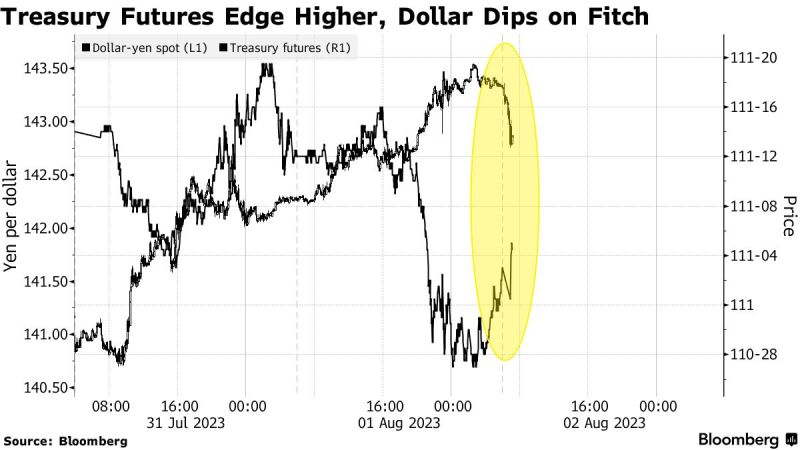

BREAKING: Fitch downgrades the United States' long-term credit rating from AAA to AA+

Fitch says that "repeated debt-limit political standoffs and last-minute resolutions" are to blame. They note that debt-ceiling standoffs have "eroded" confidence in fiscal management. Source: The Kobeissi Letter, Bloomberg

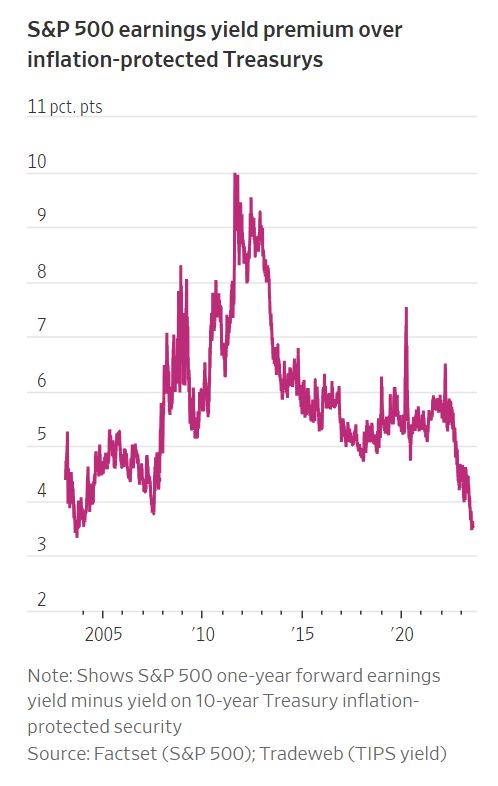

Bonds are looking the most attractive vs stocks in decades, according to one metric

The gap between the earnings yield of the S&P 500 and the yield on the 10-year Treasuries dropped to around 1.1 percentage point last week, its narrowest since 2002. Source: Lisa Abramowicz

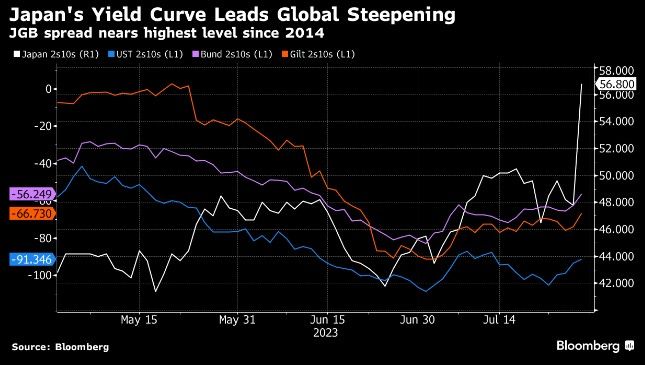

🌎 Global yield curve steepening gained momentum last week as a sign that major central banks are nearing the end of their tightening cycles

