Siegfried Back on an Important Level

Siegfried (SFZN SW) is currently retesting the July 2024 breakout level at 943.50, which was also the 2021 top. The stock has also entered a strong demand zone between 917-991. Keep an eye on the price action over the next few days for potential opportunities. Source: Bloomberg

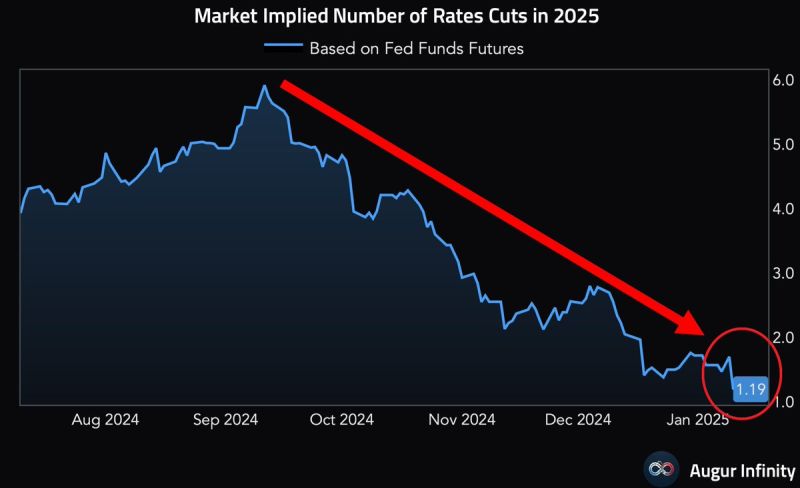

⚠️The market is pricing in just ONE Fed rate cut for 2025. This is down from nearly 5 rate cuts expected in September.

Great Chart: @AugurInfinity, Global Markets Investor

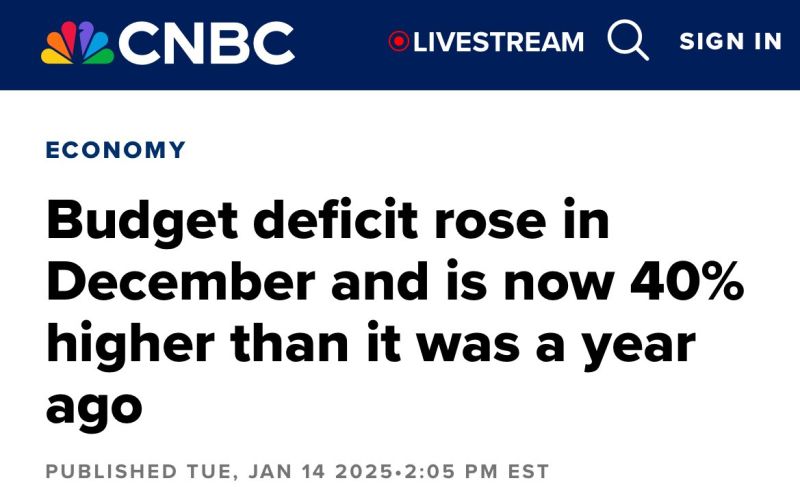

The first quarter of FY 2025 produced a deficit of $710.9 Billion.

That’s $200B more than the first quarter of fiscal 2024, or a 39% increase YoY. The US is now running a ~$3 TRILLION annual deficit...

