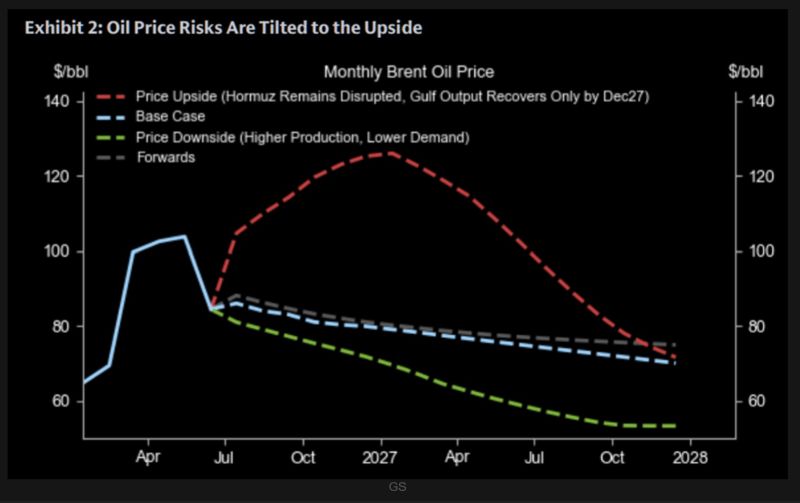

Goldman Sachs models a scenario where the Strait of Hormuz remains disrupted through late 2027.

Under these conditions, they project Brent crude could spike above $120/bbl by Q4 2026, before settling at an average of ~$100/bbl throughout 2027. This contrasts sharply with Goldman's $80 base case, suggesting current prices still assign relatively low odds to a prolonged physical supply disruption Source: GS, TME

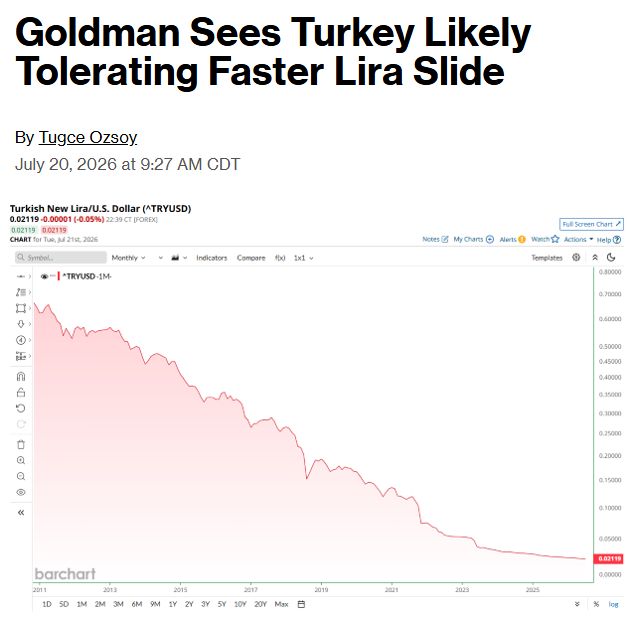

Turkey will let the Lira fall even faster against the U.S. Dollar, cautions Goldman Sachs 🚨

