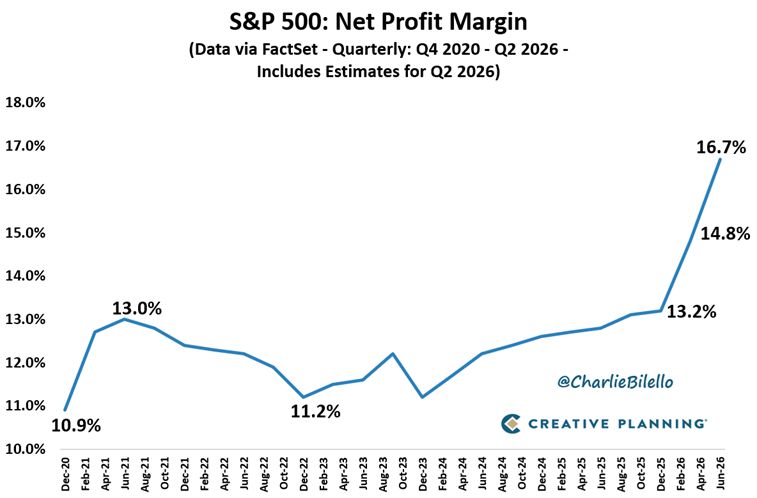

S&P 500 profit margins spiked to 16.7% in Q2, which is by far their highest level in history.

“Profit margins are probably the most mean-reverting series in finance, and if profit margins don't mean revert, then something has gone badly wrong with capitalism. If high profits don't attract competition, there's something wrong with the system.” - Jeremy Grantham Charlie Bilello

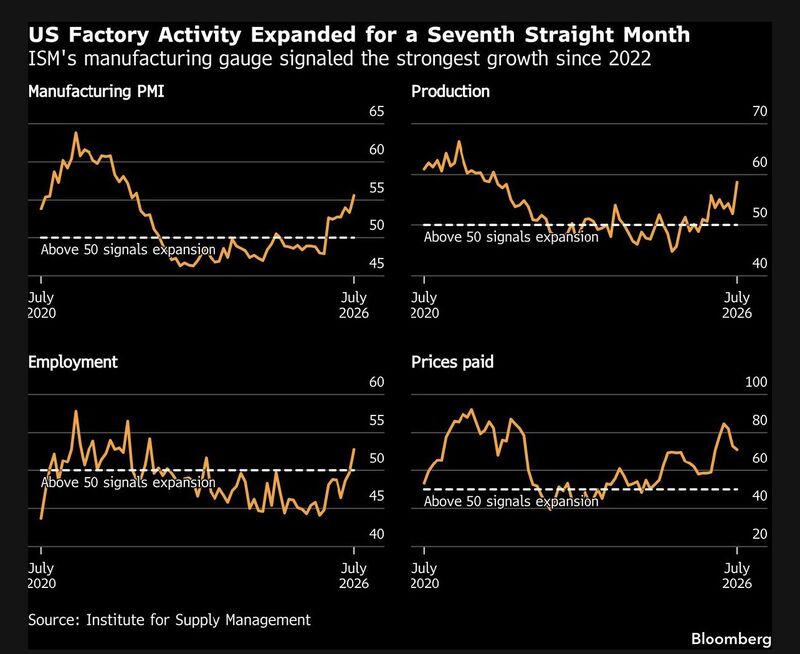

US manufacturing is booming, expanding at the fastest pace since 2022 and beating expectations in many metrics for the month of July.

Omar Sharif of Inflation Insights points out that the ISM production index rose by the most for any July since 1951. Source: Lisa Abramowicz