Source: Bloomberg, Fast reveal

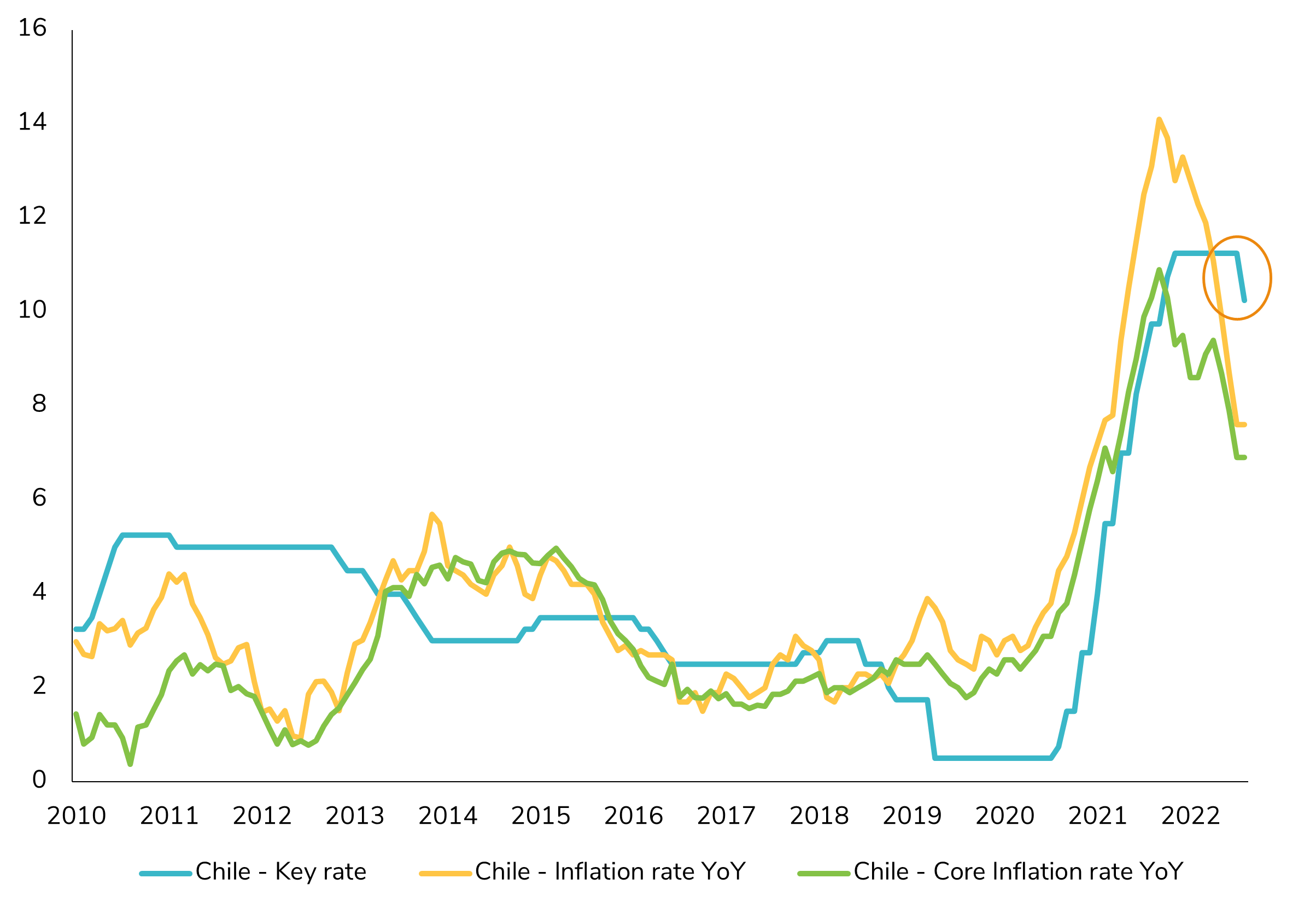

Chile Central bank cut its key rate by 100bps!

