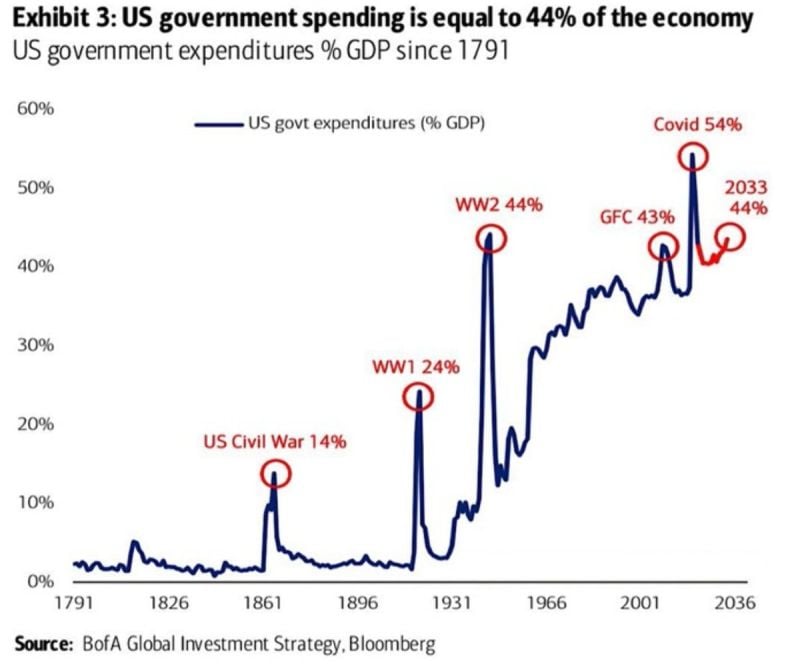

US GOVERNMENT SPENDS MONEY AS IF THERE IS A CRISIS:

US government spending as a % of GDP is now ~43%, in line with THE GREAT FINANCIAL CRISIS. This is just 1 % below World War II levels. Only the COVID crisis saw higher expenditures as a share of GDP of 54%... Source: BofA, Global Markets Investor

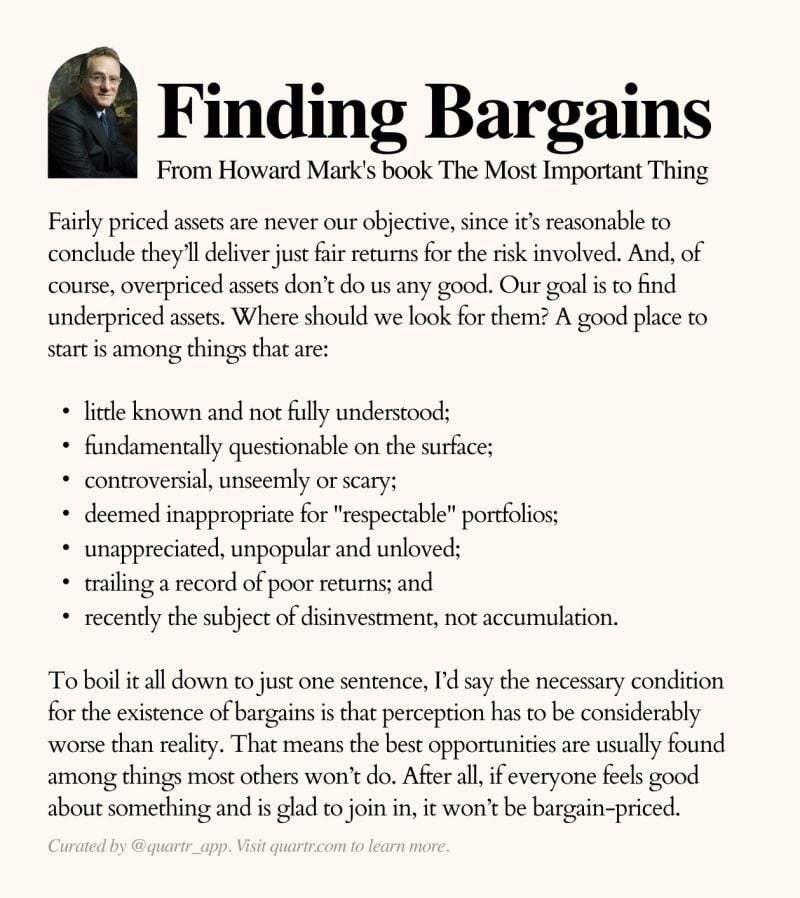

Howard Marks' checklist for finding bargains by Quartr

.

