japan is estimated to have spent $60–80 billion supporting the yen in just one week. According to reports, Bessent wants that limit increased. However, expanding the facility would require approval from the Federal Open Market Committee (FOMC), and the Federal Reserve has so far declined to comment. Source: Bull Theory

The market broadening in one chart

The S&P 500 Equal-weight index $SPY just hit new all-time high while the Nasdaq 100 $NDX is still over 8% below highs. Source: Bloomberg, RBC

Gold is coiling and getting ready for a big move

Bollinger Bands are now the tightest since August 2025, right before Gold soared 60% over the next 5 months. Source: Barchart