Carnage in hyperscaler bond land:

Investment Grade bond spreads for hyperscalers are exploding every day, as credit investors refuse to fund memory chip purchases any longer. CDS (inverted in red on the chart below) are following. How long will it take for the hyperscaler stocks (in blue) to follow ? Source: zerohedge

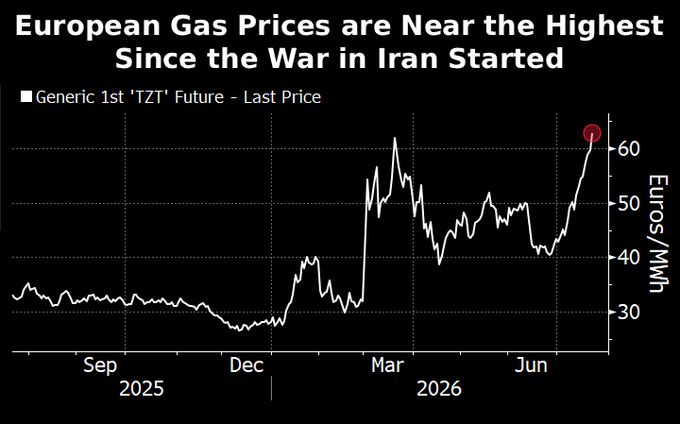

European gas futures are back near their highest level since the Iran war started

The reason: Europe is losing the LNG bidding war. Imports down 35% y/y over the last month; China's up 8%. TTF is back near its post-Iran-war high — not because Europe wants more gas, but because it has to pay up to get any. The cargoes aren't disappearing, they're just sailing east. US exporters are indifferent to which. Source: Jack Prandelli on X, Bloomberg

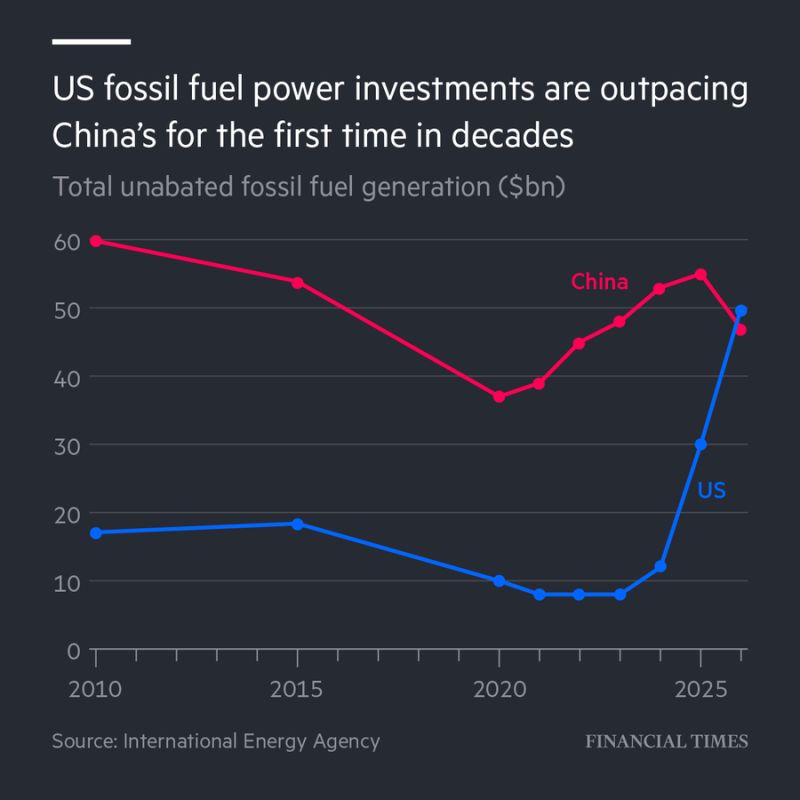

U.S. fossil fuel power investment is now outpacing China's for the first time in decades

