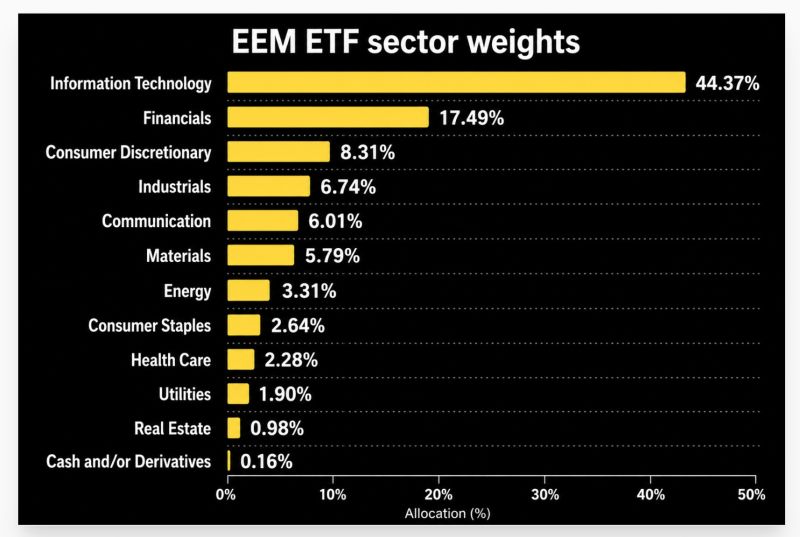

The King of Tech... $EEM iShares Emerging Markets ETF isn't what it used to be.

Many still view it as a commodities and old-economy EM trade, but the ETF has quietly evolved into a tech beast driven by semiconductors and AI-related exposure. Source: TME, Bloomberg

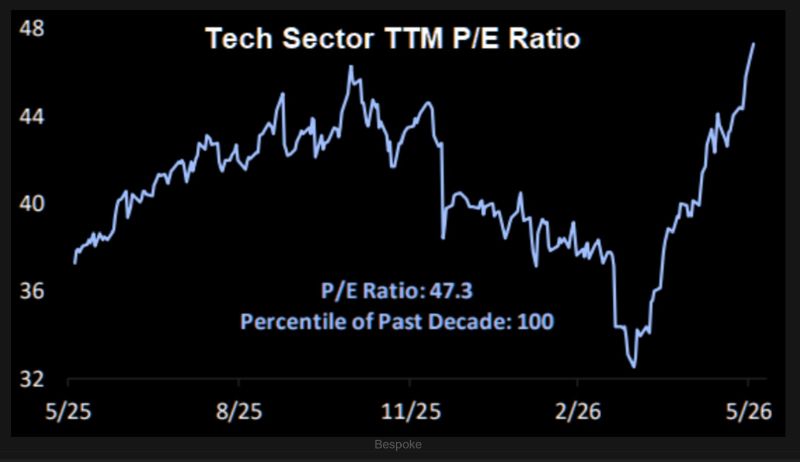

That was quick... The S&P Tech sector's trailing 12-month P/E ratio has jumped from roughly 32 to 48 since the 3/30 low.

Source: TME

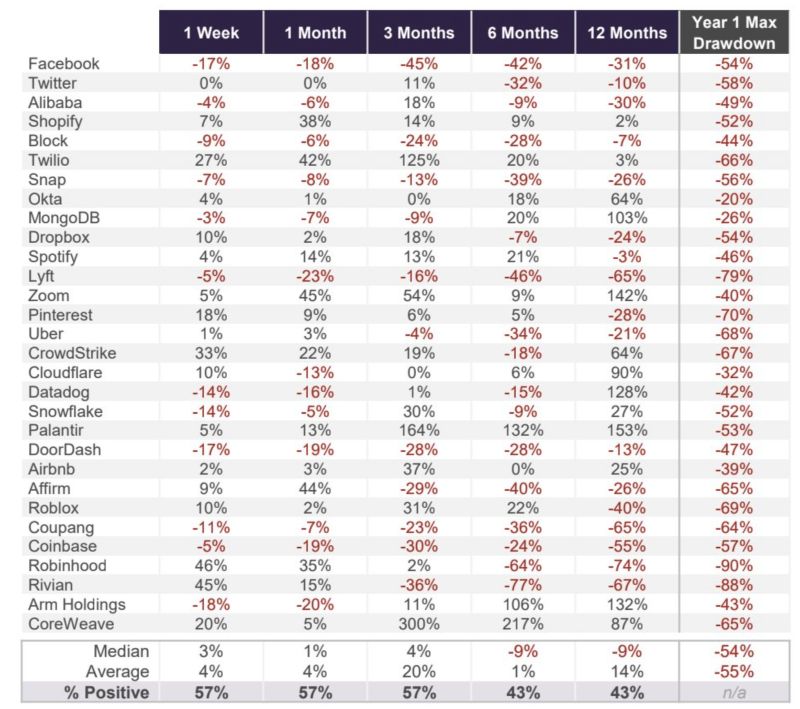

Moral of the story - do NOT chase hot IPO

Year-1 average drawdown = 55% Year-1 median drawdown = 54% Table: Truist Source: Puru Saxena