The star of the show this week and it's not even close.

Highest one-week return since January and now green on the year. $TSLA Source: Trend Spider

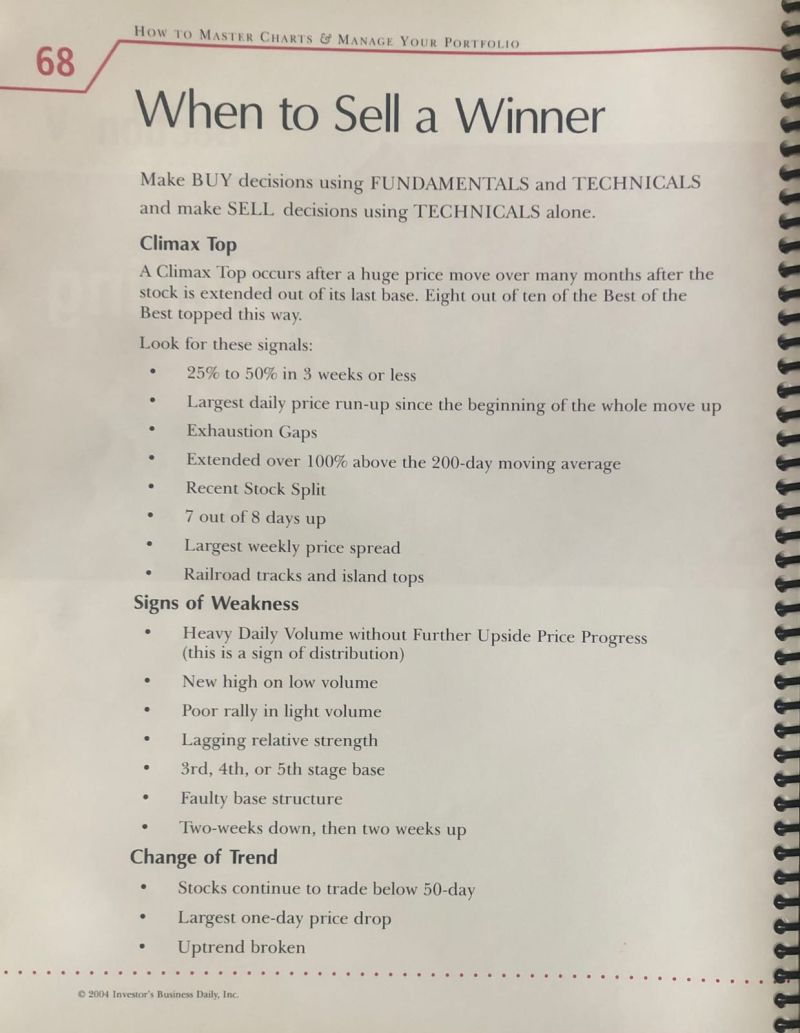

Probably one of most difficult question to answer for portfolio managers... WHEN TO SELL A WINNER?