Source: Hedgeye, FT, IEA

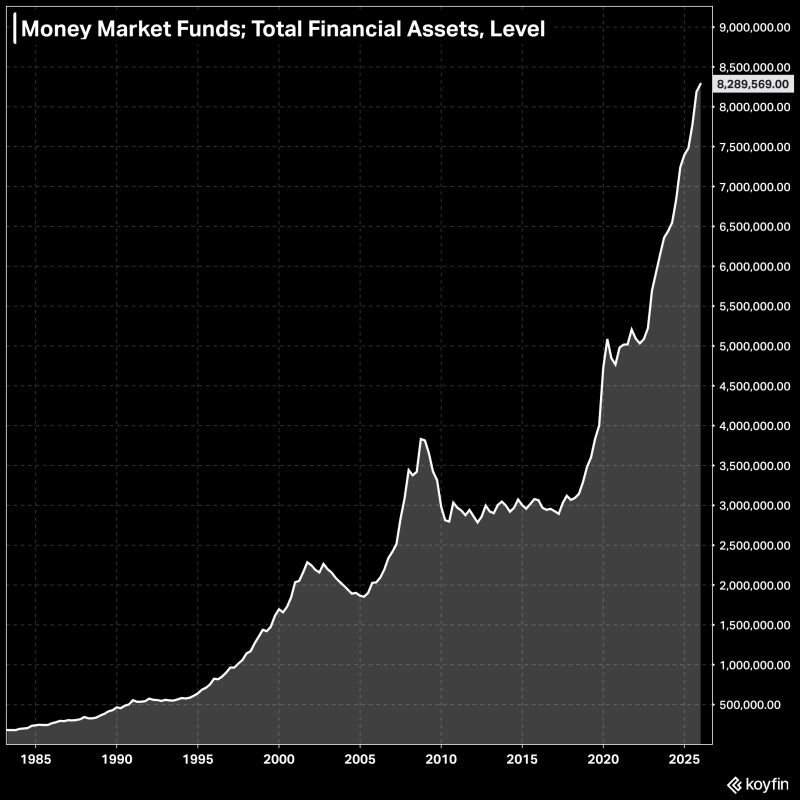

There is a record $8.29 trillion in money market funds right now.

Source: Koyfin

$1.48 TRILLION has been wiped out from SpaceX $SPCX in the last 37 days, as it hits a new all-time low.

Source: Bull Theory

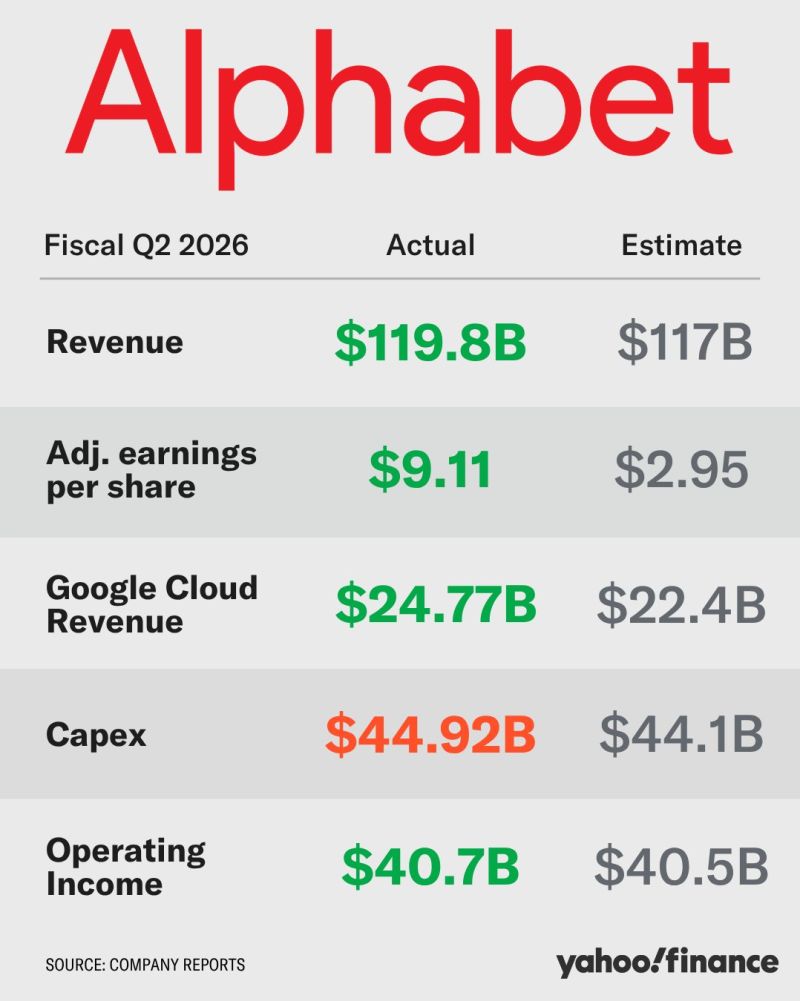

Alphabet beat Q2 revenue expectations, but missed on underlying earnings.

