In Case You Missed It: On February 8th the Wall Street Journal reported that OpenAI CEO Sam Altman wants to raise up to $7 trillion

For a “wildly-ambitious” tech project to boost the world’s chip capacity, funded by investors including the U.A.E. — which in turn will vastly expand its ability to power AI models. To put numbers in perspective: $7 TRILLION is around ~10% of global GDP…Or the combined market cap or BOTH Microsoft & Apple. That means he wants to totally reshape the global semiconductor industry. By the way, where will all the energy needed come from? Source: VB, Creative Capital, WSJ

BREAKING: ETFs are buying 12.5x more bitcoin per day than $BTC network can produce

Source image: Motley Fool, BITCOINLFG

Meme Stock Anniversary

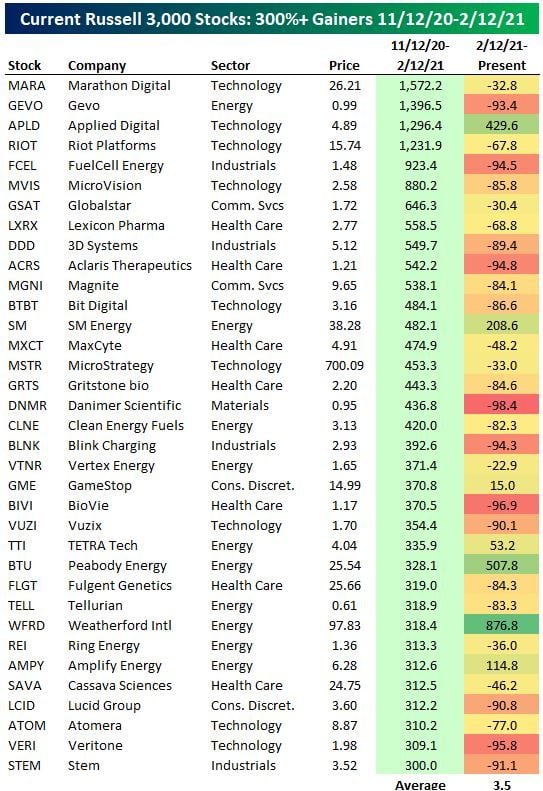

Three years ago today, the "meme-stock mania" that saw hundreds of profitless stocks surge hundreds of percent in a matter of months hit its ultimate peak. In the three months leading up to February 12th, 2021, the average stock in the Russell 3,000 (current members) rallied 40%, but there were 178 stocks that saw three-month rallies of more than 100%, 35 stocks that rallied 300%+, and four stocks that rallied over 1,000%. Below is a table of the 35 stocks currently in the Russell 3,000 that rallied 300%+ in the three months leading up to 2/12/21( include also how each of these stocks has performed since 2/12/21) source : bespoke

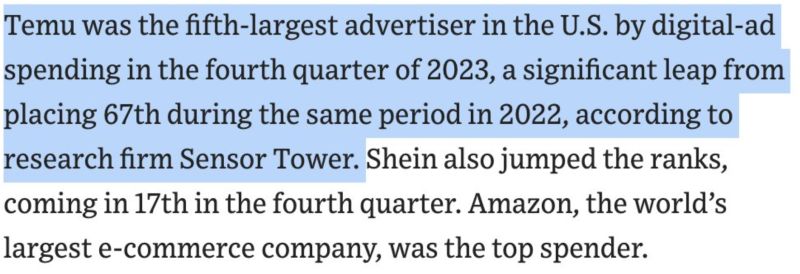

The Spend, Spend, Spend Strategy..

Temu is going all in on Marketing (including in this Sunday’s Super Bowl) Marketing spend: • 2023 - $1.7 billion • 2024 - $3 billion (est.) source : wsj

Has the fed won the party?

US Medium-Term Inflation Expectations Lowest in 11 Years of Data – Source: Bloomberg

THE SILENT BULL MARKET...