Source: Marketr rebellion

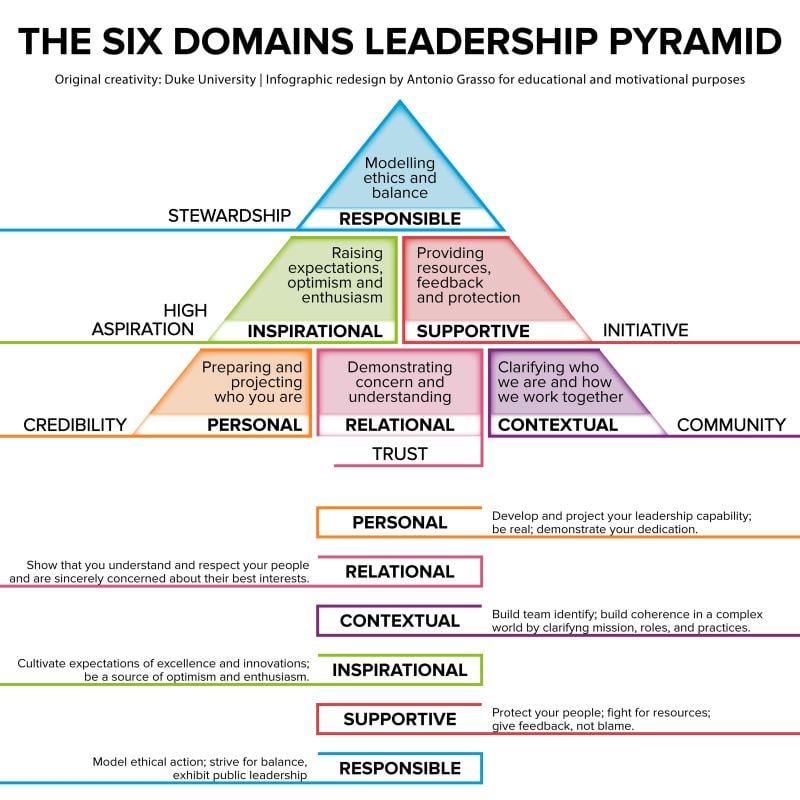

Duke University thru agrassoblog.org:

The 6 domains leadership pyramid or where to focus to become an effective leader

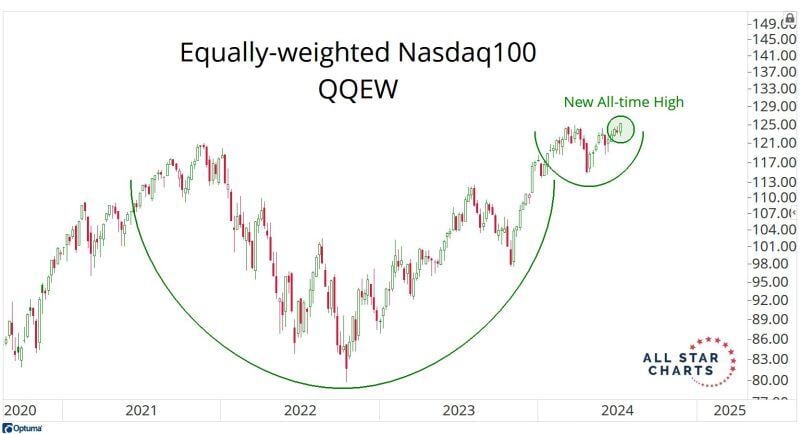

The US equities market explained in one image

Source: Trend Spider

Can it really be only 7 stocks if the equally-weighted index with 100 stocks in it just went out at new all-time highs?

Source: J-C Parets, https://allstarcharts.com/

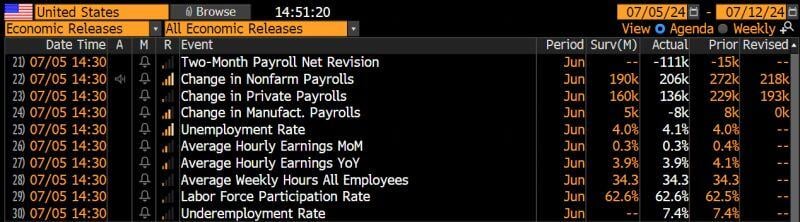

Latest US jobs numbers show economic momentum keeps cooling: Non-farm-payrolls rose by 206k jobs in June, ahead of 190k forecast.

However, 2 months net revisions were NEGATIVE with -110k. Moreover, government employment rose by a whopping 70k while PRIVATE employment with 136k was below estimates. Unemployment rate rose to 4.1% from 4.0% due to higher labor participation rate. Wage rose 3.9% YoY in line w/estimates. Bottom-line: these numbers seem to confirm our thesis that the US job market is NORMALIZING hence reinforcing the disinflation trend which will ultimately enable policy makers to NORMALIZE. More to come from our Chief Economist Adrien Pichoud... stay tuned... Source: Bloomberg, HolgerZ