On the other side of the world, China’s economic signals are shifting.

While trade dynamics fluctuate, attention is turning to its energy position. Estimates suggest China holds roughly 1.4 billion barrels in oil reserves—enough to cover about six months in a worst-case disruption scenario . At the same time, efforts by BRICS nations to move away from the U.S. dollar in oil trade have made limited progress, with the dollar still dominating global transactions. China has long relied on discounted oil imports from countries like Iran and Venezuela, but geopolitical pressures may complicate that strategy. Amid global tensions and proxy conflicts, the broader strategic rivalry between the U.S. and China remains a defining theme. Source: NY Times, Rothmus on X

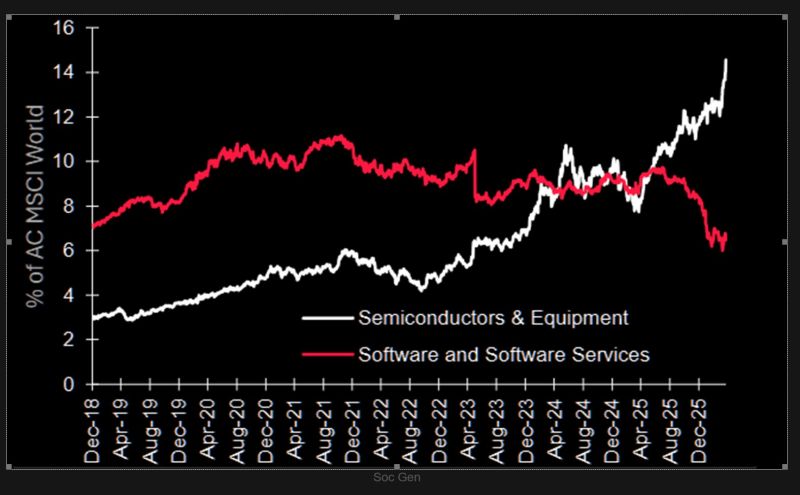

Semiconductors now represent almost 15% of AC MSCI World market capitalisation and are now the largest sector overall.

Source: SocGen, TME

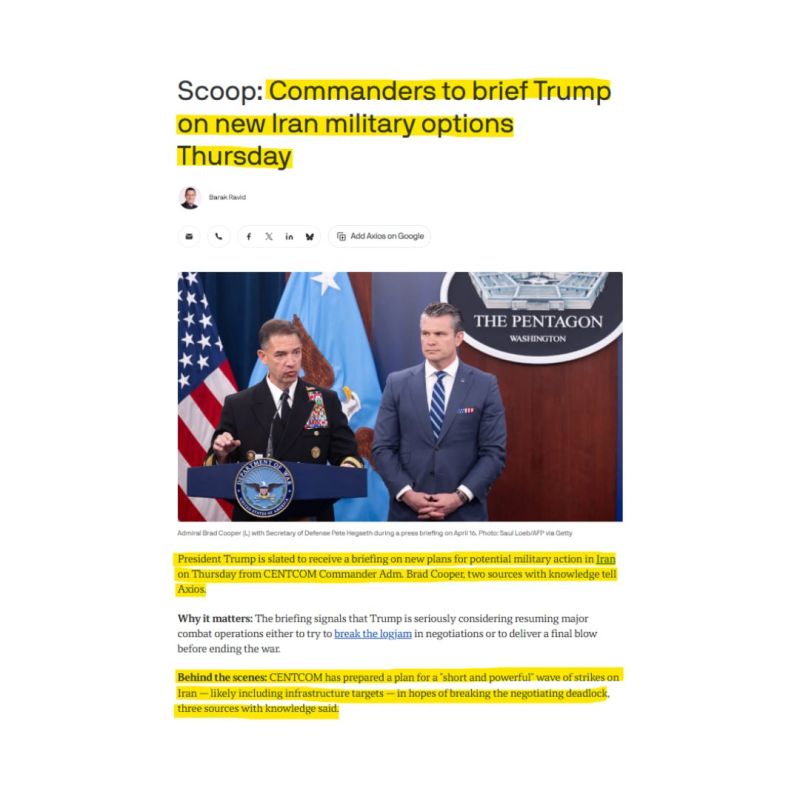

Trump to be briefed on new military options for Iran.

