France’s Interior Minister Gerald Darmanin said the minimum wage could be increased, opening the door to a key proposal of the leftist bloc

Raising the floor on the basic wage known as the SMIC by around €200 ($217.64) to €1,600 a month net is a core proposal of the New Popular Front, which won the largest share of seats in a snap election two weeks ago, but not enough to govern alone. Source; Bloomberg

Since its inception in 1999, the Euro has lost 40% of its purchasing power.

To put this into perspective: 1 Euro today can only purchase about 60% of what it could back in 1999. Source: Relai 🇨🇭

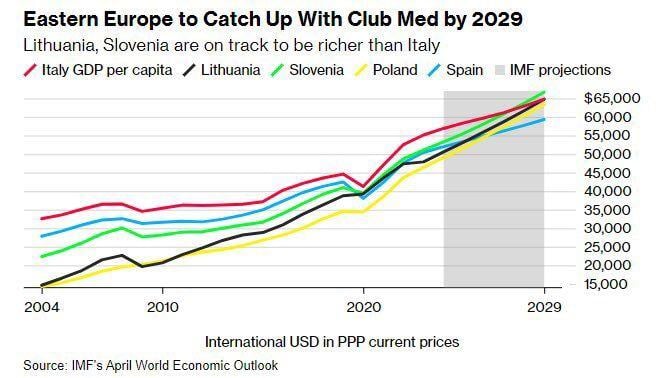

What is happening in Poland is nothing short of economic wonder.

Standard of living in Poland overtaking Spain and Italy within just one generation is amazing. Source: Michel A.Arouet, IMF

In Germany, the number of corporate insolvencies up by a third.

In April 2024, the local courts reported 1,906 corporate insolvencies. The courts put the creditors' claims from the corporate insolvencies reported in April 2024 at ~€11.4bn. In April 2023, the claims had totaled ~€1.3bn. Source: HolgerZ, Bloomberg

A storytelling chart about Europe

thru Michael A. Arouet, FT

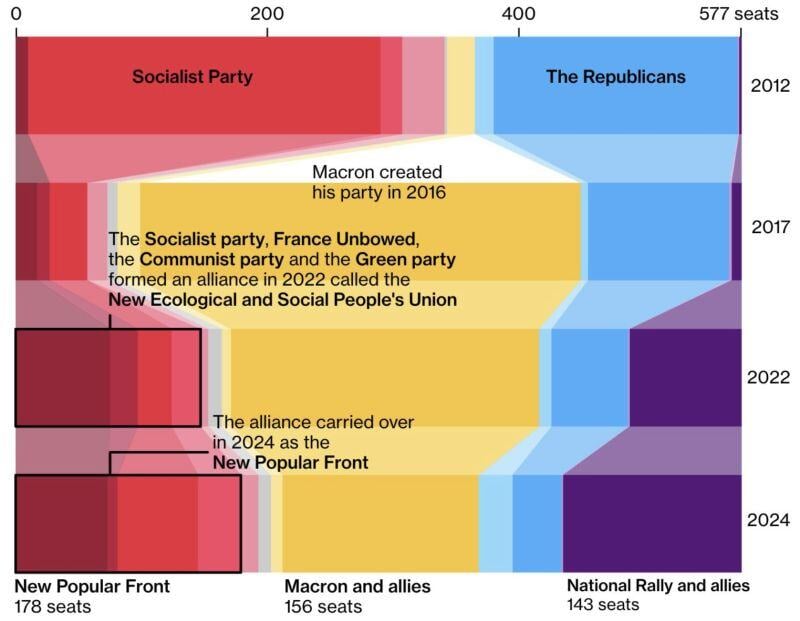

Macron’s Rise and Fall in one chart: at first, he kicked out opposition coming from the traditional right and left parties.

Fast forward to 2024 and the parliament is in gridlock with Macron's Renaissance being stuck between left and far-right. French assets could feel more pressure in the near-term -- even in the case of a hung parliament -- after the Nouveau Front Populaire came out on top in a second round of parliamentary elections. Its fiscal expansion and anti-business program could push the French-German yield spread back toward 80-85 basis points and weigh on all companies with a large exposure to hashtag#France. Source: Bloomberg

Great column in the FT

France and Britain are changing places "Britain and France are sitting on opposite ends of a political see-saw. Three days after the UK elected a pragmatic, centrist government with a huge majority, France went to the opposite extreme. Sunday’s legislative elections have produced a deadlocked parliament, with both the far right and the far left gaining ground. (...) Relief that the far-right Rassemblement National performed worse than expected in the second round of voting cannot disguise the fact that the centre ground in French politics is shrinking — and with it the authority of President Emmanuel Macron. The calm of London on election night last week contrasted strongly with the fevered atmosphere in Paris on Sunday evening. (...) it may be many months before France has a government that is capable of delivering a coherent response on European questions. That will be a problem, not just for Britain but for the whole of the EU," LINK TO THE ARTICLE >>> https://lnkd.in/eaMy_zCQ

The far-right RN was defeated yesterday but the problem is far from over.

They got 37% of the popular vote. 37% !! The "winning left" got 26%... Note 2 things: 1) The specificities of the French lower house voting system: One party rises from 33% to 37% between the 2 rounds and move from rank #1 to rank #3. Another one (left / far left) declines from 28% to 25% a move from rank #2 to rank #1 2) If you take out far-right RN and far-left/left, the true "traditional / establishment" parties are less than 30% of votes... (despite unprecedented turnout) Source image: JohannesBorgen