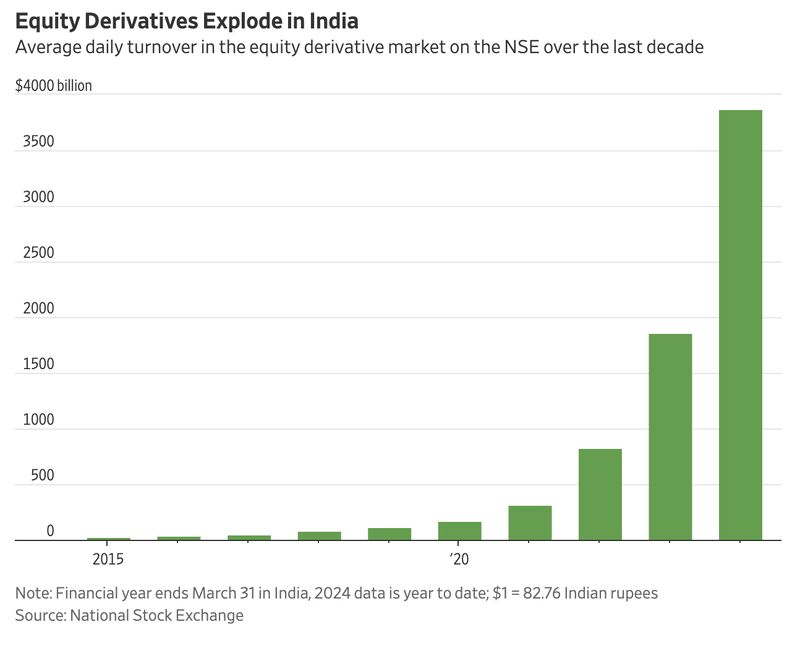

78% of equity options throughout the world were traded in India last year.

Look at this growth since the onset of Covid! Source: Barchart

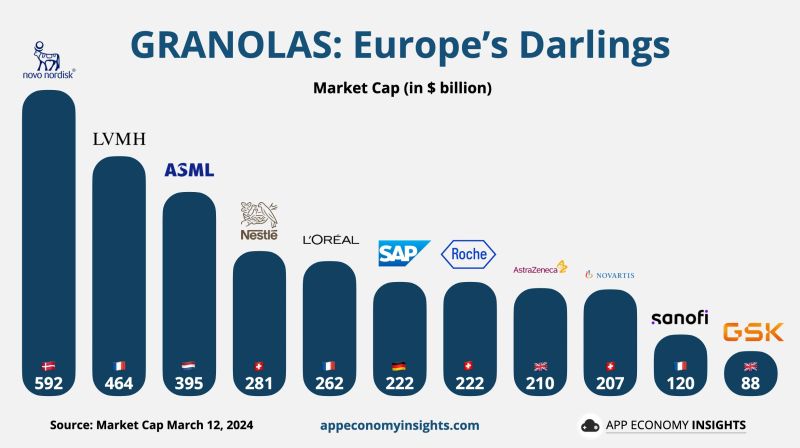

Who are Europe's GRANOLAS?

Novo Nordisk $NVO LVMH $LVMUY ASML $ASML Nestlé $NSRGY L'Oréal $LRLCY SAP $SAP Roche $RHHBY AstraZeneca $AZN Novartis $NVS Sanofi $SNY GSK $GSK Source: App Economy Insights

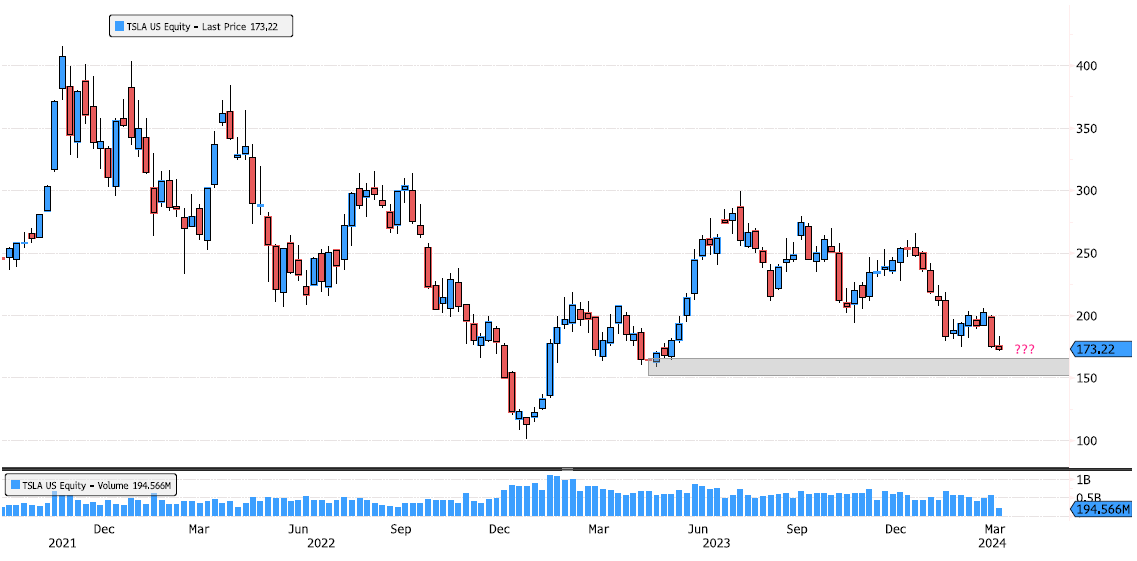

Tesla reaching strong support zone

Tesla (TSLA US) is approaching support zone 152.37 - 165.65. Keep an eye for any reaction over the next few days. Source : Bloomberg

More crypto rich...

