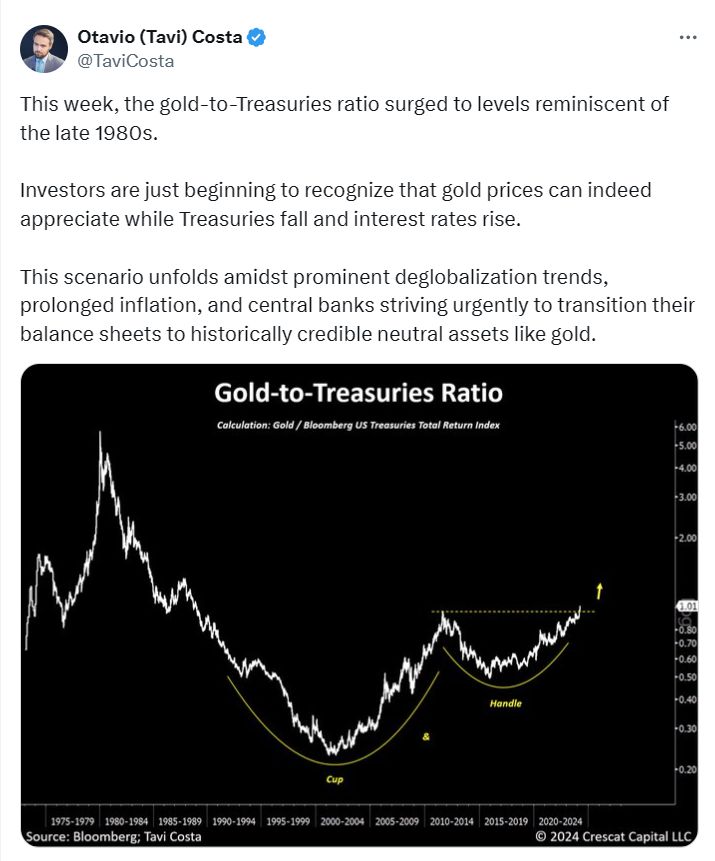

Gold as the ultimate macro hedge / diversifier within a multi-assets portfolio

This might be one of key investment theme of the current decade

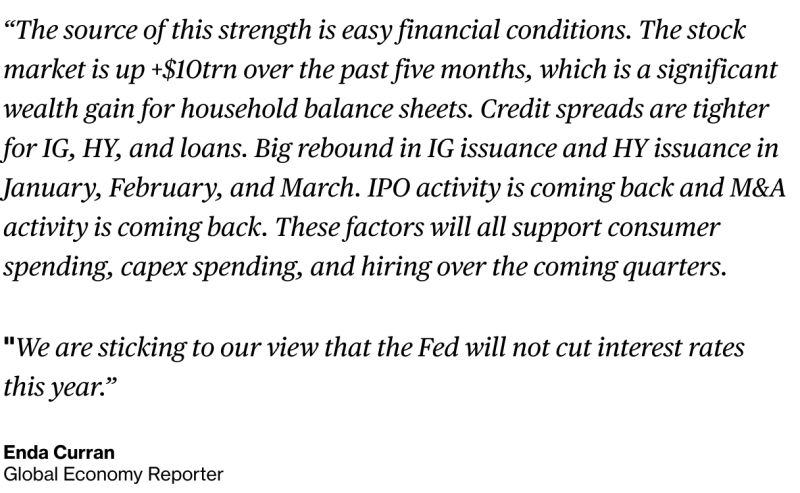

Torsten Slok at Apollo is sticking to his view that there will be no US rate cut this year...

