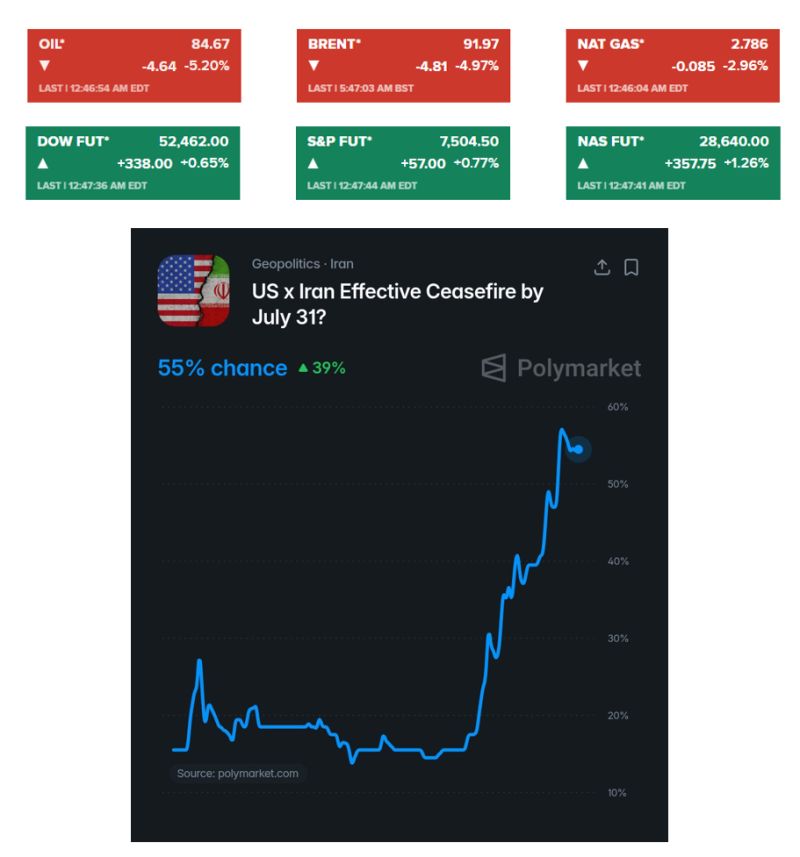

Oil slides 5% and US stocks indices futures jump as Iran reportedly signals halt to attacks if U.S. pause holds.

Iran has indicated it will stop carrying out attacks as long as the U.S. also refrains from striking, Reuters reported. There is now a 55% chance that the United States 🇺🇸 and Iran 🇮🇷 will sign a ceasefire this month, according to Polymarket traders Source: Evan, CNBC

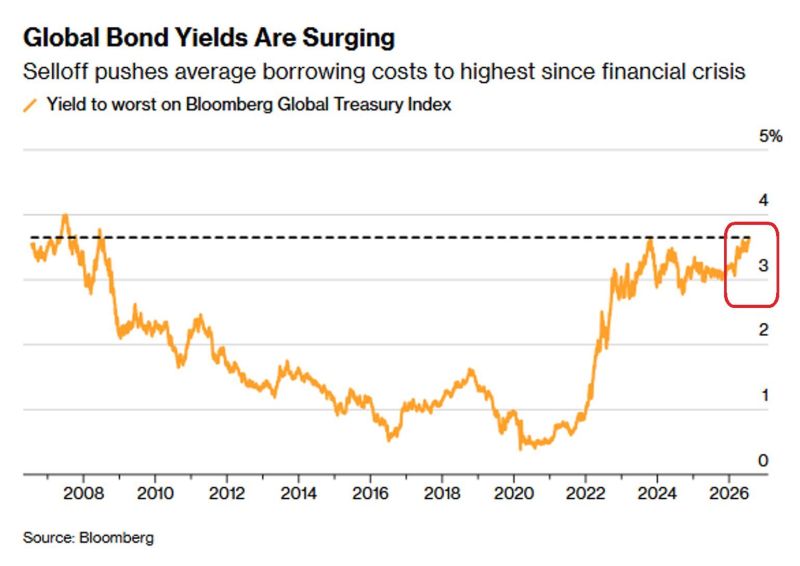

Global bond yields hit highest level since 2008

Source: Hedgeye, Bloomberg

WSJ: "Nvidia $NVDA is in talks to provide a roughly $250 billion backstop for OpenAI as part of a massive data-center project

It is one of the most ambitious financial transactions yet in America’s artificial-intelligence boom The guarantees from Nvidia would help the ChatGPT maker lease a 10-gigawatt project that SoftBank’s energy subsidiary is developing in southern Ohio, people familiar with the matter said. In total, the project could cost more than $500 billion, including the chips that would go inside the data centers. It would be the largest data-center project announced to date".