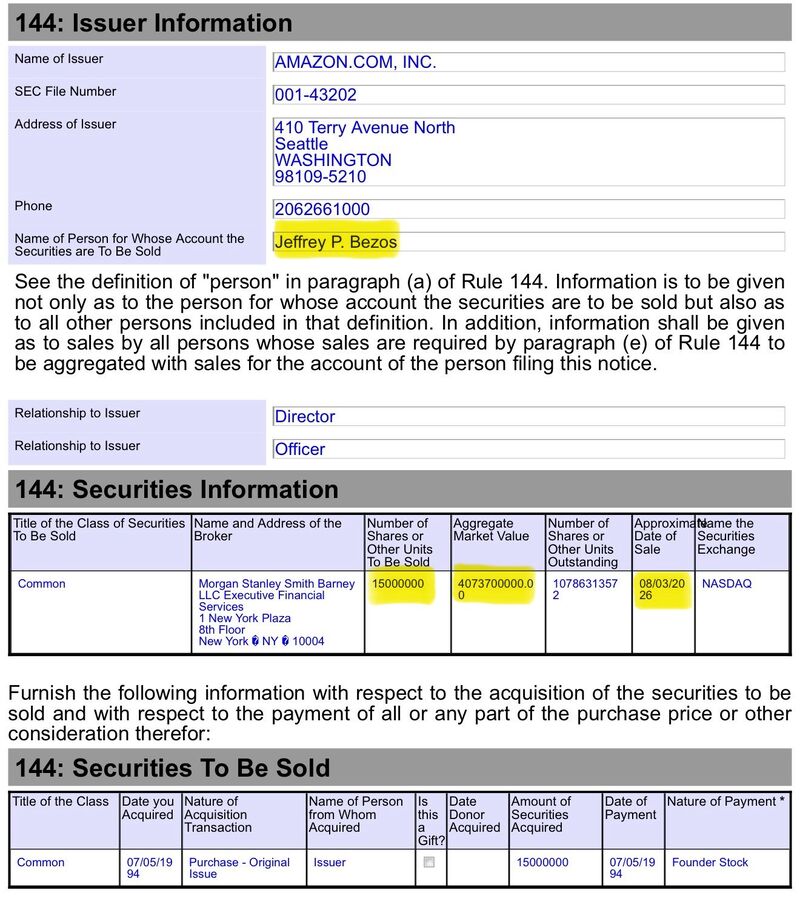

Jeff Bezos sold $4,073,700,000 worth in Amazon $AMZN stock today, his first sale of stock in over a year.

Source: Trend Spider

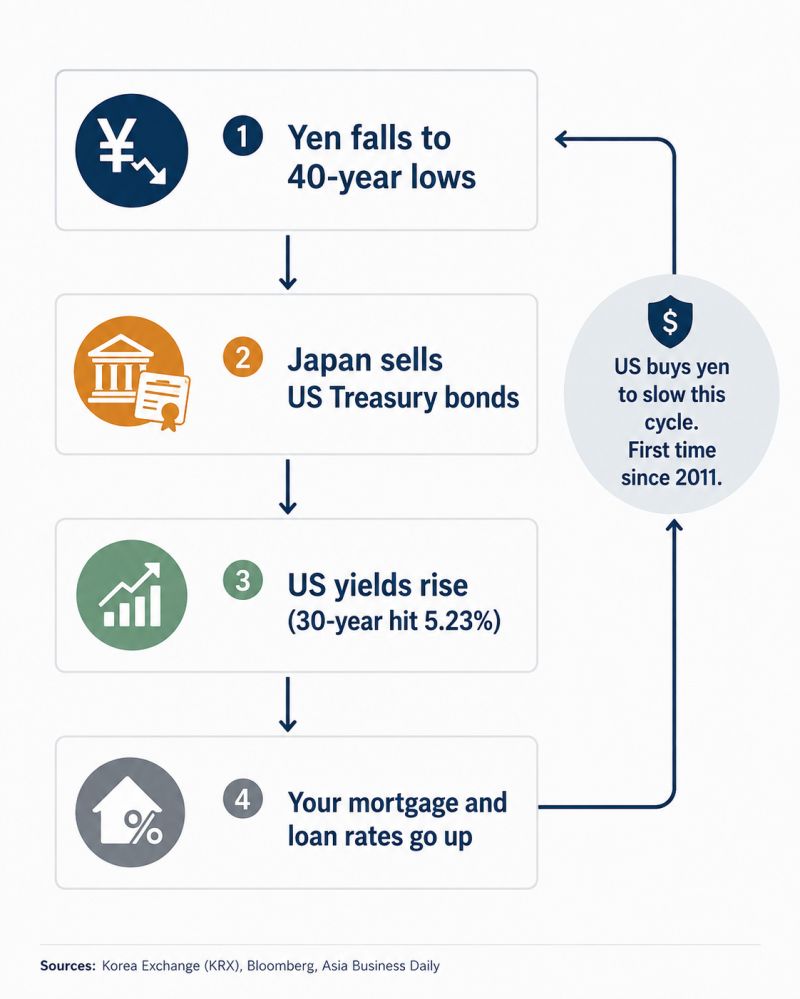

The US just stepped in to support Japan's currency—without selling dollars

The US Treasury reportedly bought Japanese yen for the first time since 2011, funding the move by selling euros rather than dollars. The goal: help stabilize the yen while avoiding downward pressure on the US dollar. Why does this matter? Japan owns about $1.19 trillion in US Treasuries, making it the largest foreign holder. If the yen weakens too much, Japan may need to sell Treasuries to raise dollars and defend its currency. More Treasury selling can push US bond yields higher, increasing borrowing costs across the economy—from mortgages to auto loans. Japan can also tap the Fed's FIMA Repo Facility, allowing it to borrow dollars against its Treasury holdings instead of selling them outright. That could reduce pressure on the US bond market. Reports suggest the US and Japan may announce a coordinated currency policy in the coming days. Source: Hedgie

