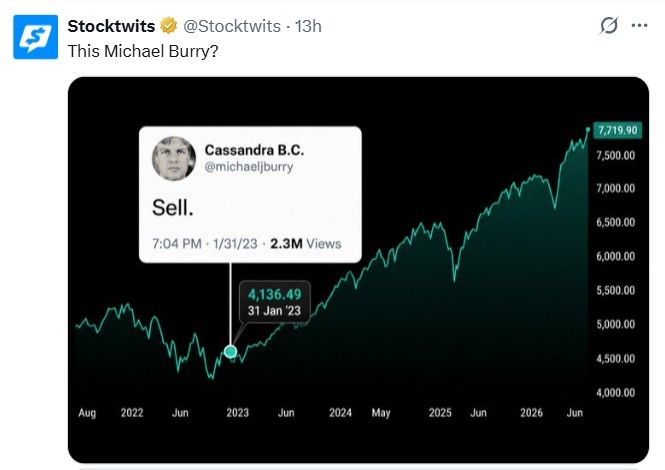

Being short the market can be dangerous

Source: Stockwits

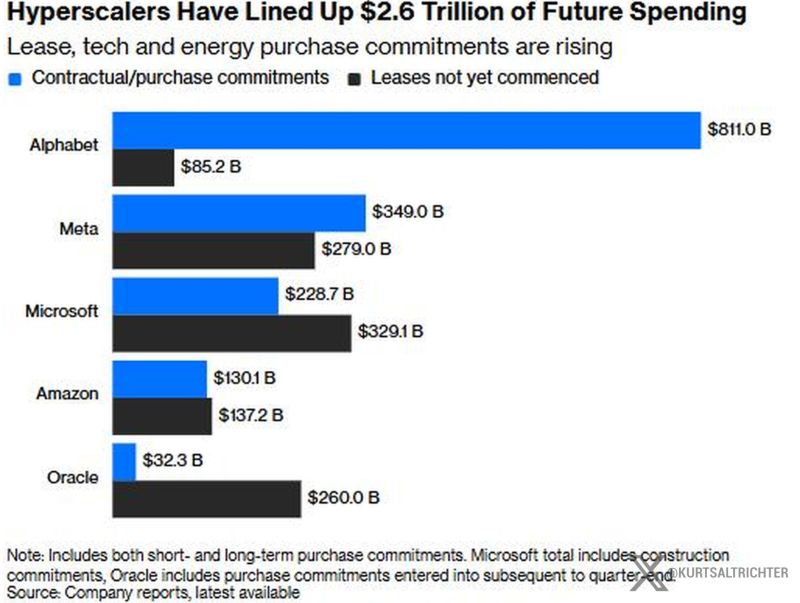

The scariest number in the AI boom may be the one you won’t find on the balance sheet.

The five largest hyperscalers have committed more than $2.6 trillion to data centers, chips, and power infrastructure. Alphabet alone reportedly carries $811 billion in commitments, much of it disclosed deep in the footnotes. And these obligations don’t disappear if AI demand falls short of expectations. Meanwhile, the cost of insuring Big Tech debt is already rising. That matters because credit markets often detect stress before equity markets do. If AI infrastructure spending grows faster than the revenues it generates, the first warning sign may not come from tech stocks. It could come from the bond market of the biggest companies on Earth. Source: Kurt S. Altrichter, CRPS®

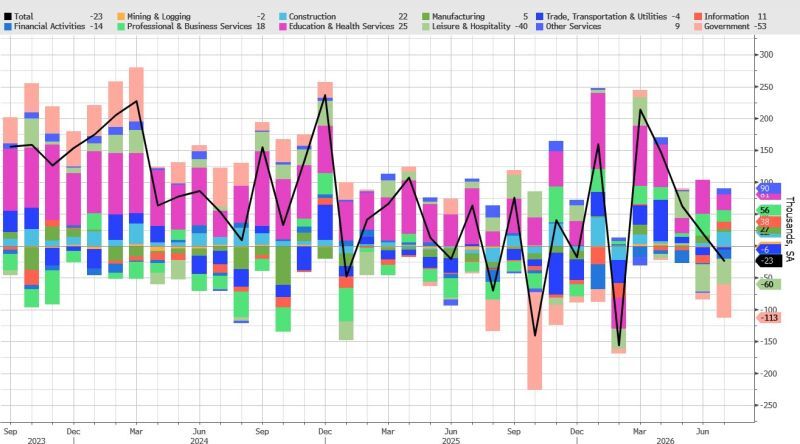

Two key drivers for today's big jobs drop:

1. Leisure and Hospitality jobs -40K (of which -26.1K restaurant workers and -16.1K performing arts, sports, amusement and recreation) which was mostly World Cup driven 2. Local government jobs, entirely due to education (-50K), i.e. vacation. Source: zerohedge

Gold ripping and now finally breaking out

Source: Barchart

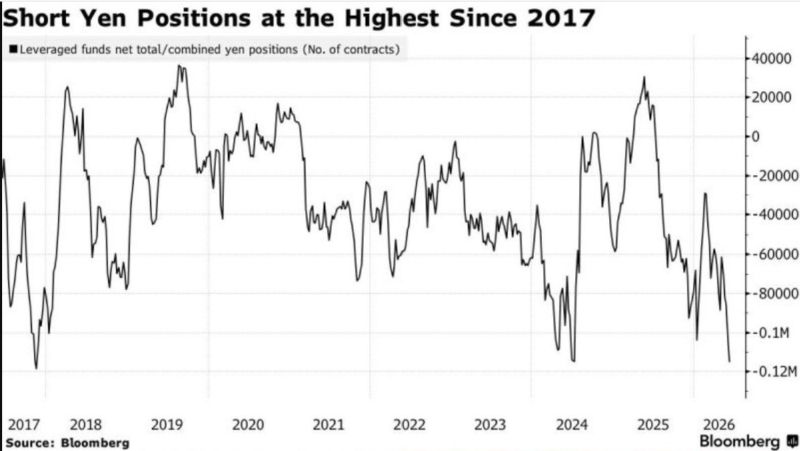

THE WORLD'S MOST DANGEROUS TRADE IS GETTING EVEN MORE CROWDED.