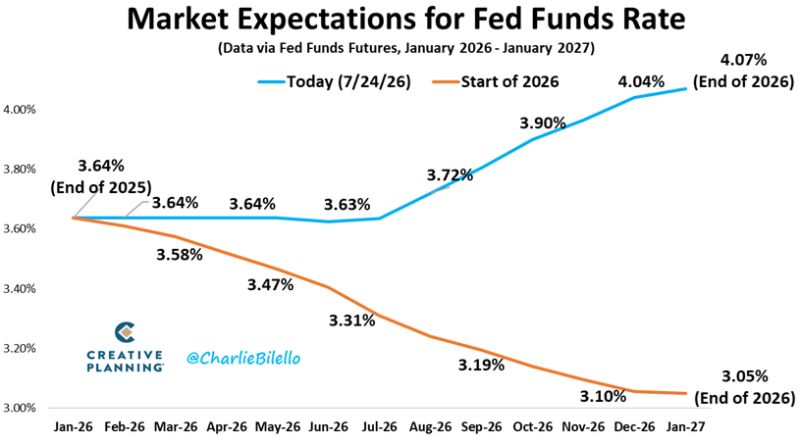

At the start of the year, the bond market was pricing in 2 Fed rate CUTS.

Today it's pricing in 1 to 2 Fed rate HIKES. That's a 1% swing in expectations. Source: Charlie Bilello

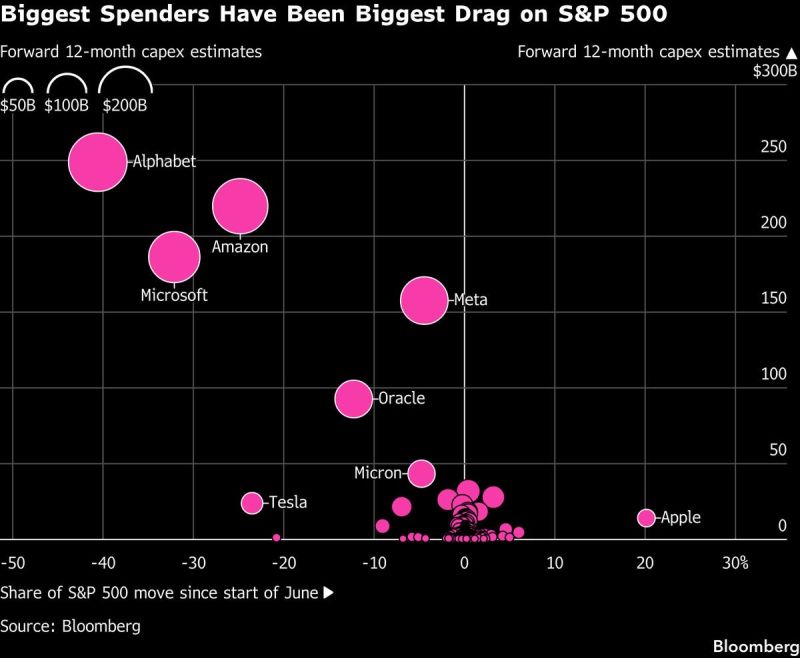

Biggest spenders have been biggest drag on S&P 500 since the start of June.

The chart below shows contribution to SPX declines versus 12 month capex estimates. Apple is the outlier. Tim Apple is leaving the company on a high note. It takes a lot of discipline not to follow the crowd - undoubtedly part of the reason why Buffett loves him. Source: Bloomberg, Negligible Capital