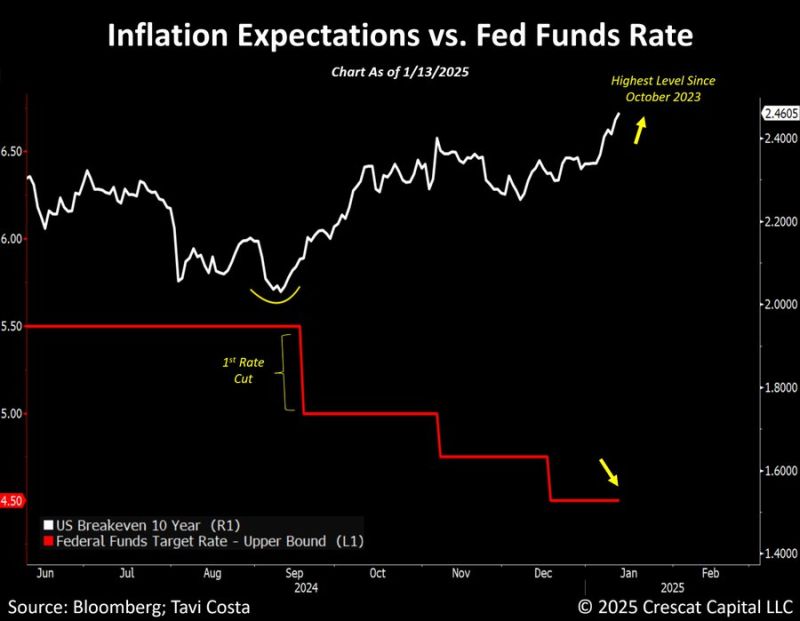

Inflation expectations have almost perfectly bottomed exactly when the Fed started to cut rates.

10-year breakeven rates are now at its highest level since October 2023. As highlighted by Tavi Costa, this is a reminder that when debt limits a monetary authorities actions, inflation becomes the path of least resistance. Source: Tavi Costa, Bloomberg

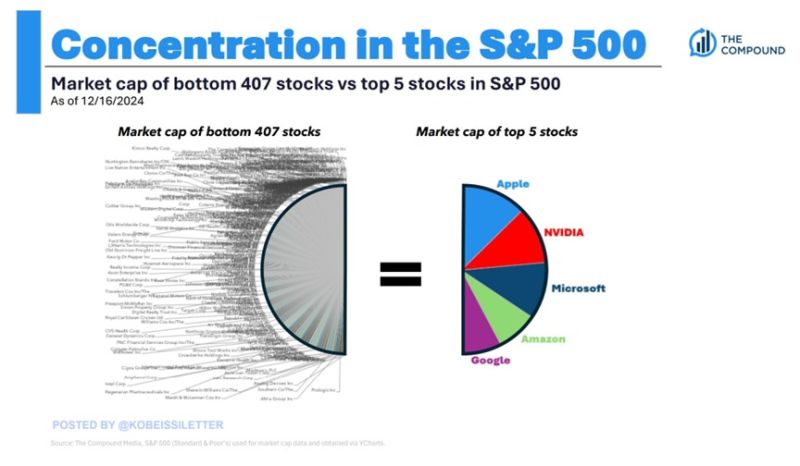

Shocking stat of the day: The market cap of the SP500’s top 5 stocks is now equal to the size of the bottom 407 stocks.

Apple, $AAPL, Nvidia, $NVDA, Microsoft, $MSFT, Google, $GOOGL, and Amazon, $AMZN are worth now a combined $15.3 trillion. These companies have added $5 TRILLION in market value since the beginning of last year. To put this into perspective, these 5 stocks are worth now nearly as much as China and Hong Kong's stock markets COMBINED. The top 5 companies reflect a record 24% of the entire US stock market cap. Source: Compound, The Kobeissi Letter

🚨US PPI DATA SHOULD PLEASE POWELL! December US PPI annual inflation rises 3.3%, below expectations for 3.5%.

vCore PPI inflation increased 3.5% Y/Y, compared to forecasts for a gain of 3.8%. BULLISH🚀 YoY Growth: 🇺🇸 PPI (Dec), 3.3% Vs. 3.5% Est. (prev. 3.0%) 🇺🇸 Core PPI, 3.5% Vs. 3.8% Est. (prev. 3.4%) MoM Growth: 🇺🇸 PPI (Dec), 0.2% Vs. 0.4% Est. (prev. 0.4%) 🇺🇸 Core PPI, 0.0% Vs. 0.3% Est. (prev. 0.2%)

Real yields on 30-year US treasury bonds are now at 2008 levels.

It seems that bond markets are worried about much more than just inflation... Source: Adam Kobeissi, Bloomberg

⚠️Bank of Japan is getting closer to deliver another rate hike:

Inflation has picked up while wages have jumped to the highest level in at least 3 DECADES. The market is pricing in about a 60% probability of a hike next week, and an 82% chance by March. Remember when in August 2024 the market flash crashed by suddenly waking up to BOJ's rate hikes? This is key to watch. Source: The Kobeissi Letter, The Daily Shot