Japanese stocks index Nikkei 225 closes up 1066.55 points and within striking distance of all time high 38957! It briefly crossed the 38,000 mark for the first time since the asset bubble burst in 1990 as it rallied about 3% and pushed 34-year highs. In times of financial repression aka negative real rates, real assets go up. January PPI came weaker than expected (+0.0% m/m vs. 0.1% expected) Futures going higher still: Nikkei 38110 Source chart: IG

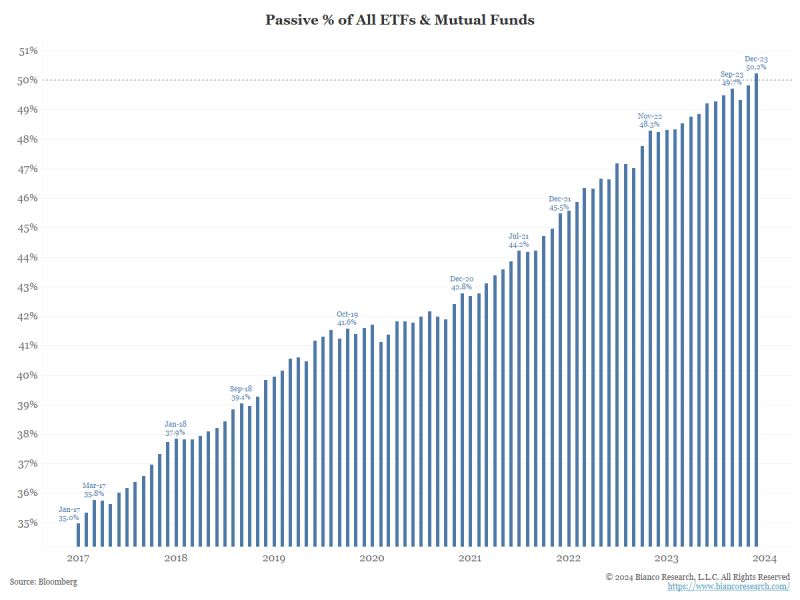

According to Bloomberg's estimates, passively managed money just exceeded 50% of all assets.

Money management just crossed the Rubicon. Source: Bianco Research

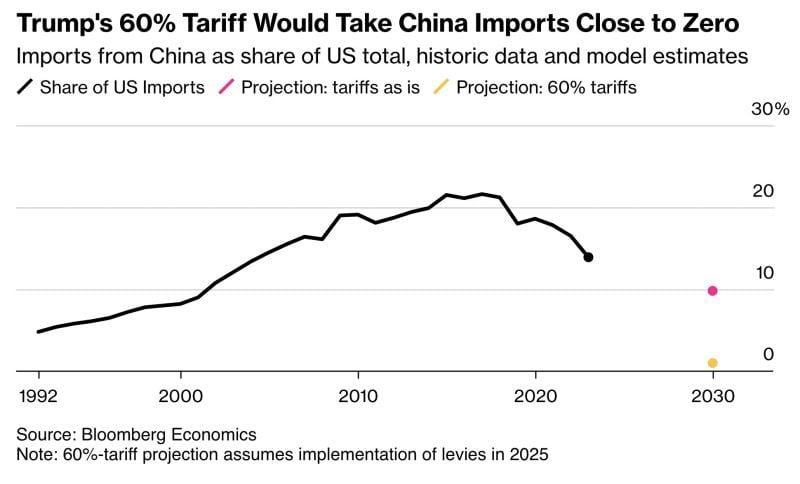

Donald Trump is pitching a 60% tariff on all Chinese imports.

That would shrink a $575bn trade pipeline to practically nothing, Bloomberg analysis shows. For China ’s economy and its slumping stockmarket — down >40% from its 2021 high — that’s bad news. Worse, Trump’s rhetoric may add pressure on Biden to take harsher measures in the run-up to election day Source: HolgerZ, Bloomberg