The Fed is finally giving up...

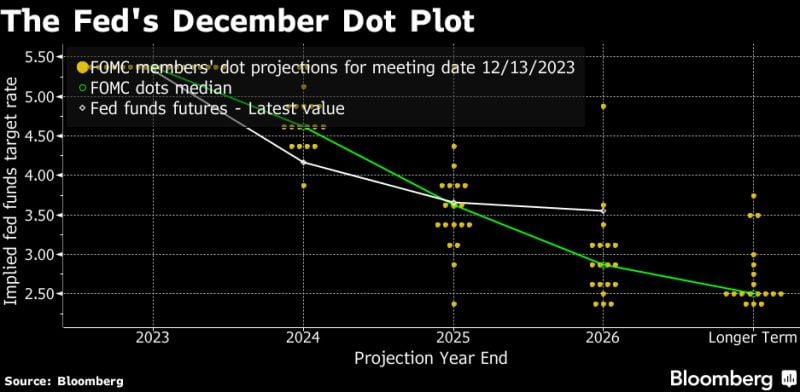

Fed holds rates steady but indicates three cuts coming in 2024. Indeed, the Dot Plot is adjusted down significantly more dovishly than expected, narrowing the gap to the market's expectation significantly... The US 10 year is down 20bp to 4%, the Dow surges by 300 points!

⚠️BREAKING:

*FED'S POWELL: IT IS NOT LIKELY WE WILL HIKE FURTHER *POWELL: POLICYMAKERS ARE THINKING AND TALKING ABOUT WHEN IT WILL BE APPROPRIATE TO CUT RATES Source: www.investing.com

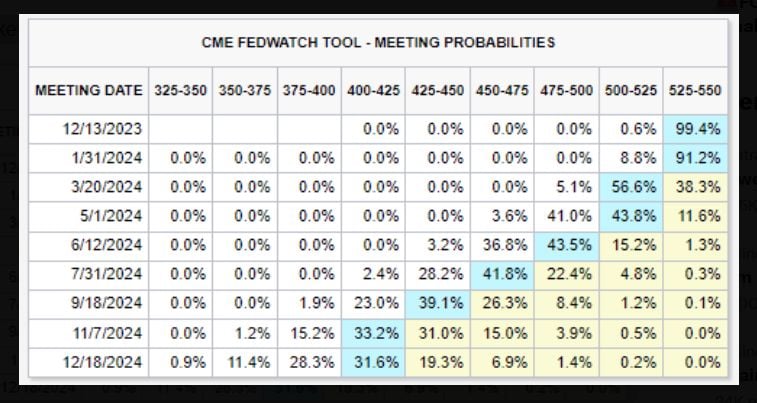

Interest rate futures shift to showing a ~57% chance of rate CUTS beginning in March 2024

Markets also see a growing 9% chance of rate cuts beginning as soon as next month. Futures are projecting a total of FIVE rate cuts in 2024. There's a 28% chance of 6 cuts and an 11% chance of 7 cuts in 2024. Meanwhile, the Fed just said they see just 3 rate cuts in 2024. So markets are still "fighting" the Fed. But the Fed is starting to adjust... Source: The Kobeissi Letter

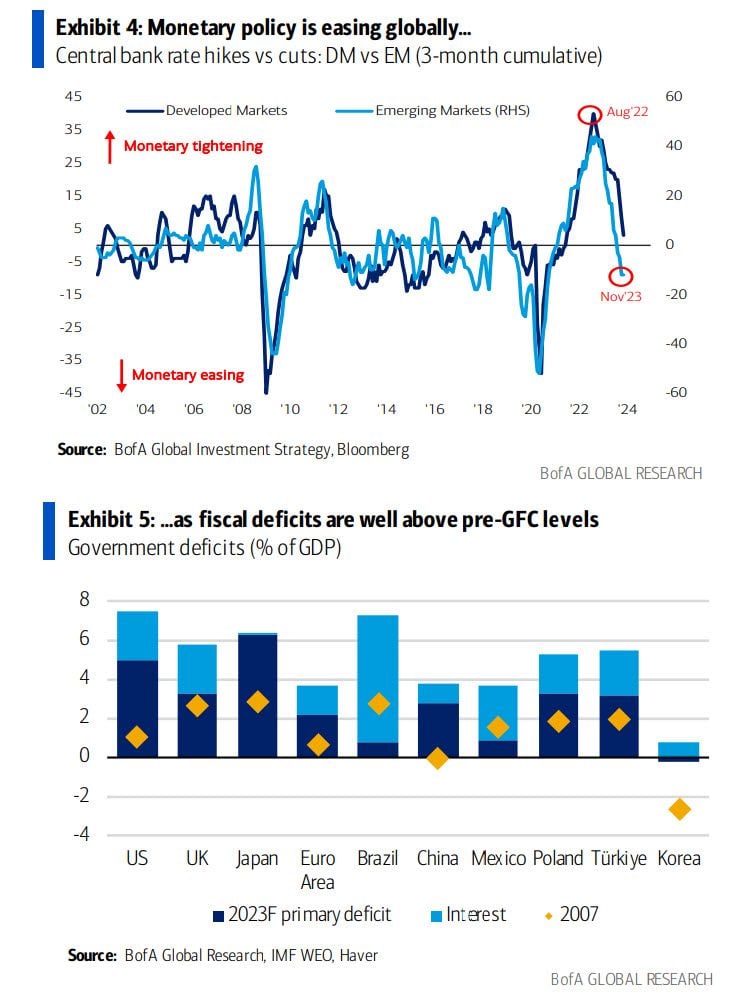

Monetary policy is now easing globally - and will ease much more in 2024/25 - at a time when fiscal deficits are far above the global financial crisis levels