According to a report by Kaiko Research, BTC’s latest rally is creating about 1500 millionaire wallets daily. However, despite the increase in Bitcoin (BTC) millionaire wallets, Kaiko Research notes that the number of millionaire wallets created daily during the 2021 bull run was closer to 4000, more than double the current number. According to Kaiko Research, low millionaire wallets could be due to the lack of new capital. The report notes, ‘In 2021, there was a huge influx in capital as all manner of bull sought to benefit from the crypto hype. This time around, whales could be taking a more cautious approach, waiting to see if the gains have legs before investing.‘ https://lnkd.in/eabkjiHh

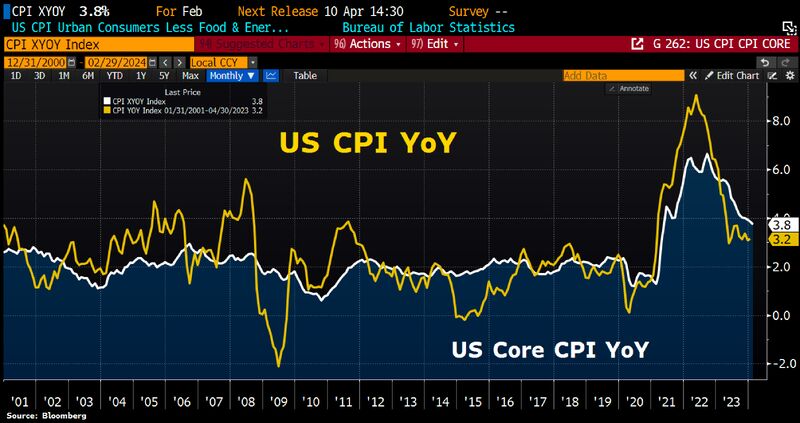

US inflation looks sticking, at least decline in the US headline CPI is stalling since Jun 2023.

In Feb, CPI rose by 0.4%MoM, both overall & excluding energy & food. Prices for services in particular increased, reflecting rising wage costs. High inflation rate in Jan was not an outlier. Source: Bloomberg, HolgerZ

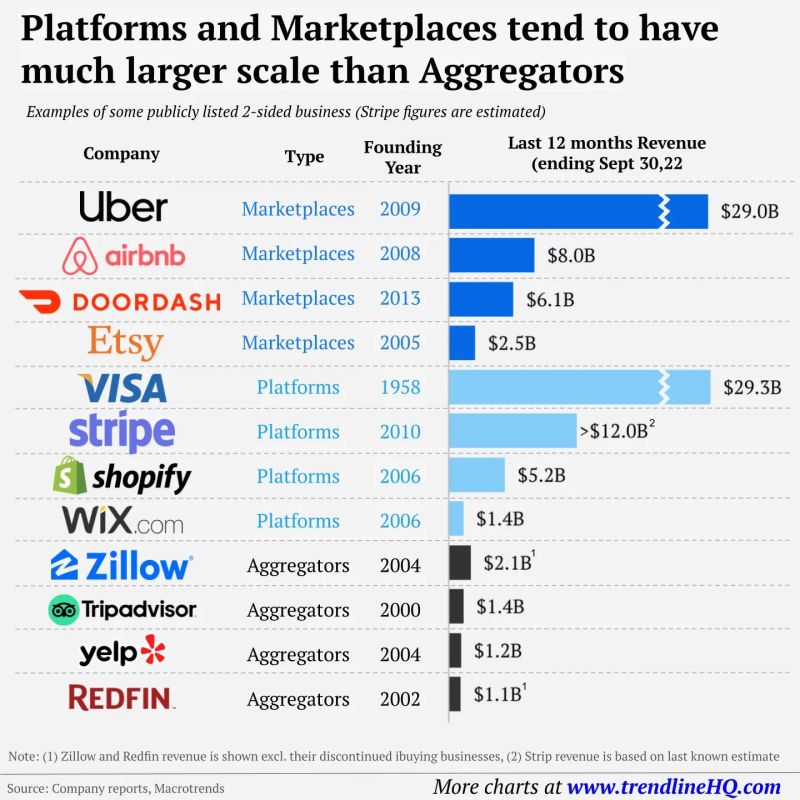

What's the difference between a marketplace, an aggregator, and a platform? A lot...

Source: CJ Gustafson

ING Group breakout after 23 years ?

ING Group (INGA NA) broke yesterday February 2022 high ! It is also breaking the 2001 downtrend line ! Keep an eye

Semiconductor stocks have reached their highest valuation compared to the S&P 500, exceeding the levels seen during the dot-com bubble peak.

source : bloomberg