CENTCOM Commander Brad Cooper is set to present updated plans for potential military action, per Axios. The briefing signals the US is weighing a return to major combat operations amid stalled negotiations. Options under consideration include escalation to break the deadlock or delivering a decisive strike before ending the conflict. Source: Bull Theory Activate to view larger image,

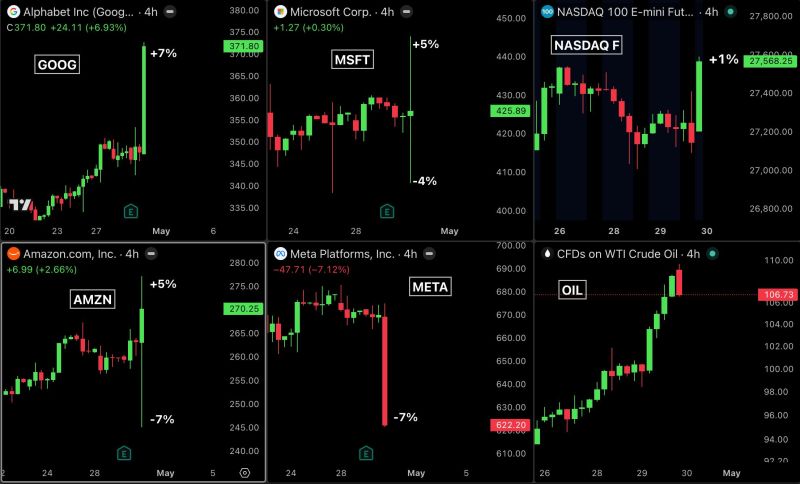

The "MAGNIFICENT 7" just reported the biggest revenue surge in stock market history.

Google nearly doubled what Wall Street expected. EPS came in at $5.11 against an estimate of $2.63, a 94% beat. Revenue hit $109 billion against an estimate of $107 billion. $GOOG jumped 7% and hit a new all time high. Microsoft beat every expectation. EPS of $4.27 against an estimate of $4.06. Revenue of $82 billion against an estimate of $81 billion. $MSFT gained 5%. Amazon had one of the biggest EPS beats of any company its size in years. EPS of $2.78 against an estimate of $1.64, a 70% beat. Revenue of $181 billion against an estimate of $177 billion. $AMZN dropped 7% immediately after the report and then fully recovered to close up 4%. Meta beat every single number Wall Street had. EPS of $10.4 against an estimate of $6.82, a 52% beat. Revenue of $56 billion against an estimate of $55 billion. $META dropped 7% anyway. Source: Bull Theory

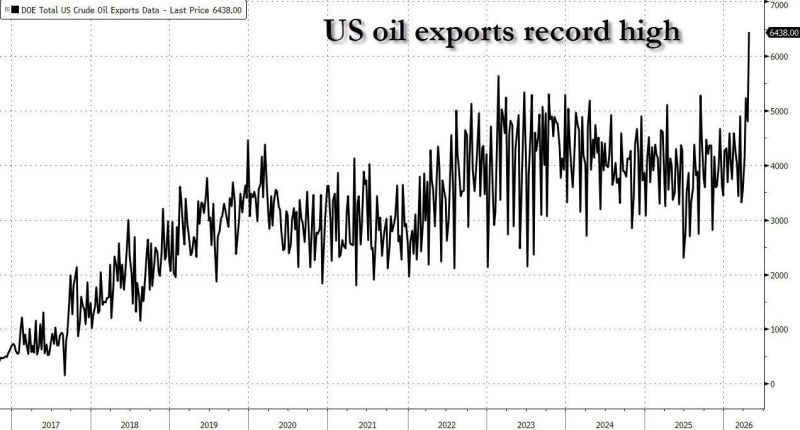

US oil exports soared to a record 6.4 million barrels last week. Out of the US SPR... and to foreign buyers