Source: Markets & Mayhem, Apollo

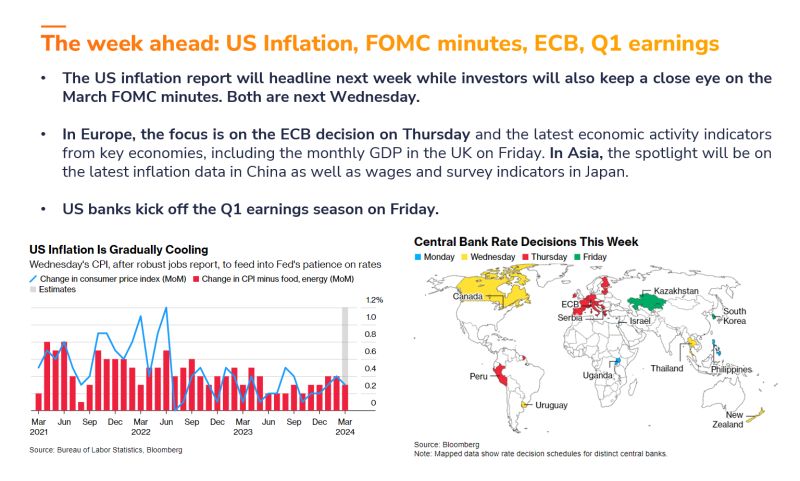

The week ahead...

Source: Syz Group

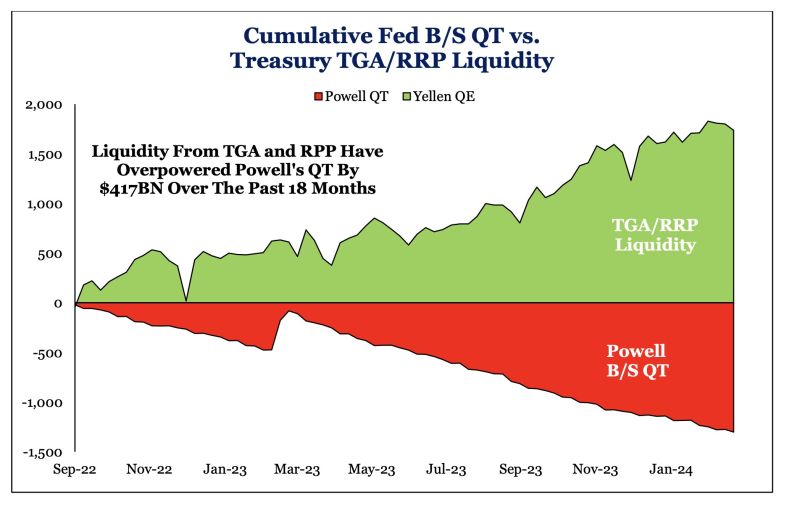

It's the liquidity, stupid! Yellen's stealth QE overpowering Powell's QT.

This probably helps risk assets performing well despite high interest rates and qt (Chart via SRP thru HolgerZ)

The global economy is addict to easy-money policies.

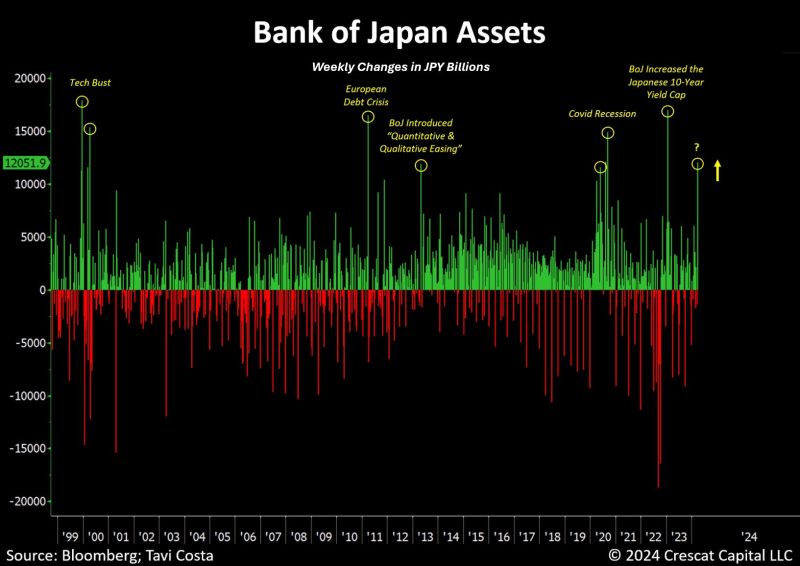

While everyone is talking about boj hiking rates, we just experienced one of the largest weekly changes in the BoJ balance sheet assets in history. In USD terms, this move accounted for nearly $80 billion in one week... Source: Tavi Costa, Bloomberg

