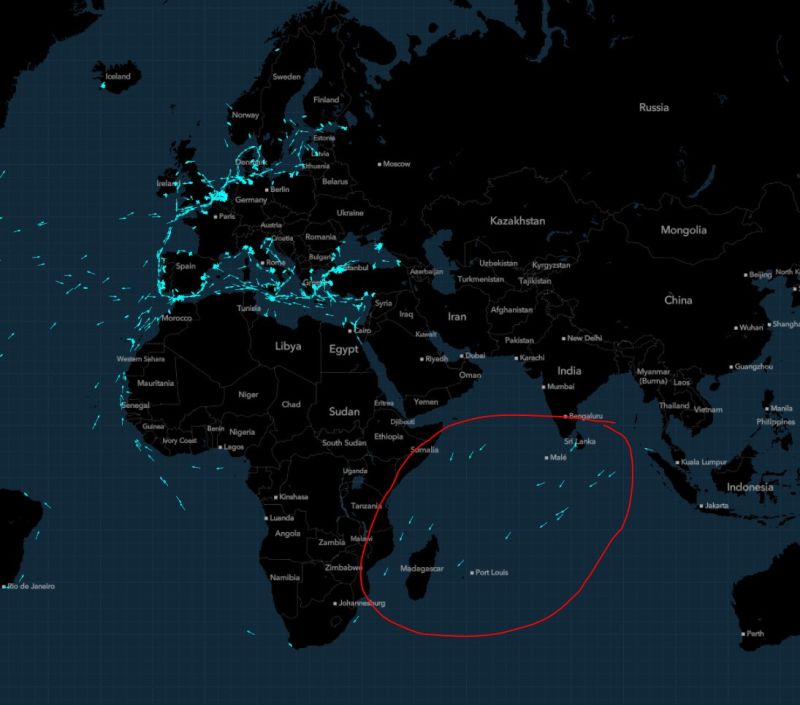

MAP OF THE DAY: The number of ships that have diverted from the Red Sea and instead taken the 10/14-day longer route around Africa has risen to >100.

The map shows **container ships** declaring European ports as destination, with one only left in the Red Sea | Red Sea Source: Javier Blas

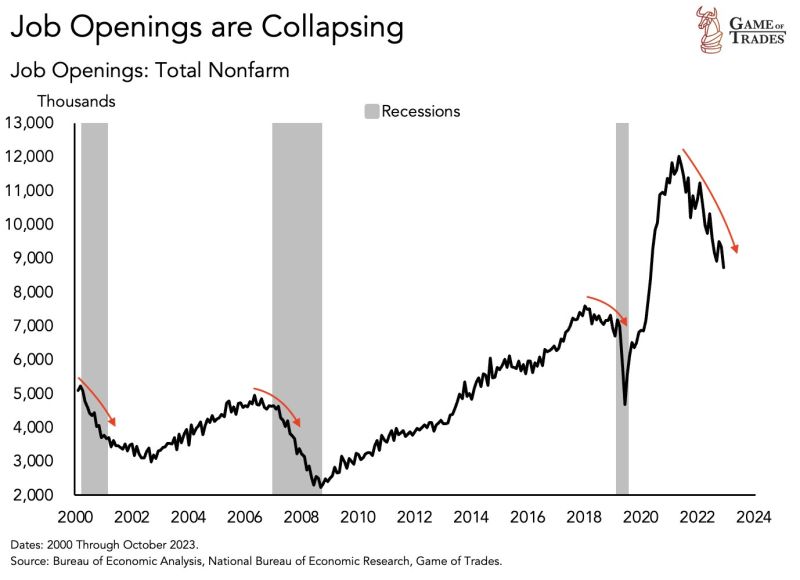

ALERT: Job openings are collapsing (but from a very high level)

Source: Game of Trades

Labor unions are pushing for big pay rise…

e.g Southwest Airlines pilot pay would increase 50pct under new labor contract. A wage-inflation spiral remains a threat (even if overall job creations are plunging) Source: CNBC