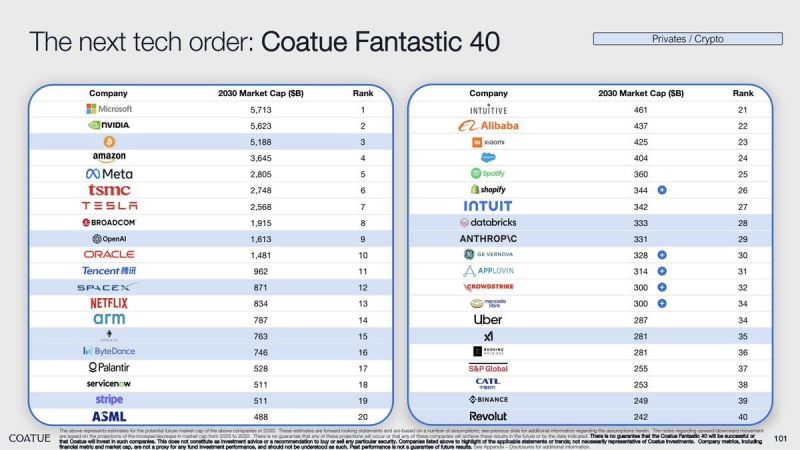

A little over one year ago, Coatue released a 100-page keynote presentation on the evolving technology landscape across public & private companies.

They predicted these 40 companies will be the largest by market cap in 2030. Note the absence of Alphabet $GOOG $GOOGL Source: Koyfin @KoyfinCharts

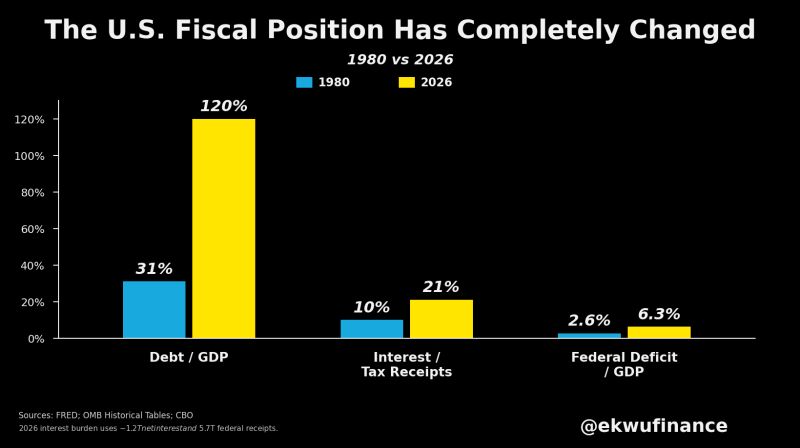

Stephen Warsh can sound like Volcker. The US fiscal position means he can't easily govern like Volcker.

The backdrop has completely changed: • Debt-to-GDP: 31% in 1980 → ~120% today • Interest costs: 10% → 21% of federal tax receipts • Budget deficit: 2.6% → 6.3% of GDP That leaves the Fed facing a much tougher trade-off than it did in the early 1980s. Raise rates aggressively to crush inflation, and you risk destabilising the Treasury market and sharply increasing government financing costs. Prioritise financial stability instead, and inflation remains higher for longer, putting continued pressure on the US dollar. The Volcker playbook was built for a very different fiscal world. Today's debt burden makes every rate decision far more consequential. Source: Lukas Ekwueme @ekwufinance

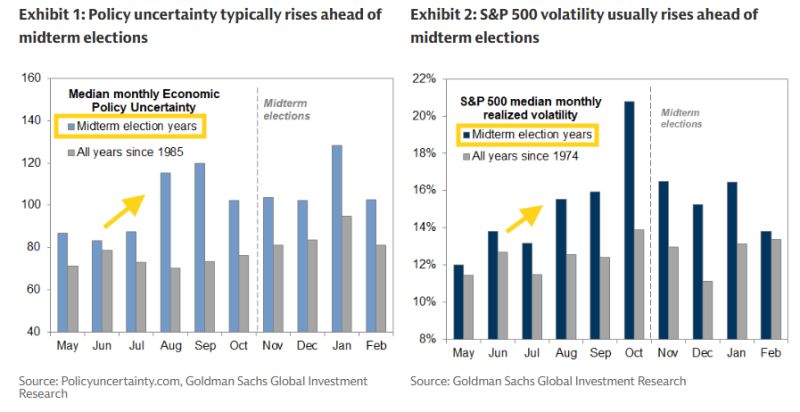

Goldman: With the 2026 midterms three months away, investor focus is likely to turn increasingly to elections in coming weeks. Midterm elections will take place this year on November 3.

During the last few decades, economic policy uncertainty and equity market volatility have typically begun to rise in the late summer ahead of midterm elections. Our economists have found the same pattern after adjusting for the economic cycle as measured by the unemployment rate. Source: Goldman Sachs, Neil Sethi on X