Mind the gap:

Gold has hit fresh ATH despite a rise in US real yields. At current 2% 10y real rate, Gold at $2,300/oz is ~$270/oz expensive, Jefferies has calculated. There are fundamental reasons: Increased government spending & indications of a willingness to accept higher inflation Source: HolgerZ, Bloomberg

NOTHING NEW FROM POWELL YESTERDAY...

Fed Chairman Powell reiterated the Federal Reserve's cautious stance on interest-rate cuts, stating that they would wait and observe before making any decisions. While Powell didn't introduce any significant changes, his comment provided relief to Wall Street by suggesting that recent inflation data hadn't substantially altered the overall economic outlook. He also reiterated the likelihood of rate reductions at some point during the year. “On inflation, it is too soon to say whether the recent readings represent more than just a bump,” Mr. Powell stated. “We do not expect that it will be appropriate to lower our policy hashtag#rate until we have greater confidence that inflation is moving sustainably down toward 2 percent.” At the same time, he said that cuts to the benchmark federal funds rate are “likely to be appropriate at some point this year” as he does not believe “inflation is reversing higher.”

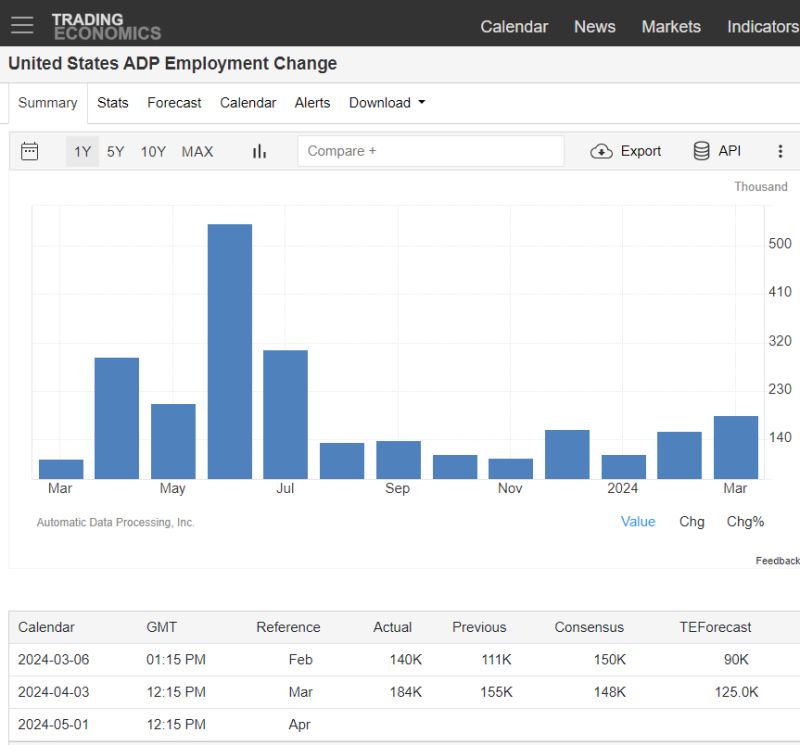

SUMMARY OF US MARCH ADP JOBS REPORT:

1. The U.S. economy added a higher-than-expected 184,000 jobs in March, as per ADP, easily beating forecasts for +148,000. 2. The number of monthly job gains was the highest in eight months (July 2023) 3. February number was also revised upwards. 4. Wage growth accelerated for those who changed jobs, rising +10% from a year earlier. Key Takeaway: The pickup in jobs growth supports the case that the labor market remains strong, and the economy continues to hold up better than expected. The ADP report does not point to imminent Fed rate cuts as markets continue to push back the timing of the first move. Source: Jesse Cohen, Trading Economics