Hong Kong growth beat estimates by the most in 13 years in the first quarter.

Source: David Ingles, Bloomberg

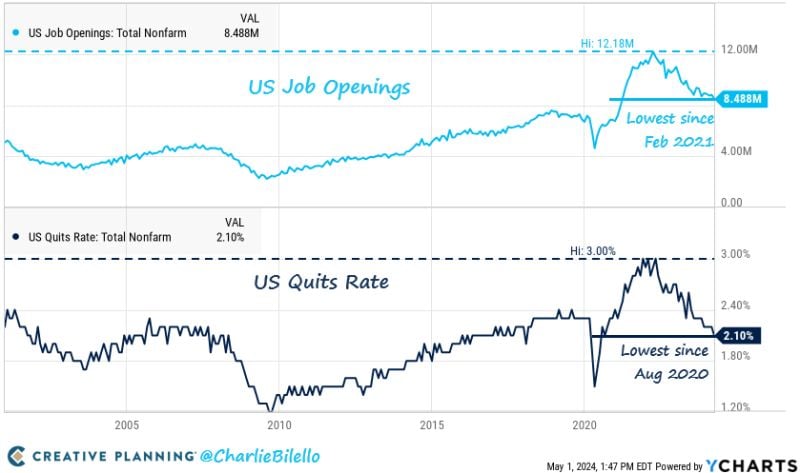

US job openings dropped in March to the lowest level in 3 years.

US available vacancies declined to 8.49 million from 8.81 million in February, hitting the lowest level since March 2021. Job openings have been declining for the past 2 years since the March 2022 peak of 12 million vacancies. Meanwhile, the quits rate has fallen to 2.1%, the lowest since August 2020. This suggests that many currently employed individuals are either losing confidence and/or are more dependent on their jobs. All eyes are on Friday's jobs report. Source: The Kobeissi Letter

The tightest labor market in US history continues to loosen with Job

Openings moving down to 8.49 million (lowest since Feb 2021) and the Quits Rate moving down to 2.1% (lowest since Aug 2020). Source: Charlie Bilello

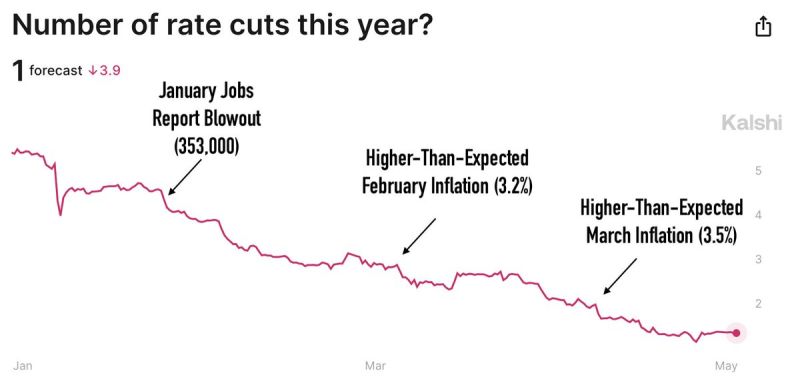

Interest rate futures have been wildly inaccurate over the last 12 months.

In September, just 2 rate cuts were expected by December 2024. In January, 6 rate cuts were expected by December 2024. Now, we will be lucky to get one rate cut over the next year or so. In fact, prediction markets are showing a 40% chance of ZERO rate cuts in 2024. Prediction markets also see an 11% chance of a rate HIKE in 2024 despite Powell saying he thinks it's unlikely. Source: The Kobeissi Letter, Kalshi

