As highlighted by The Kobeissi Letter, the US housing market is having its historical moment

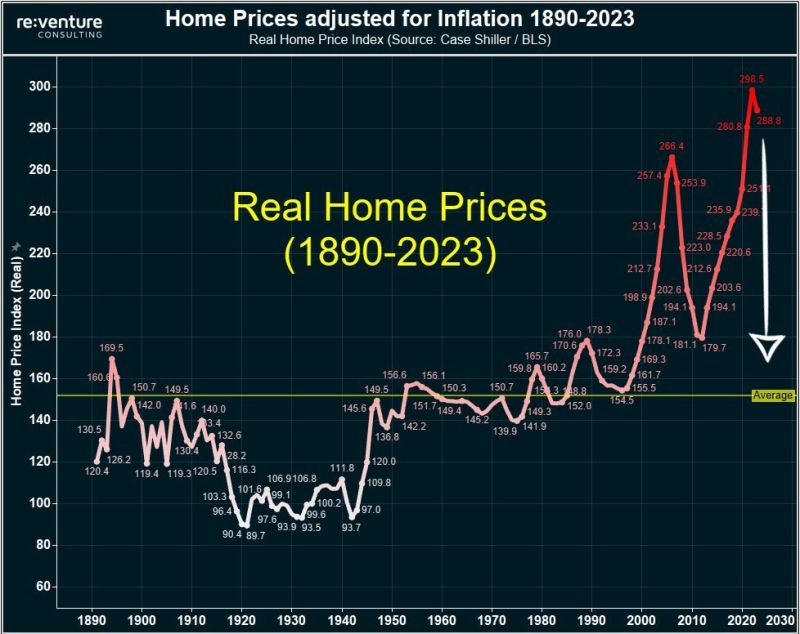

The US housing market is having its historical moment. Indeed, Real home prices in the US are currently almost 10% MORE expensive than they were in 2008. In fact, real home prices are now 80% ABOVE the 130-year historical average, according to Reventure. This means that even on an inflation adjusted basis, home prices have never been more expensive. Meanwhile, housing supply is 40% below the historical average. All while mortgage demand is at its lowest since 1994 and the median homebuyer now has a $3000/month payment. Source: The Kobeissi Letter, Reventure

As of the end of October, investor's sentiment index was almost at maximum fear

But November turns out to instead be among one of the greatest months in stock market history. Source: J-C Parets