Revenue rose 24% to $119.8 billion, led by an 82% increase in Google Cloud revenue to $24.8 billion. Cloud operating margin reached 36%. Reported net income was boosted by roughly $99 billion in unrealised gains on investments including Anthropic and SpaceX. Excluding these gains, adjusted EPS was $2.85 versus $2.90 expected. The stock fell 3% after hours. Source: App Economy Insights @EconomyApp Bull Theory Yahoo Finance

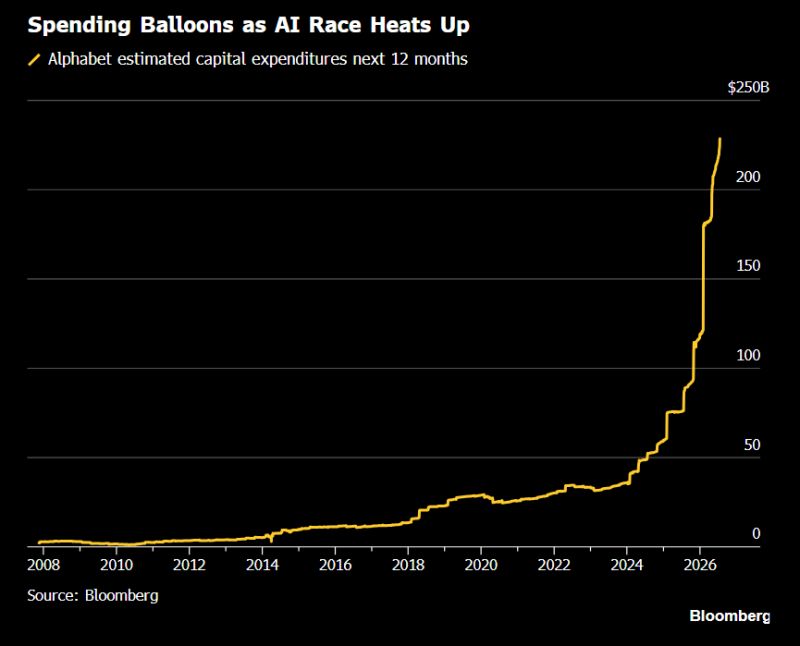

Google's capex is on track to nearly triple in two years

Source: Hedgeye @Hedgeye Bloomberg

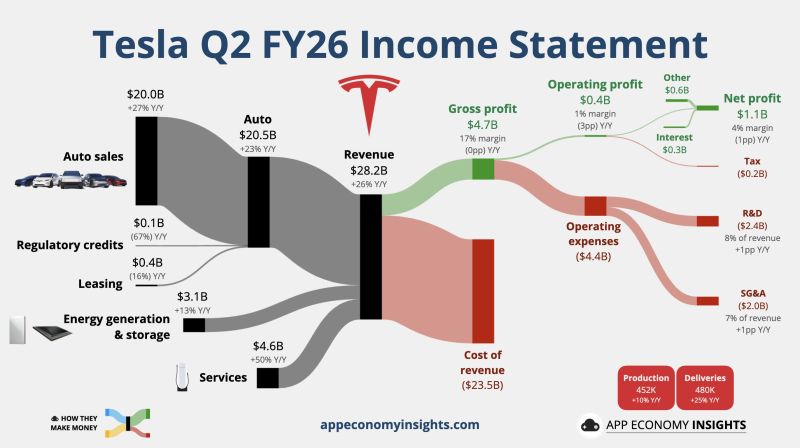

Tesla $TSLA is getting pounded after-hours after missing badly on earnings

Adjusted EPS came in at 33 cents, well below the 51 cent estimate. Gross margin fell to 16.8%, versus 19.4% expected. Tesla sold more cars than ever this quarter, but had to cut prices and lean on incentives to do it. More volume, less profit per car. $TSLA Tesla Q2 FY26: • Revenue +26% Y/Y to $28.2B ($1.8B beat) • Gross margin 17% (flat Y/Y) • Operating margin 1% (-3pp Y/Y) • CapEx +142% Y/Y to $5.8B • Free cash flow flips negative -$1.1B • Non-GAAP EPS $0.33 (versus $0.51 expected = MISS) Source: App Economy Insights Barc chart