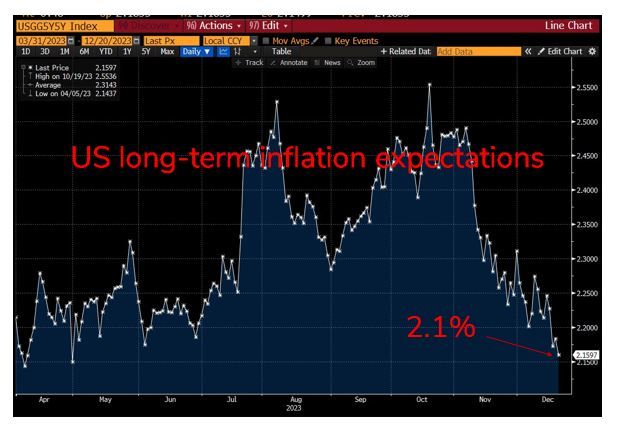

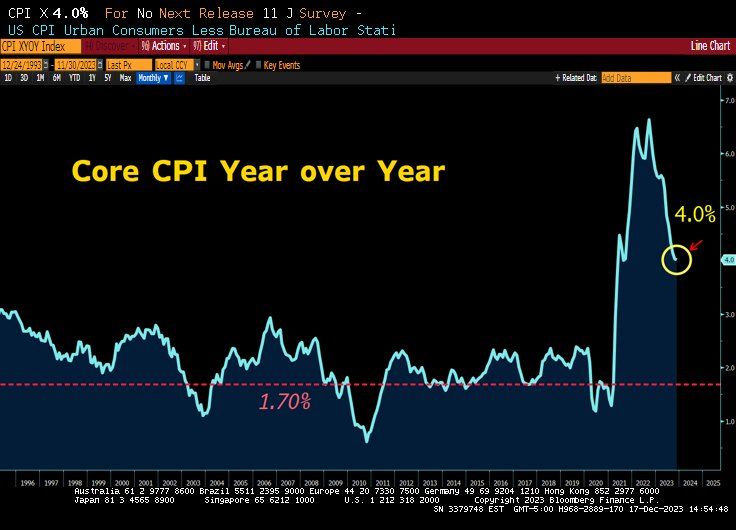

Longer-term US inflation expectations have fallen dramatically over the past two months, to close to the Fed's 2% target

Source: Bloomberg

Compound interest as the 8th wonder of the world...

.

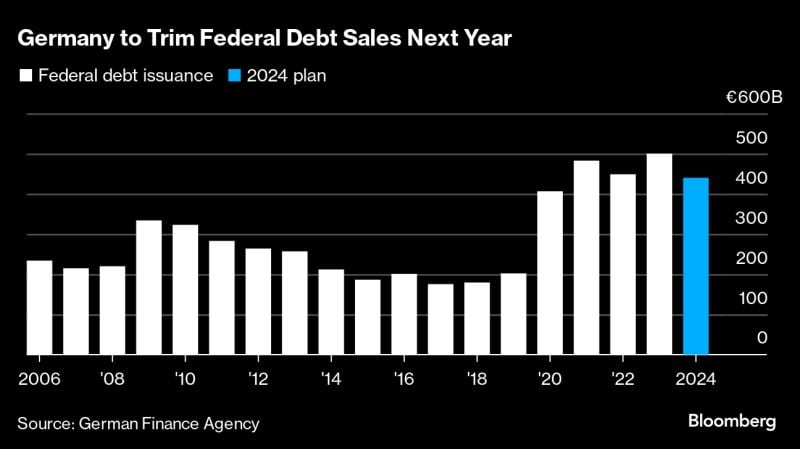

German federal government is set to trim federal debt sales next year following the German top court's 'debt brake' ruling. Berlin plans to issue ~€440bn in debt

That compares with a record volume of ~€500bn in 2023 Source: HolgerZ, Bloomberg

“The reports of my death are greatly exaggerated.” Mark Twain, 1897

Source: Lawrence McDonald, Bloomberg

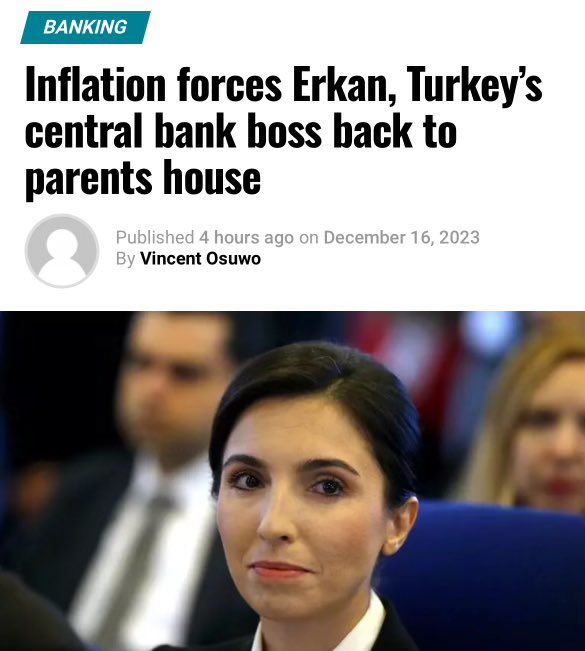

What a headline...

Hafize Gaye Erkan, the new head of Turkey’s central bank, said rampant inflation has priced her out of Istanbul’s property market, leaving the former finance executive with no choice but to move back in with her parents. “We haven’t found a home in Istanbul. It’s terribly expensive. We’ve moved in with my parents,” 44-year-old Hafize Gaye Erkan, who took up her post in June after two decades in the United States, told reporters. Source: Wall Street Silver