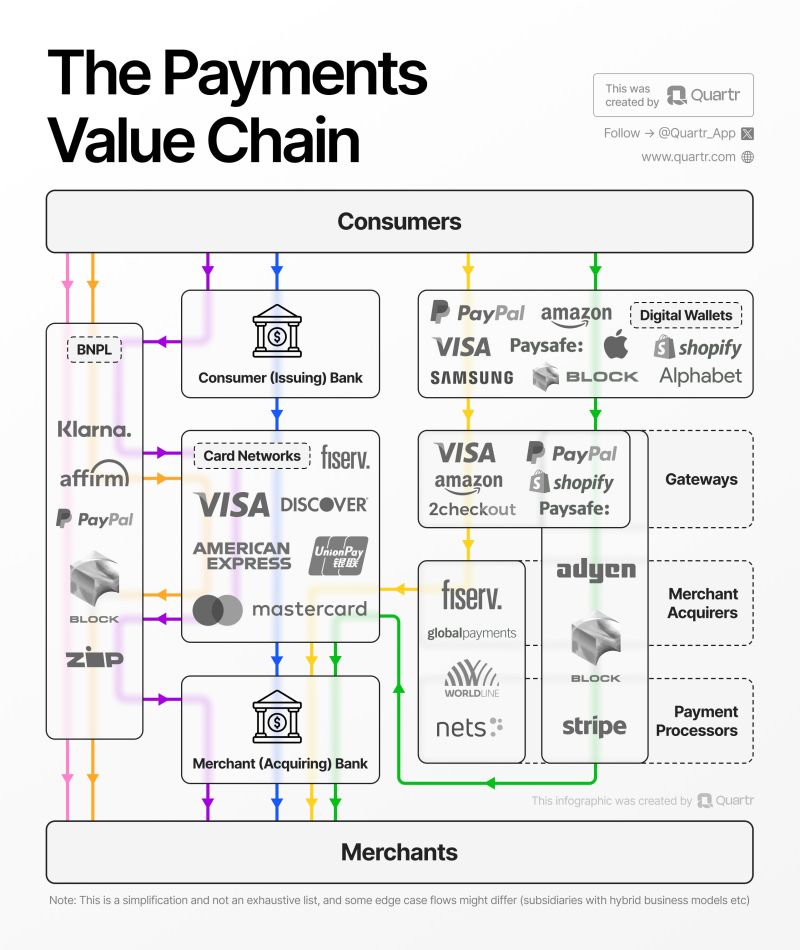

The Payments Value Chain by Quartr

They jave updated our highly appreciated infographic explaining the complex payments layer between consumers and merchants. It illustrates how and where key players such as $V, $MA, $FISV, $ADYEN, $AMZN, and $PYPL fit in. Source: Quartr

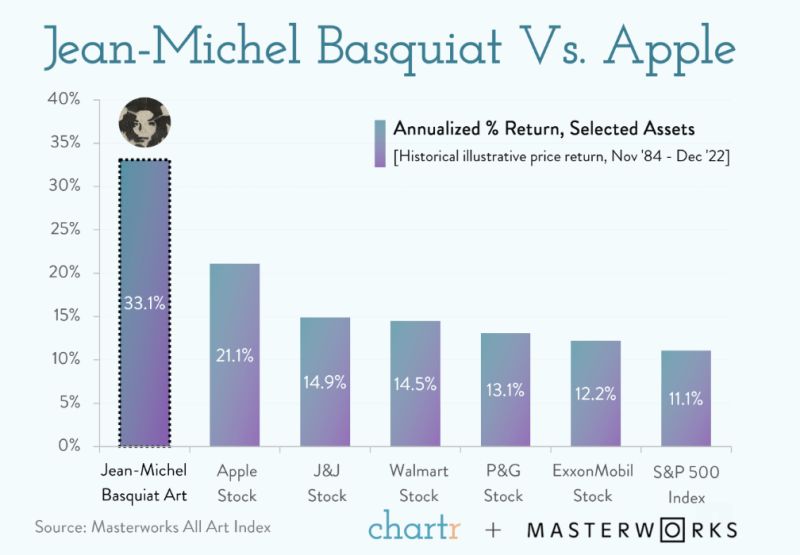

Contemporary art beats stocks and Basquiat beats apple

Since 11/84, Jean-Michel Basquiat has been generating higher annualized return than apple... Source: Chartr

Friday Humor

Food for Thought

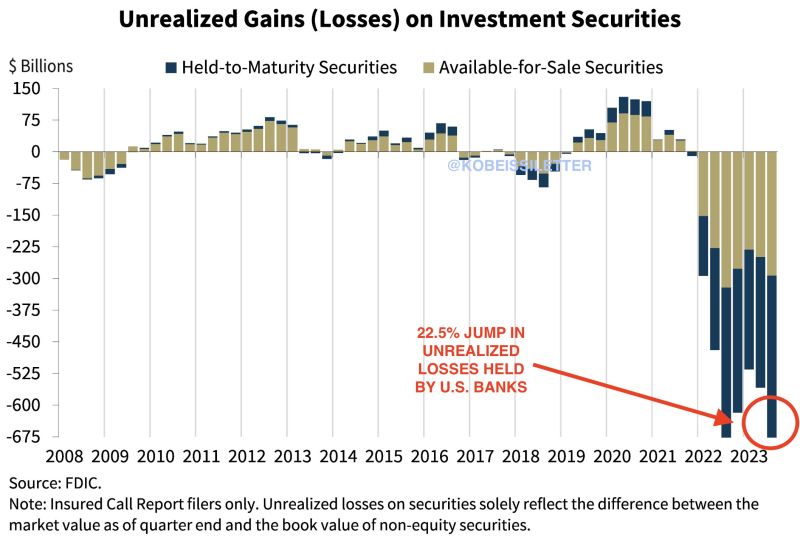

Is the US banking crisis really over?

