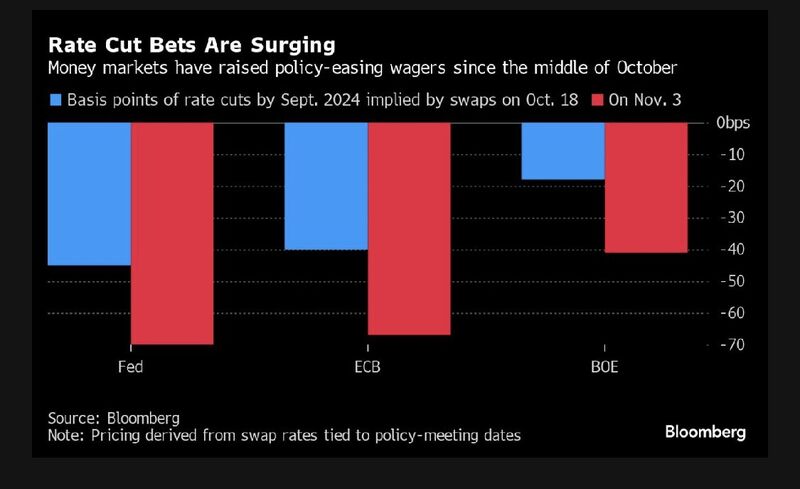

Markets are now betting on big rate cuts next year

This chart shows that money markets have raised policy-easing wagers since the middle of October: by September 2024, the FED should have cut by 70 basis points, the ECB by 65 basis points and the BoE by 40 basis points. (pricing is derived from swap rates tied to policy-meeting dates) Source: Bloomberg

Key Events This Week:

1. Fed Chair Powell Speaks - Wednesday 2. Initial Jobless Claims - Thursday 3. Fed Chair Powell Speaks - Thursday 4. Consumer Sentiment data - Friday 5. ~10% of S&P 500 reports earnings this week 6. Total of 12 Fed speaker events All attention remains on the Fed. Source: The Kobeissi Letter

Central Banks around the world are now cutting rates at the fastest pace in more than 3 years

When will the U.S. follow suit? Source: Barchart, BofA

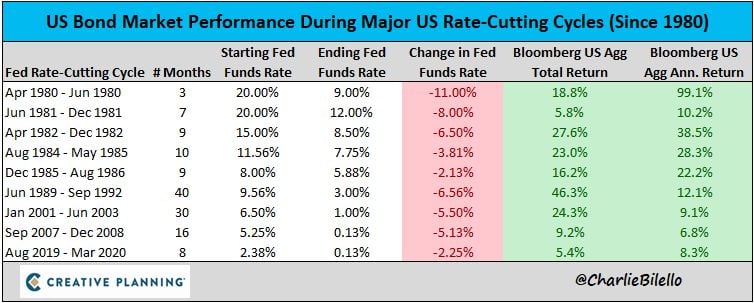

The Fed is now expected to start cutting rates in May 2024

Here's how bonds have performed during prior rate-cutting cycles... Source: Charlie Bilello

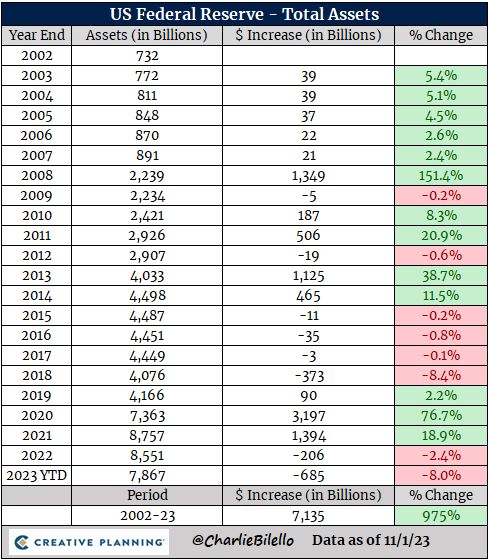

The Fed's balance sheet hit its lowest level since May 2021 this week, down $1.1 trillion from the peak in April 2022

Annual changes in the Fed's balance sheet since 2002 by Charlie Bilello

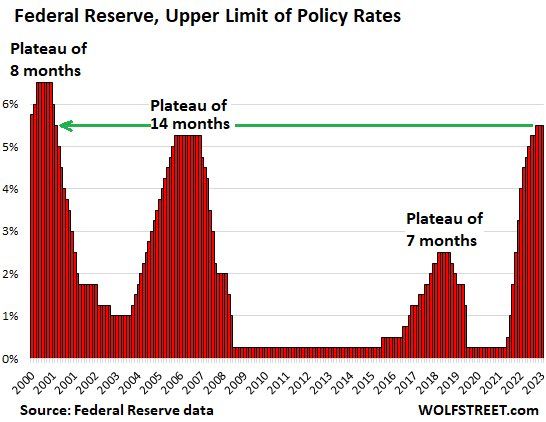

The end of the rate hikes is typically followed by plateaus before rate cuts begin

The end of the rate hikes may not be here yet, and the Fed has already said a many times for months that the plateau is going to be “higher for longer". How long will the plateau be this time? Source: Wolfstreet

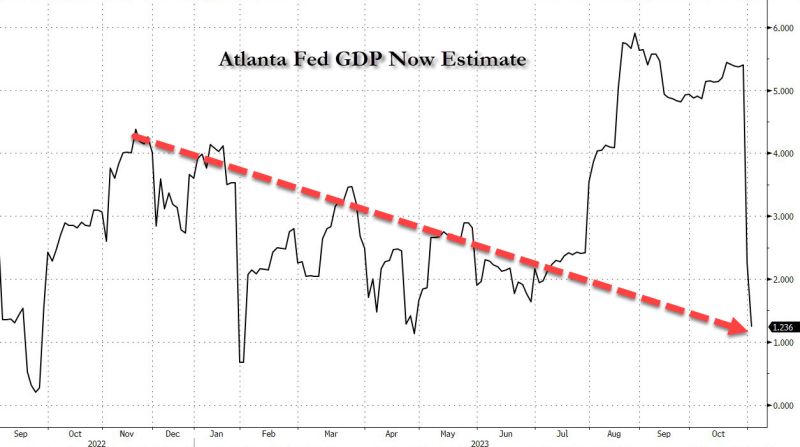

And we're back to Bidenomics trendline

Source: www.zerohedge.com

No change as expected

Nothing really new except that they acknowledge strong growth and strong wage gains versus September, effectively upgrading their economic assessment. This is the 3rd time they upgrade their view on growth. Our view is unchanged: we are due for a long pause. High rates is the new normal.