Source: zerohedge

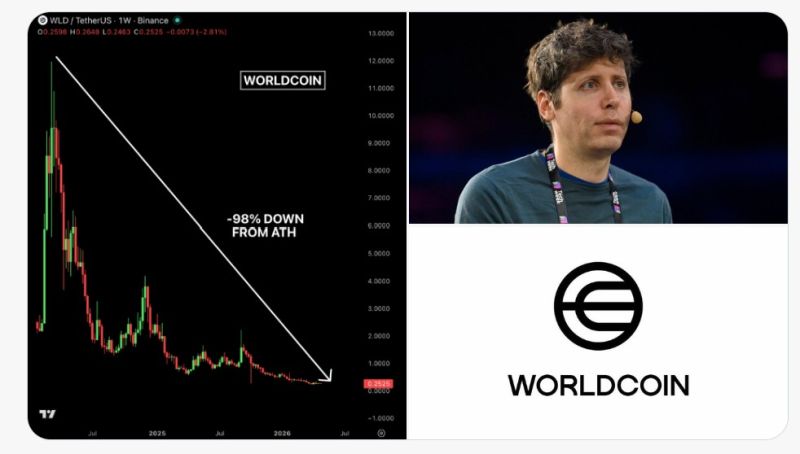

Sam Altman’s Worldcoin ($WLD) has lost about 98% of its value, turning a $100,000 investment at its peak into roughly $2,000.

The project’s “Orb” device, which scans irises in exchange for tokens, raising concerns about permanent biometric data collection and consent—echoed by Edward Snowden and researchers like MIT. It highlights regulatory pushback and bans across multiple countries. Some are pointing out that the project’s team of selling large amounts of tokens while supply increases, contributing to price decline, and portrays broader ethical and legal concerns around the project.

US economic data keeps surprising to the upside, while European data keeps surprising to the downside.

That gap just keeps growing, according to Bloomberg economic surprise indexes. Source: Bloomberg, Lisa Abramowicz

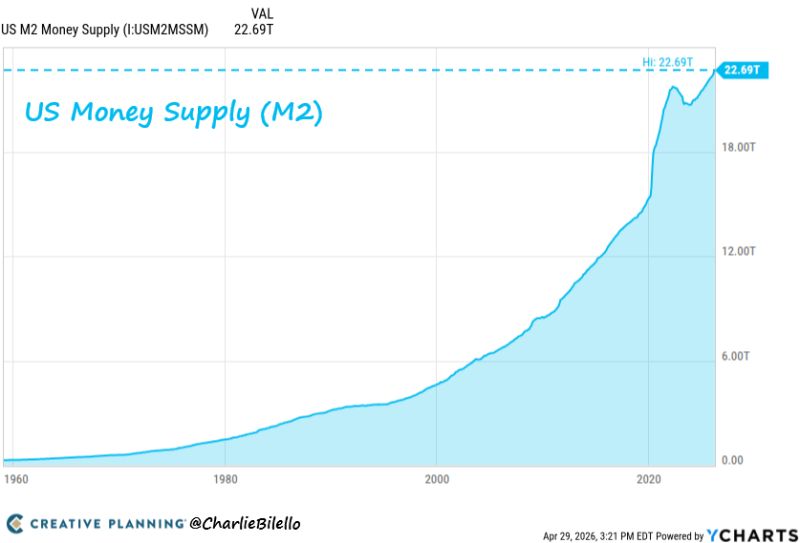

The Fed expanded the money supply by nearly $9 trillion under Powell.

Inflation has averaged >4% per year over the past 6 years. Powell's explanation? It was nearly all due to rolling “supply shocks" over which the Fed has no control. The truth: this inflation was made in Washington as it always is - from too much government borrowing/spending and too much government creation of money. Source: Charlie Bilello