Here we go ! The Banco Central de Chile (BCCh) is the first central bank to kick off easing cycle! The Chilean Central Bank made a surprising move by cutting its key interest rate by 100bp to 10.25%, surpassing market expectations of a 50bp reduction. The decision was unanimous, and the BCCh hints at further rate cuts in the near future. This move comes as inflationary pressures ease rapidly, and economic activity weakens. Despite recent challenges, the CLP (Chilean Peso Spot) has shown resilience this year, benefiting from reduced political uncertainty. Policymakers aim to support the #economy amidst deteriorating #sentiment and economic activity. The minutes scheduled for August 14 will provide further insights into the central bank's outlook. Source : Bloomberg

US Treasuries sold off yesterday and are now on the verge of a breakdown from support

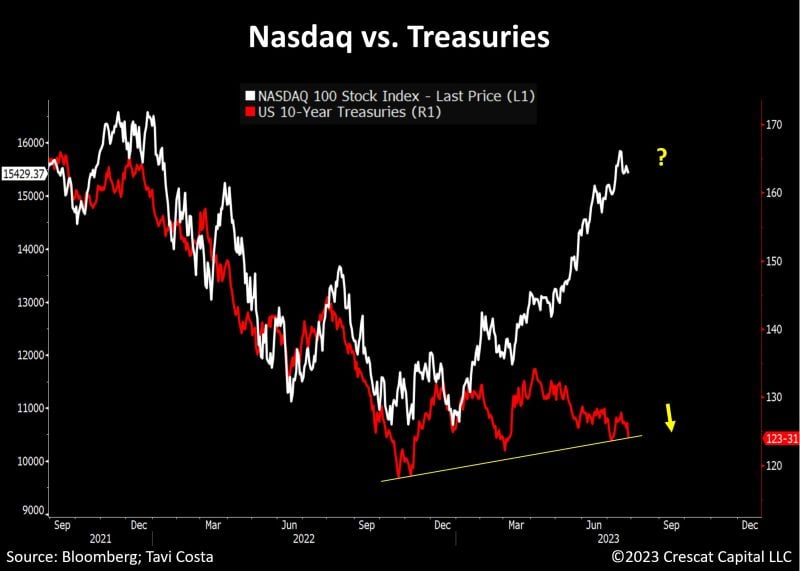

The chart below courtesy of Crescat Capital / Tavi Costa is a reminder of the divergence between rising yields and the highly valued Nasdaq index. Is this divergence sustainable? Source: Bloomberg, Tavi Costa

