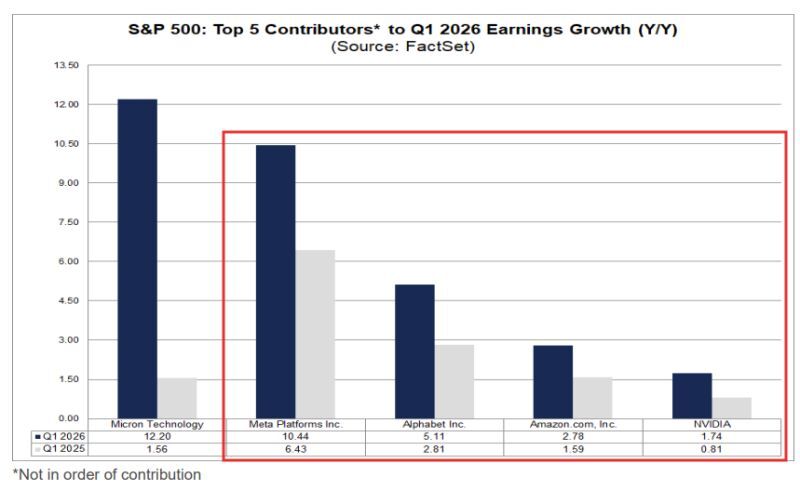

Factset notes that Mag-7 GAAP earnings growth for Q1 is now expected to come in at an astounding +61.0% up from 22.4% at the end of the quarter

(March 31st) with 4 of the top 5 contributors to SPX earnings growth coming from this cohort (Alphabet, NVIDIA, Amazon and Meta, the other is Micron) That said, Factset notes that the three of those who have reported though each were boosted by one-time non-cash items: "The (GAAP) EPS actual for Alphabet for Q1 2026 included a net gain of $37.7 billion primarily due to net unrealized gains on non-marketable equity securities. The (GAAP) EPS actual for Amazon.com for Q1 2026 included pre-tax gains of $16.8 billion included in non-operating income from investments in Anthropic. The (GAAP) EPS actual for Meta Platforms for Q1 2026 included an $8.03 billion income tax benefit." Source: Factset, Neil Sethi

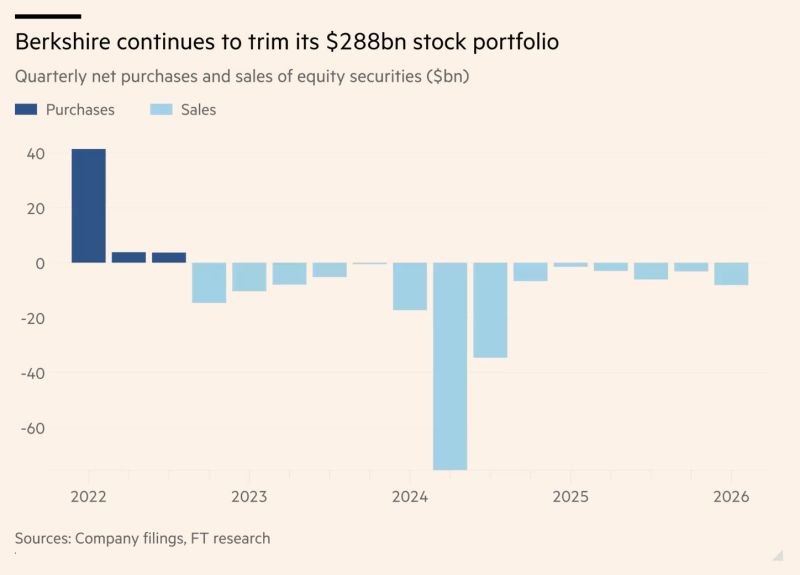

Berkshire Hathaway $BRK.A has now dumped stocks for 14 consecutive quarters, the longest selling streak in its history

Source: Barchart, FT

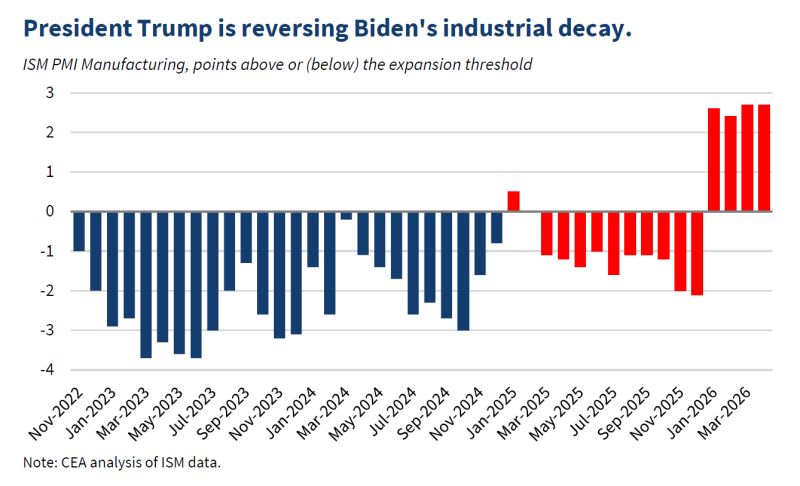

There is a manufacturing boom underway in America.

