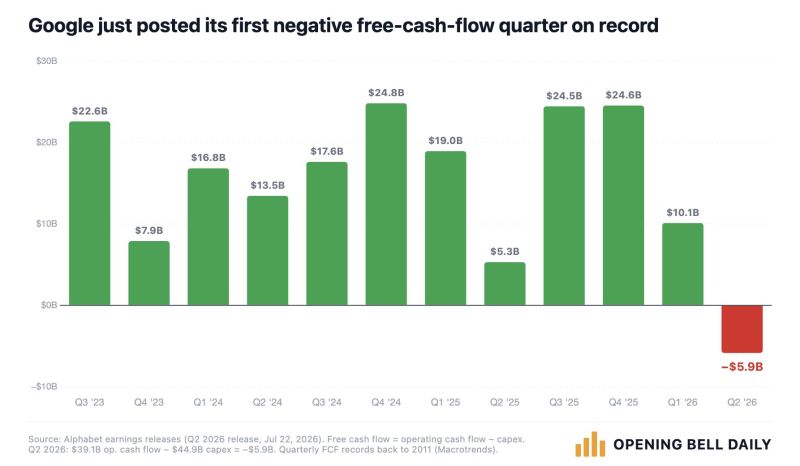

Alphabet $GOOG just reported NEGATIVE free cash flow for the first time in history.

And the story is not over; Alphabet projected full-year capital expenditures will be $195 billion to $205 billion in 2026, increasing its already sky-high spending estimate for the year as it works to secure an edge in the AI race. Source: Phil Rosen @philrosenn

Dell is up +11% today after Super Micro's record AI server orders boosted confidence across the entire sector.

$DELL has already built a $51.3 billion AI server backlog and raised its own revenue guidance to $60 billion. Its partnership with Nvidia gives it integrated AI infrastructure that larger enterprises are increasingly betting on. Source: Bull Theory

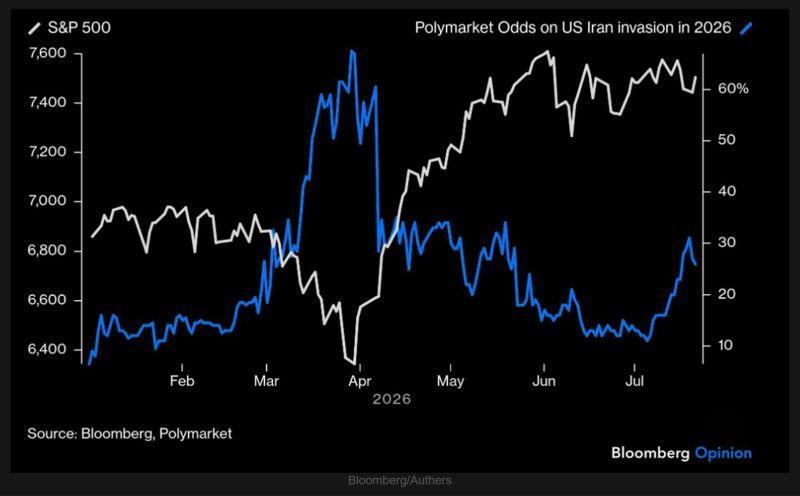

Prediction markets sharply lowered the perceived odds of a ground invasion, helping fuel a strong rally in the S&P 500.

Following conciliatory remarks from Iran and President Trump's announcement of a bombing pause earlier this year, investors concluded that neither side had the appetite for a prolonged ground conflict. Those odds have started to climb again, however, even as equities remain relatively resilient. Source: TME, Bloomberg/Authers

Andy Bechtolsheim wrote Google a $100,000 check before it even had a bank account.

That $100,000 check is worth $15 billion today. Andy Bechtolsheim is a billionaire German-American electrical engineer, investor, and tech entrepreneur. He co-founded Sun Microsystems in 1982 and Arista Networks in 2004. Source: Bull Theory