Victoria’s Secret just posted its best quarter in years — and the stock exploded 47% after-market.

Just four years ago, the company looked dead. Its entire brand was built around fantasy-driven marketing and supermodel runway shows — a formula that dominated for decades but eventually lost touch with what women actually wanted. Sales collapsed from $7.51B in 2020 to $6.18B in 2023. The annual fashion show was scrapped. Wall Street had completely written the company off. The turnaround ultimately came down to one thing: bras. CEO Hillary Super rebuilt the business around new bra launches, focusing on the category that drives the highest repeat purchases and the strongest customer lifetime value. When customers buy bras, they come back more often — and spend more across every other category. The results have been dramatic. Q1 2026 revenue reached $1.56B, up 15% YoY. The company swung from a $2M loss to a $48M profit in just 12 months. Management also raised full-year revenue guidance from $6.85B to $7.13B. Two years ago, investors thought Victoria’s Secret was finished. Today, the stock hit an all-time high. Source: Bull Theory

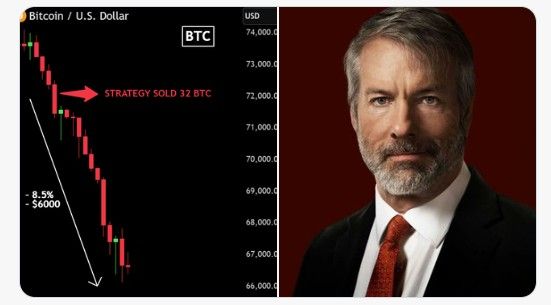

Bitcoin has fallen $6,000 since Michael Saylor's STRATEGY disclosed its first Bitcoin sale in 3.5 years.

More than $2.41 billion in crypto positions have been liquidated in just 48 hours. STRATEGY currently holds 843,706 BTC, acquired for $63.9 billion at an average price of $75,699 per Bitcoin. The last time Saylor sold Bitcoin in December 2022, BTC went on to rally 660% from $17,000 to $125,000. Source: Bull Theory

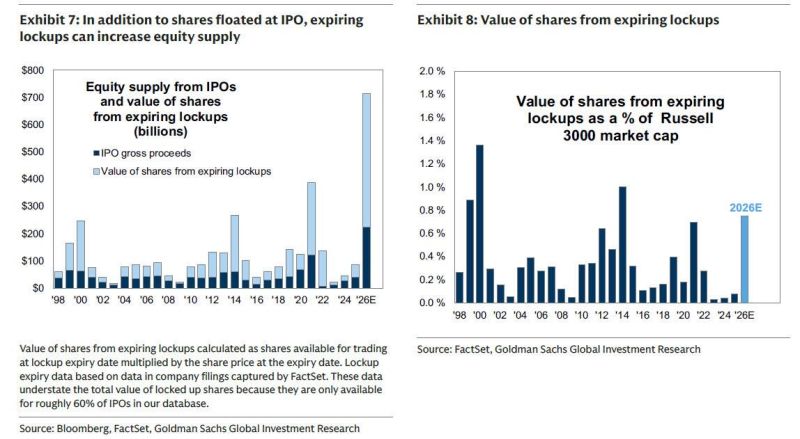

Beware of the increase in equity supply... It’s not just the IPOs. It’s the coming wave of lockup expirations too

Source: Goldman Sachs, zerohedge

ALPHABET $GOOGL MANDATORY CONVERTIBLE STOCK SALE IS SAID TO BE OVERSUBSCRIBED

ALPHABET $GOOGL MANDATORY CONVERTIBLE STOCK SALE IS SAID TO BE OVERSUBSCRIBED Source: Wall St Engine

Japan's NIKKEI has surpassed 68,500 for the first time in history.

The NIKKEI is now up 36.5% in 2026, adding ¥365,000,000,000,000 ($2.5 trillion) in market value. Source: Bull Theory