Source: Anthony Pompliano

World's Most Cash Rich Companies

Source: The Market Mind

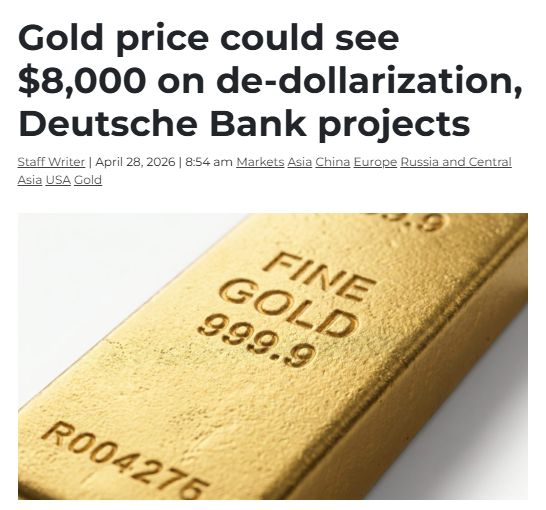

The German investment bank said it sees a scenario where central banks continue to increase their gold holdings as a financial safety net to protect themselves from Western sanctions.

These central banks have added over 225 million ounces to their reserves since the 2008 financial crisis, while their holdings of US dollars have fallen from a peak of over 60% in the early 2000s to about 40% today. Gold’s share of global central bank reserves could reach 40%, up from 30% currently, the bank predicts. At that allocation, Deutsche Bank ran a simulation that projects gold prices to hit $8,000 an ounce within five years, a near 80% rise on current levels. Source: Wall Street Mav

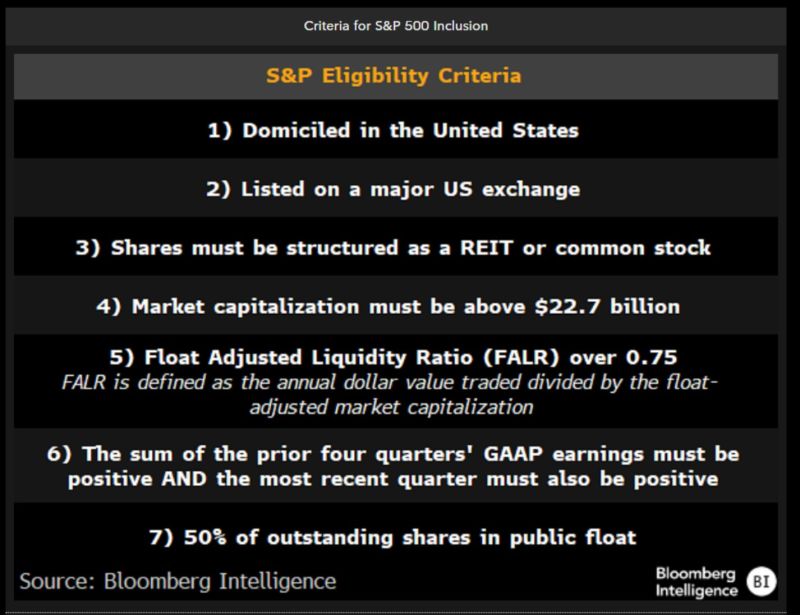

S&P is considering rule changes that would let newly public companies join its indexes faster with Nasdaq weighing a similar move.

The shift could pull index demand forward for mega IPOs like SpaceX, OpenAI, Anthropic & Databricks. Current requirements for S&P 500 inclusion include the following, including positive GAAP earnings for the last 4 quarters AND the most recent quarter must also be positive, something SpaceX, OpenAI, and Anthropic all definitely do not have currently. Source: Negligible Capital, Bloomberg Intelligence

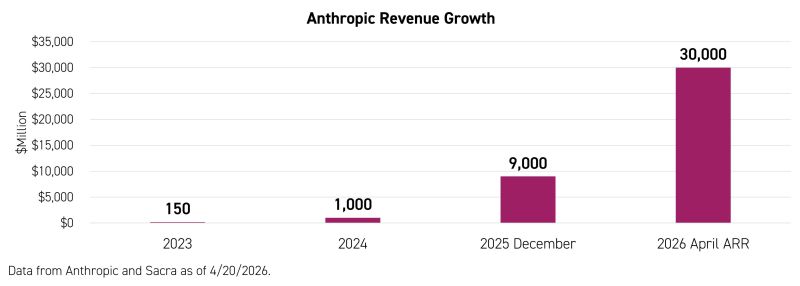

Anthropic Triples Revenue Forecast in Four Years

Source: Hedgeye

⚠️ CHINA JUST MADE IT ILLEGAL TO FIRE EMPLOYEES AND REPLACE THEM WITH AI.

China’s courts have ruled that companies cannot fire or penalize employees simply because AI can replace their work. In two cases, employers who cut pay or terminated workers due to AI adoption were found to have acted illegally. The courts stated AI adoption is a voluntary business choice, so companies must retrain, reassign, or support workers instead of shifting the burden onto them. This contrasts with global trends, where over 1.5 million jobs have been cut since 2020, many due to AI. Major firms like Amazon, Block, and Meta have reduced staff to fund AI investments. Studies warn AI could replace significant portions of the workforce, reducing consumer spending. Economists highlight a risk: widespread layoffs shrink demand, creating a self-destructive cycle where productivity rises but consumers lack income. China’s approach aims to prevent this by protecting workers’ earnings and sustaining economic demand.