Source: BofA

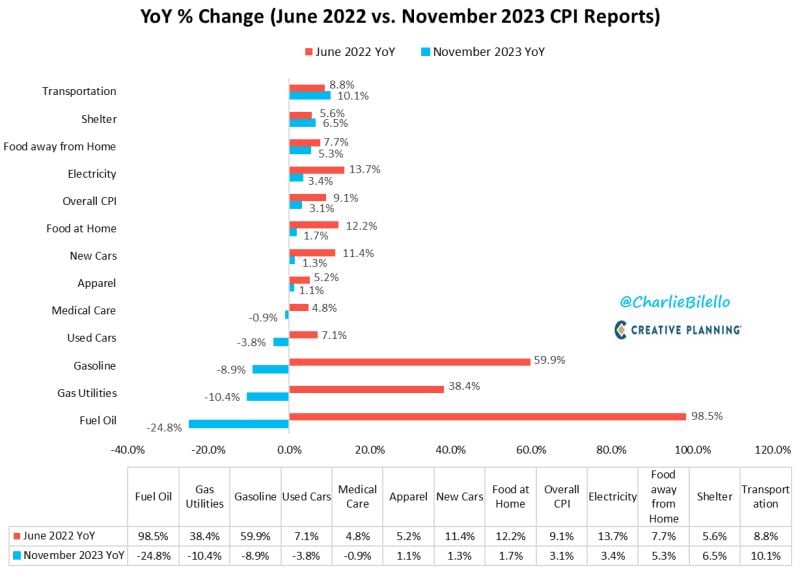

US CPI has moved down from a peak of 9.1% in June 2022 to 3.1% today

What's driving that decline? Lower rates of inflation in Fuel Oil, Gas Utilities, Gasoline, Used Cars, Medical Care, Apparel, New Cars, Food at Home, Electricity, and Food away from Home. Shelter and Transportation are the only major components that have a higher inflation rate today than June 2022. Source: Charlie Bilello

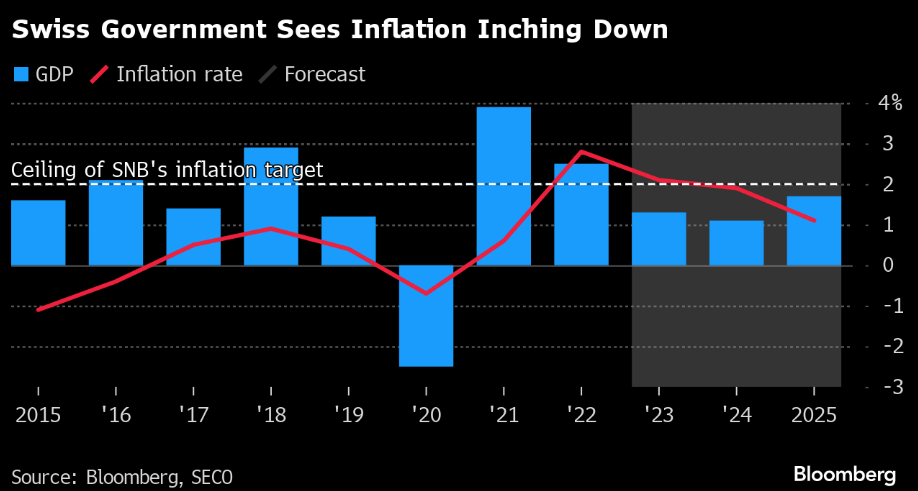

Switzerland’s inflation forecast backs SNB rate staying on hold

Switzerland’s government sees next year’s

inflation within the central bank’s target range, the latest evidence supporting a likely hold from policymakers this week. Consumer prices will grow at an annual 1.9% in 2024, in line with the previous forecast, the State Secretariat for Economic Affairs said on Wednesday.

Source: Bloomberg

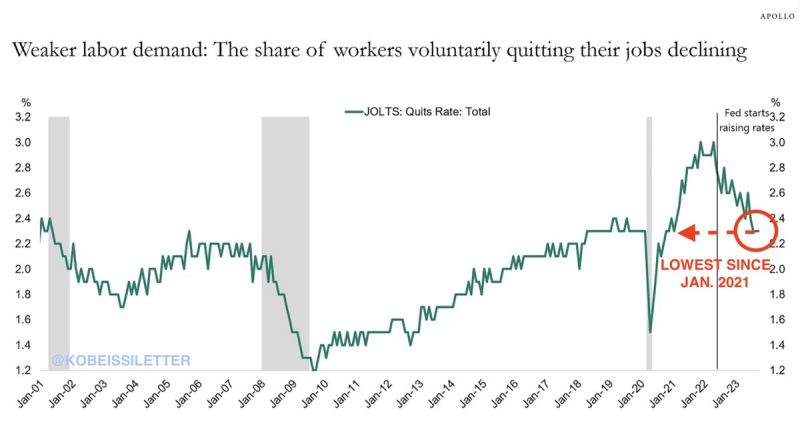

The share of workers voluntarily quitting their jobs is down to 2.3%

This is the lowest since January 2023 and down from 3.1% prior to the Fed started rate hikes. Weaker labor demand will be the theme of 2024 as job growth slows and rates stay higher for longer. Furthermore, as excess savings have now been depleted, consumers are more reliant on holding a job. Source: The Kobeissi Letter

A slightly disappointing US CPI inflation numbers for the markets...

US YoY CPI eased to 3.1% in November from 3.2% while the important core reading was unchanged at 4% YoY, despite seeing the MoM tick a bit higher. The so-called super-core, a measure watched by the Fed, meanwhile rose at one of the fastest monthly paces this year.