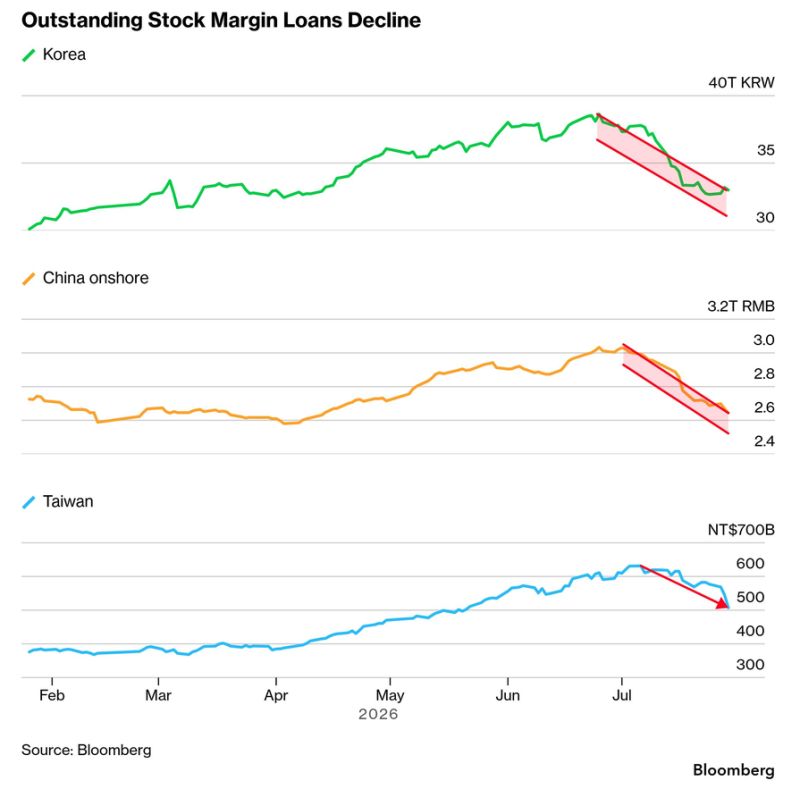

Leverage is unwinding across Asia

The borrowing that fueled this year's rally is now accelerating the selloff. In South Korea, margin debt has fallen by $4 billion since June, while leveraged ETF assets have plunged 70% (from $53 billion to $16 billion). Retail cash set aside for stock purchases has dropped 23%, and many Samsung and SK Hynix investors are now sitting on losses. The deleveraging is spreading across the region, with margin loans also falling sharply in China and Taiwan. As leveraged positions are unwound, forced selling is amplifying market volatility. Source: Global Markets Investor

The Nasdaq just posted its worst July in 22 years

The Nasdaq-100 fell 6.6% in July, while semiconductor stocks led the decline, with SOXX down 22.1%, its worst month since 2002. Unlike previous selloffs driven by a single catalyst, this correction reflects concerns over AI valuations, crowded positioning, and rising Chinese competition. Yet investors continue to buy the theme: Goldman Sachs estimates nearly $13 billion flowed into semiconductor ETFs during the decline. Meanwhile, gains in the equal-weight S&P 500 and software stocks suggest capital is rotating rather than leaving equities. The correction has reduced leverage and valuations, but conviction in the long-term AI story remains intact. Source: Bull Theory

Oil Reserves Are Still Dominated by the Giants

Proved reserves show where long-term oil power still sits Saudi Aramco remains in a league of its own with around 260 billion boe Source: Jack Prandelli on X

Brent Crude Oil crashes 10% as US and Iran halt strikes.

President Trump said the “perimeters of a deal” had been reached with Iran to reopen the Strait of Hormuz after speaking with Saudi Crown Prince Mohammed bin Salman (MbS). According to Saudi Arabia’s state news agency, both leaders emphasized dialogue, de-escalation, and pursuing a truce to prevent a wider regional conflict. Axios reported that MbS urged Trump to avoid large-scale strikes on Iran, warning of possible retaliation against Israeli and Gulf energy infrastructure. Saudi officials also sought clarity on U.S. military plans. As a key U.S. ally, Saudi Arabia has historically shaped Washington’s Iran policy and appears to have influenced efforts to delay or limit further escalation. Source: zerohedge