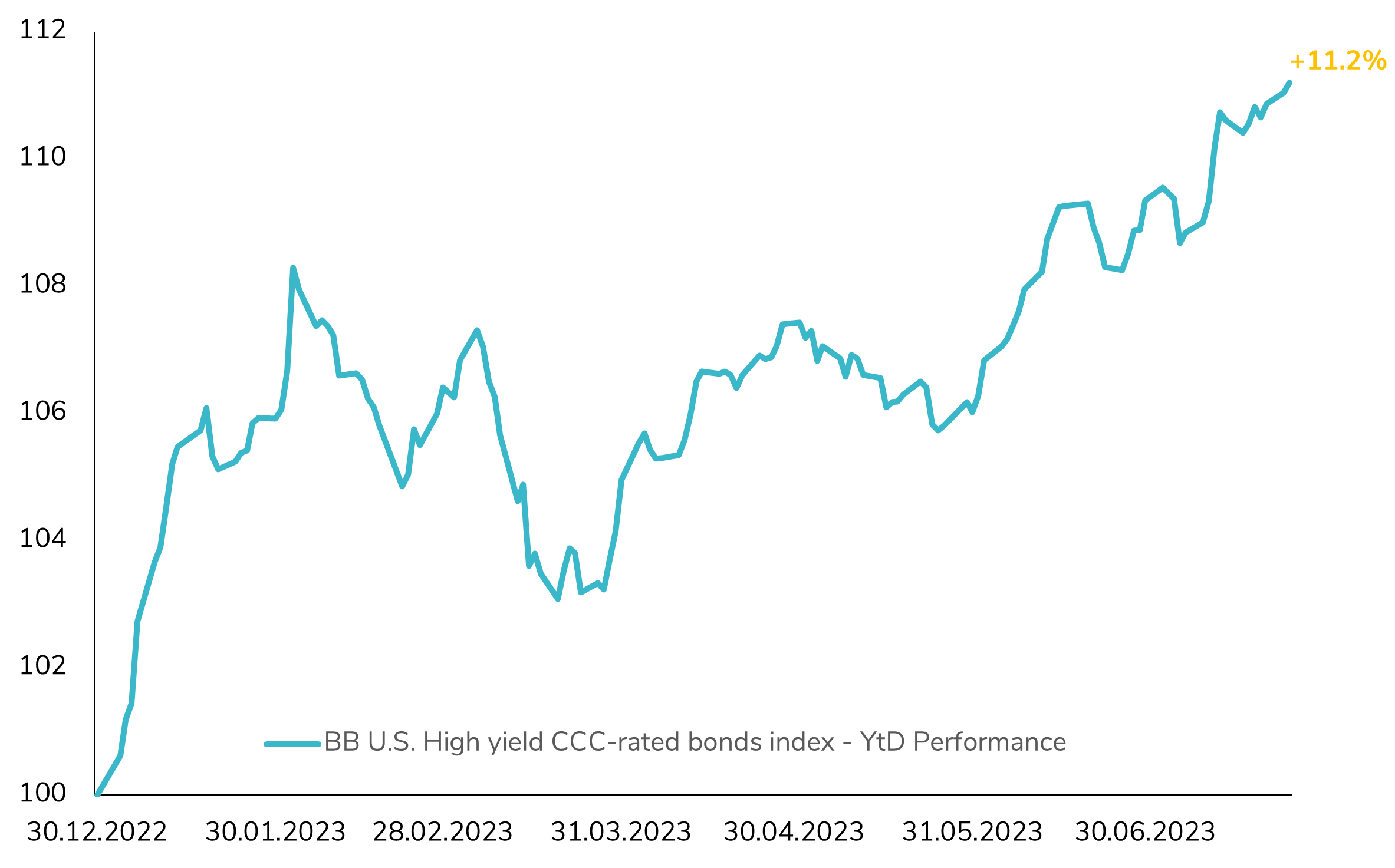

Remarkable Rally Continues in US High Yield CCC-Rated Bonds!

The Bloomberg US High Yield corporate CCC-rated bond index has delivered a staggering return of over 11% in 2023 so far. To put things into perspective, this level of performance has only been surpassed once in the last decade, back in 2016! The impressive rally in this segment can be attributed to the significant tightening of CCC credit spreads, which have contracted by a remarkable 200bps! Additionally, the high carry of the CCC-rated bonds, with an average yield-to-maturity of 13% in 2023, has contributed to the sector's stellar performance. However, as we approach a critical juncture in the economy, with looming concerns over a potential recession, the question arises: can this impressive performance sustain itself? While a soft landing scenario seems currently fully priced in, the possibility of a materialized recession in the coming months adds an element of uncertainty to the equation. Source : Bloomberg

93% of the US yield curve is currently inverted

Source: Tavi Costa, Crescat Capital, Bloomberg

Turkish Central Bank Implements another Significant Rate Hike!

The Turkish Central Bank (CBT) has taken another important step, raising its key rate by 2.5% to 17.5%. Though it slightly missed market expectations (18.5%), the chosen monetary policy path has instilled confidence among investors. This is evident as the 5-year Turkish Credit Default Swaps have hit a new low, not seen since November 2021. Furthermore, Turkish government and corporate bonds denominated in USD have demonstrated an impressive performance, gaining +6% in 2023. In addition to these developments, it is noteworthy that Turkey has recently received substantial economic support from the UAE, totaling more than $50 billion. Could this influx of support help mitigate the sharp weakness experienced by the Turkish Lira? Source : Bloomberg.