Apparently a 97% dump over 15 years isn't enough... Source. Barchart

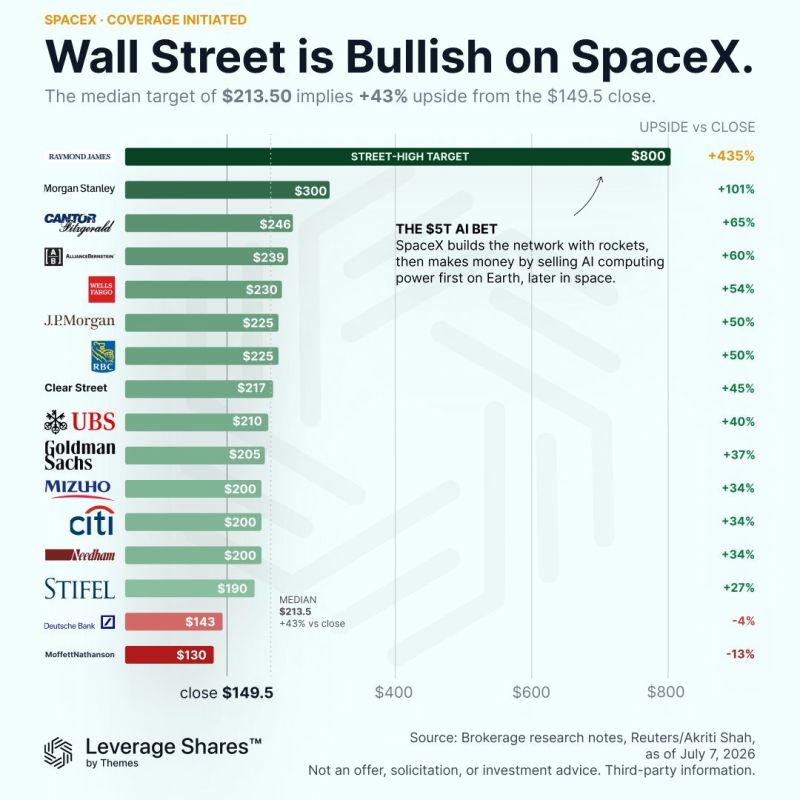

SpaceX $SPCX stock is currently trading at $122 per share

Wall Street has price targets on the stock as high as $800 and as low as $130 That means SpaceX stock is currently trading below every Wall ST analyst price target according to the graphic below from my partners at Leverage Shares Source: Evan, Leverage shares

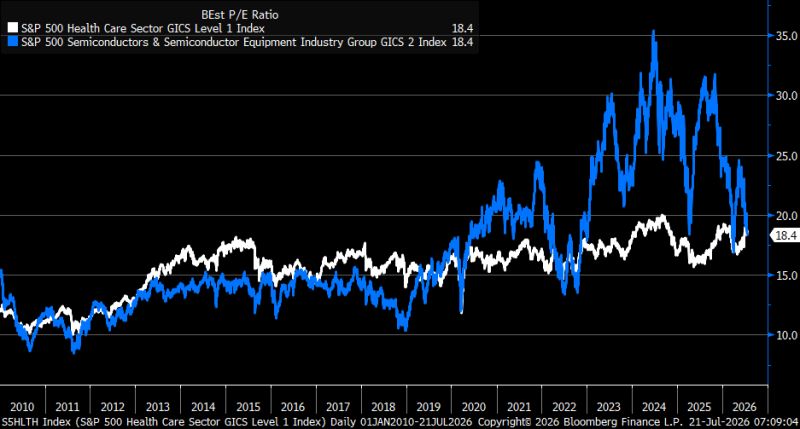

Forward P/E for both Health Care and Semiconductors are now the same...

Source: Bloomberg, Kevin Gordon

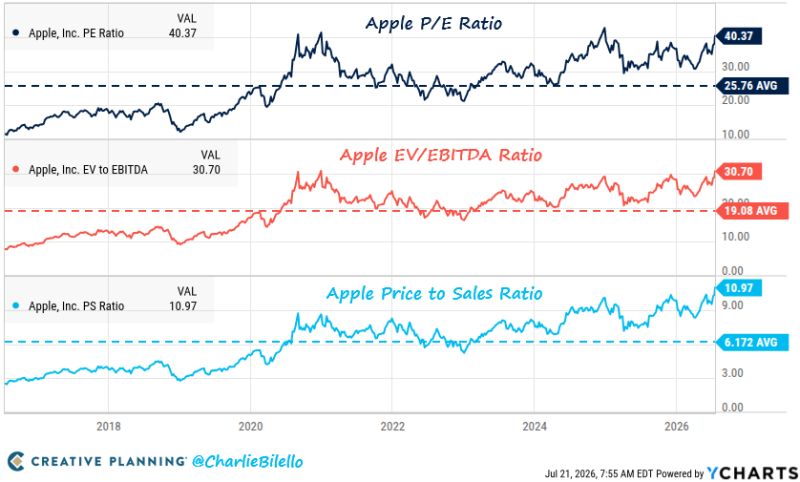

Apple's P/E Ratio: 40x ; 10-year average: 26x

Apple's EV/EBITDA Ratio: 31x 10-year average: 19x Apple's Price to Sales Ratio: 11x 10-year average: 6x $AAPL Source: Charlie Bilello