Leveraged funds are now holding their largest short position in the Japanese yen since 2017. They're borrowing ultra-cheap yen to buy higher-yielding assets, particularly U.S. technology stocks, making the yen carry trade more crowded than it has been in years. The risk is what happens if the yen suddenly strengthens. A sharper yen forces investors to buy back the currency to repay their loans, triggering rapid deleveraging across global markets. We've seen this before. In August 2024, the yen surged roughly 14% against the U.S. dollar, sparking a violent unwind of carry trades. More than $6 trillion was erased from global equity markets, and panic selling reached levels not seen since the COVID crash. Today, speculative positioning is even more extreme. That doesn't guarantee another unwind—but it does mean the market is more vulnerable if the yen stages another sharp rally. Source: The Macro Paper

This looks like a clean breakout

#goldminers Source: Tavi Costa

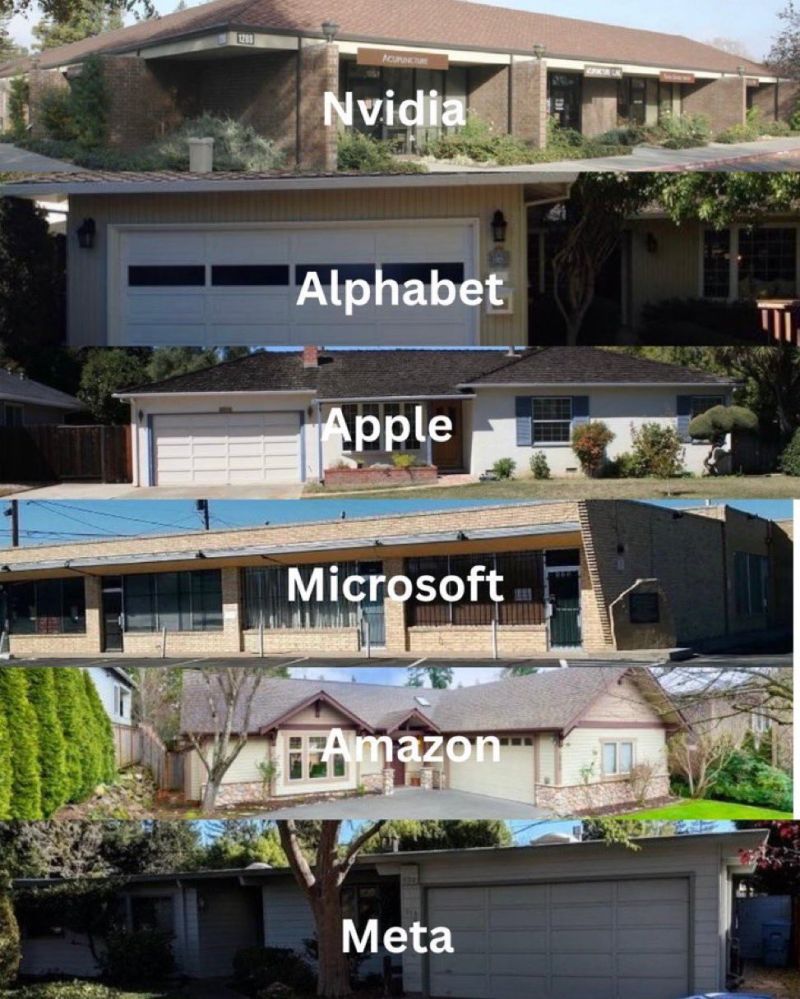

First offices of 6 companies worth a combined $22 trillion.

Source: Jon Erlichman

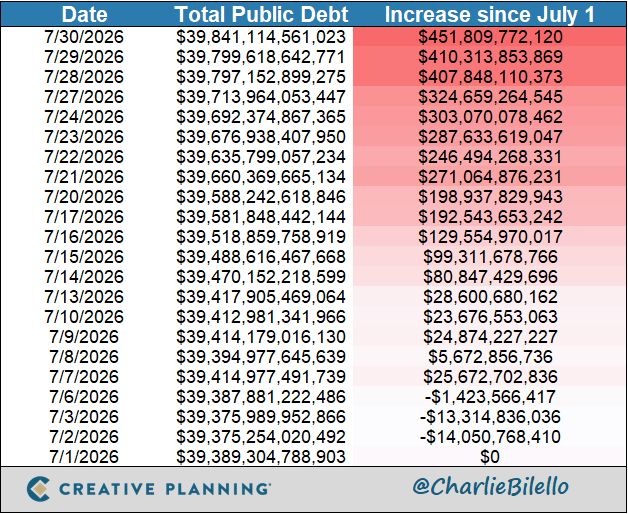

The U.S. has added $450 billion to the national debt since July 1st.

That’s over $15 billion a day. “There are two ways to enslave a country. One is by the sword. The other is by debt.” – John Adams Source: Peter Mallouk @PeterMallouk