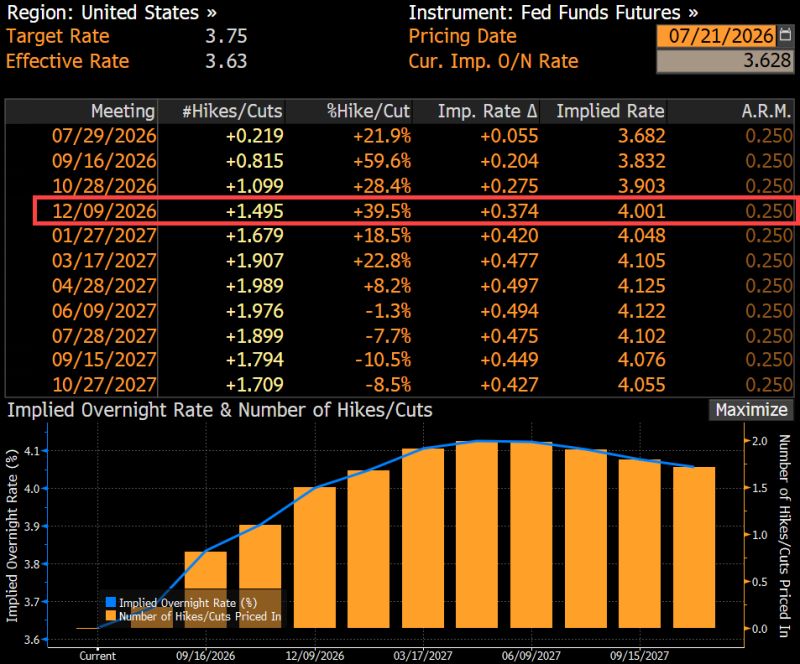

The futures market is now pricing 1.5 Fed rate hikes by year-end

Source: Hedgeye, Bloomberg

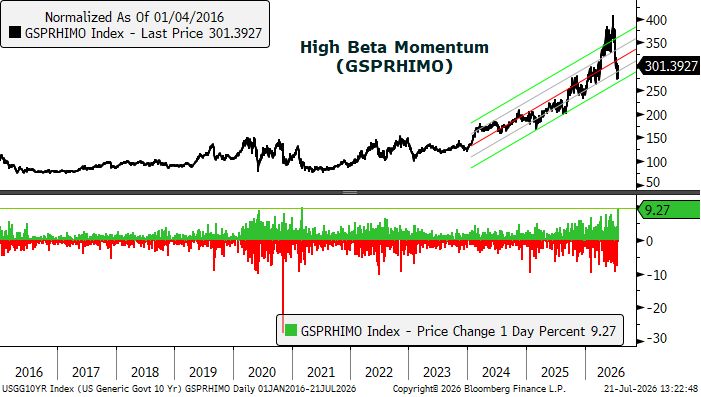

Momentum coming back to life:

"The GS High Beta Momentum Pair (GSPRHIMO) is up 9.3%, marking its strongest one day rally in the last five years following a 33% drawdown in the factor. Our sector specific TMT Unconstrained Momentum Pair (GSTMTMOM) is also posting its best day on record (+11.5%) and the GS Broad AI Pair (GSPUARTI) is up 7.3%, its best day since the launch of ChatGPT." - GS Source: Negligible capital

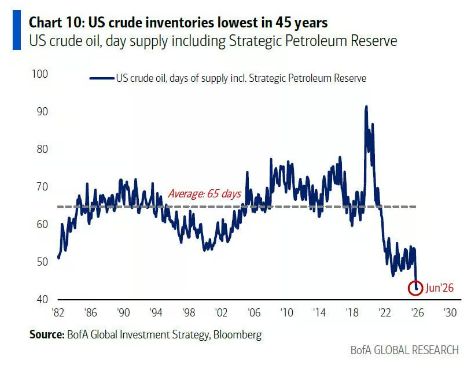

Crude Oil only has 43 days of supply left in the U.S., the lowest inventory in 45 years 🚨 🚨

Source: Barchart, BofA

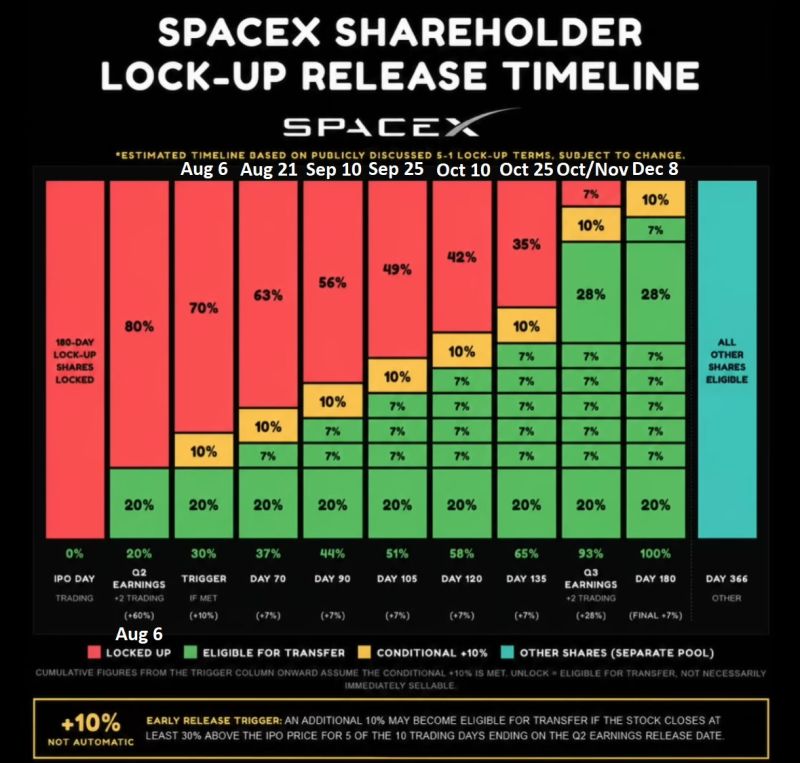

SpaceX $SPCX share unlock schedule ending at 100% December 2026.

Keep in mind only 5% of float is trading right now and most early investors bought for $0.02 - $1.22 per share. That's a lot of selling coming... Source. Financelot