Unrealized losses on investment securities held by US banks hit $684 billion in Q3, according to the FDIC. This marks a 22.5% jump compared to unrealized losses seen last year. The jump was primarily driven by rising mortgages rates reducing the value of mortgage-backed securities held by banks. Despite these challenges, the FDIC states that banks remain "well capitalized." This comes as usage of the Fed's emergency funding facility for banks hit another record high of $114 billion. Source: The Kobeissi Letter

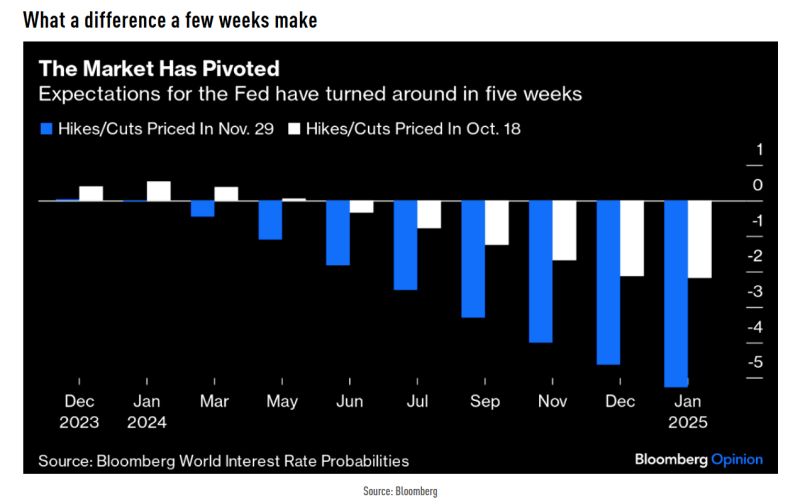

Massive change over the past 5 weeks when it comes to what the market is pricing from FED

Source: TME, Bloomberg

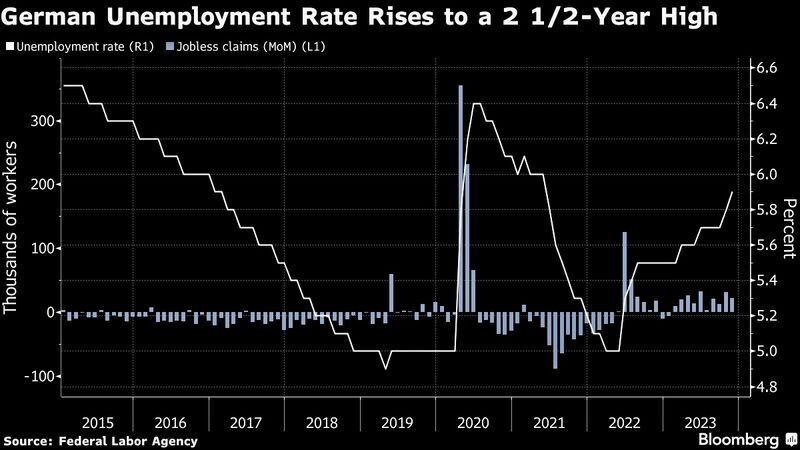

The German labor market is now sending out alarm signals despite the shortage of skilled workers

Germany’s unemployment rate unexpectedly rose to 5.9% in November, the highest level in 2.5 years. Joblessness increased by 22k. Source: Bloomberg, HolgerZ