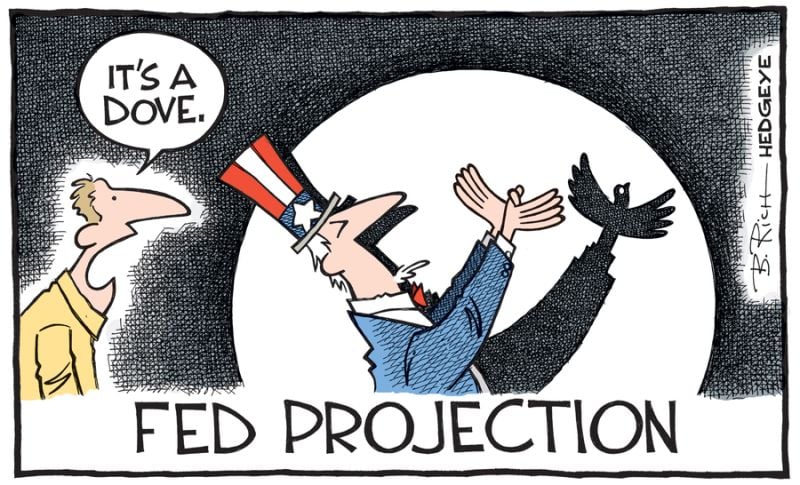

FOMC: No rate change, QT tapering in June is DOVISH (timing + amount)

Stocks, bonds, gold, bitcoin are all rallying. dollar dumped In a nutshell: 1. Fed leaves rates unchanged for 6th straight meeting *FED HOLDS BENCHMARK RATE IN 5.25%-5.5% TARGET RANGE 2. Rate cuts not appropriate until greater confidence inflation is heading to 2% 3. Fed adds following sentence to the statement: "In recent months, there has been a lack of further progress toward the Committee's 2 percent inflation objective." Inflation has eased "but remains elevated" 4. Fed to slow pace of balance sheet runoff starting in June. The Fed is tapering QT by MORE than the $30BN consensus estimate, instead will taper QT by $35BN, meaning monthly redemption cap on us treasuries goes down from $60BN to $25BN (starting June 1st). This means $105BN less gross issuance needed in Q3 (i.e The Fed implicitly saying 'yields are too high'). 5. Fed maintains mortgage-backed securities redemption cap at $35 bln per month, will reinvest excess MBS principal payments into treasuries. 6. Economic activity continues to expand at solid pace, job gains have remained strong, unemployment rate has remained low. 7. Risks to achieving employment and inflation goals 'have moved toward better balance over the past year,' as opposed to 'are moving into better balance' in the March policy statement. 8. Fed Chair Powell says it is "unlikely that the next policy move will be a rate HIKE." BOTTOM-LINE: There are some hawkish comments but overall Fed QT tapering in June is DOVISH (timing + amount) -> Stocks, bonds, gold, bitcoin are all rallying. dollar dumped Fed Chair Powell's press conference is dovish as well in terms of content and the tone of his remarks. As a reminder, we live at a time of fiscal dominance, i.e fiscal policy leads monetary policy.