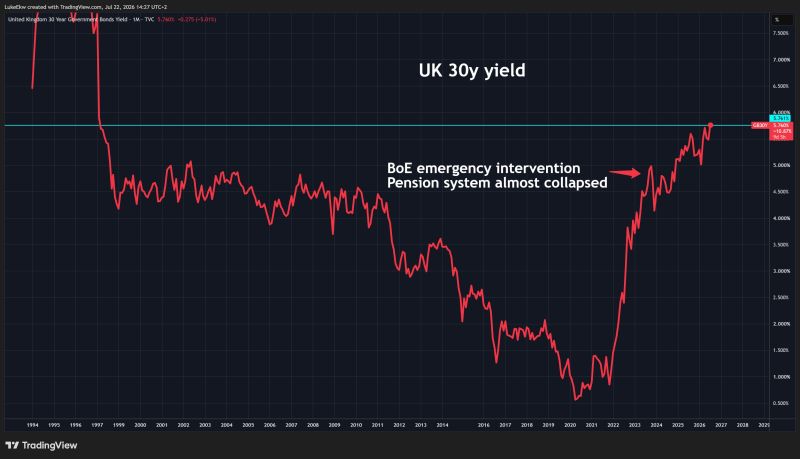

UK 30-year government bond yields have risen to the highest level in 3 decades.

From 2020-2026, they surged from 0.5% to 5.7%... UK pension funds are heavily exposed to Gilts and are suffering heavy paper losses Source: Lukas Ekwueme, Bloomberg

America isn't retiring anymore. It's working longer than ever

One in three Americans aged 55 and older is still working or looking for work, and that share has been climbing for nearly 40 years. The biggest change is among older workers: • Ages 65–69: participation has nearly doubled since the late 1980s, now above 30%. • Ages 70–74: from under 10% to almost 19%. • Ages 75+: participation has doubled to roughly 8%. The numbers are striking. Nearly 11.9 million Americans aged 65+ were employed last year, more than double the level of three decades ago. Between 2015 and 2024, the 65+ workforce expanded 33%, while the overall labor force grew by less than 9%. Longer life expectancy is part of the story. But so are disappearing pensions, rising living costs, and Social Security benefits that no longer stretch as far. Retirement is increasingly becoming a luxury rather than the default. Source: hedgeye

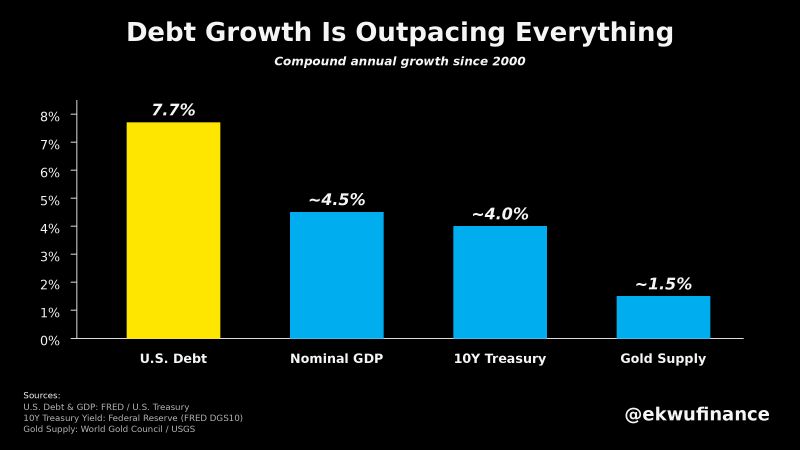

U.S. debt has been growing much faster than the economy for over two decades

Since 2000, U.S. debt has compounded at 7.7% annually, far outpacing nominal GDP (~4.5%) and the 10-year Treasury yield (~4%). Meanwhile, gold supply has expanded by only about 1.5% per year. For central banks, the contrast is striking: one asset becomes increasingly abundant as debt issuance accelerates, while the other remains structurally scarce. That helps explain why many central banks have been steadily increasing their gold holdings in recent years. Source: Lukas Ekwueme @ekwufinance