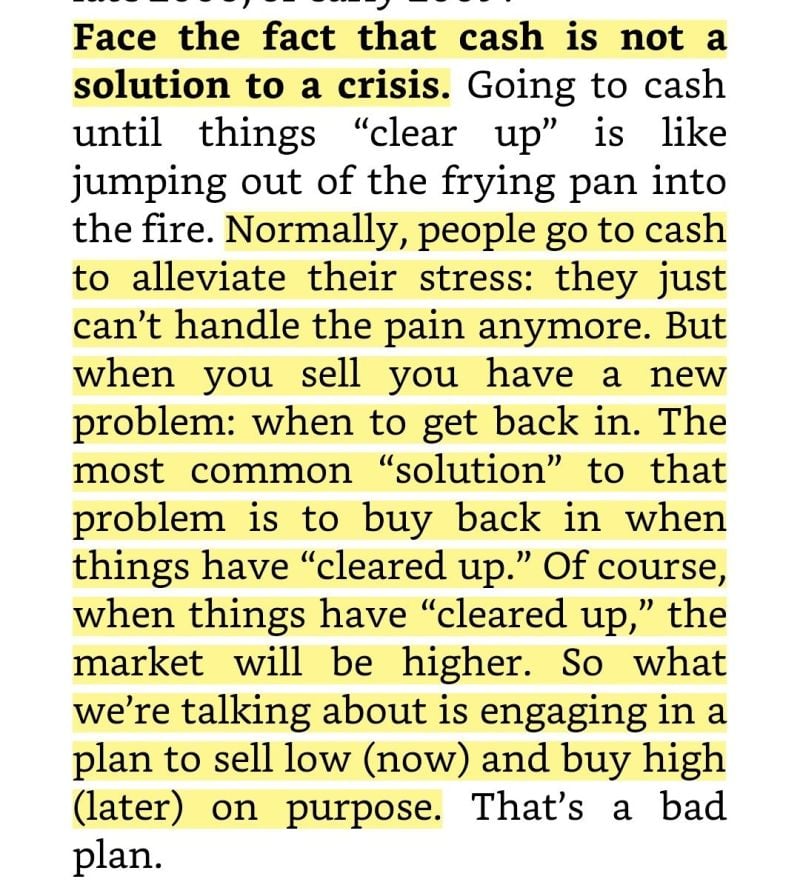

Face the fact that cash is NOT a solution to a crisis

Source: Investment Books (Dhaval)

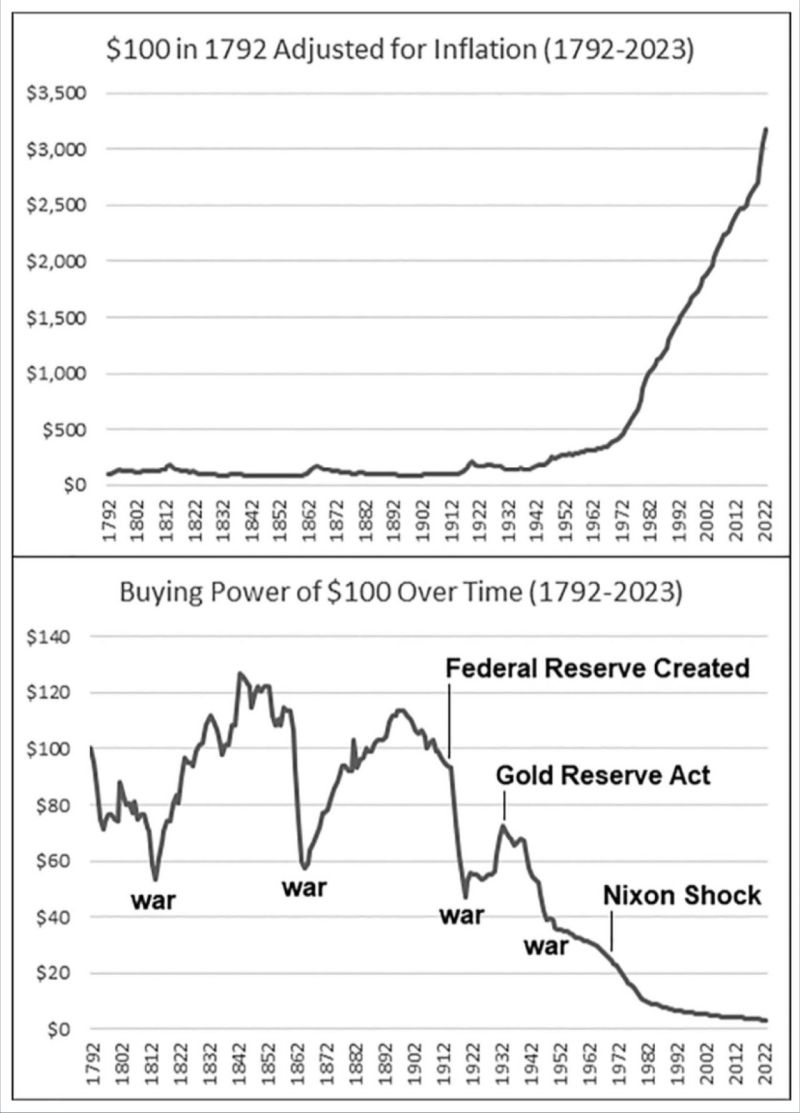

This is money debasement and loss of purchasing power looks like.

Below you can see the change in purchasing power of the U.S. dollar as measured by aggregate price inflation, including impactful historic events. Anyone who has attempted to save in dollars since the inception of the Federal Reserve until now has been robbed of their purchasing power. Source: Figure-7D, Broken Money thru Reese M.

What's going on here?

Source: Bloomberg, Lawrence McDonald