U.S. ECONOMIC DATA THIS WEEK:

*CPI INFLATION (TUES.) *PPI INFLATION, FED POLICY DECISION (WED.) *RETAIL SALES, JOBLESS CLAIMS (THURS.) *NY FED MANUFACTURING INDEX, INDUSTRIAL PRODUCTION, SERVICES PMI & MANUFACTURING PMI (FRI.) Source: www.investing.com

The average credit card interest rate right now has risen to 27.81%

And that's with U.S. credit card debt hitting new record highs north of $1,000,000,000,000 Source: Hedgeye

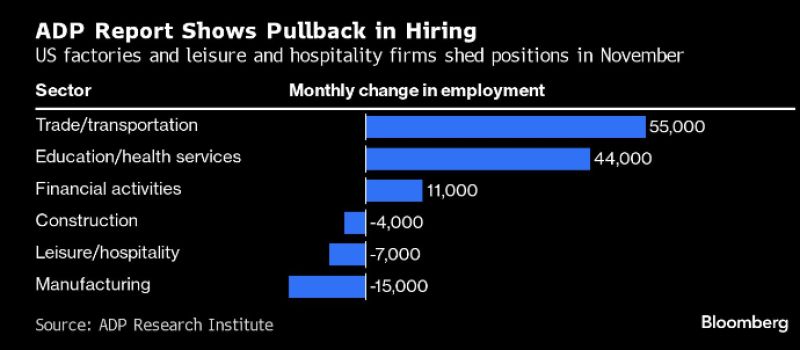

The ADP jobs report shows that the US labor market is cooling

U.S. firms scaled back hiring in November. Adding only 103k private payrolls compared 130k expected, according to ADP. Job cuts were seen in manufacturing, construction, and leisure/hospitality sectors. ADP’s report is based on payroll data covering +25 million US private-sector employees. Source: Genevieve Roch-Decter, CFA, Bloomberg

The US job market is starting to crater...

With consensus expecting only a modest drop from the reported September 9.553 million job openings, what the BLS reported moments ago instead was a stunning collapse of 617K job openings to just 8.733 million, the lowest since March 2021. This was a 6-sigma miss to the consensus estimate of 9.3 million... Source: www.zerohedge.com, Bloomberg

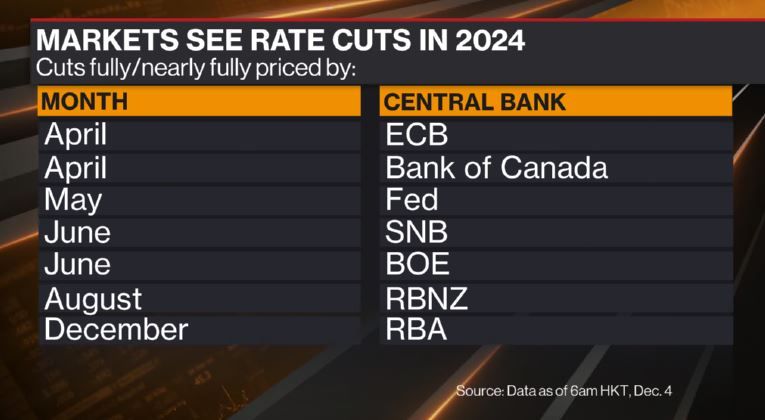

2024 is expected to be a year of interest rate cuts

Here's what's currently priced in markets of who does what when. Source: Bloomberg, David Ingles

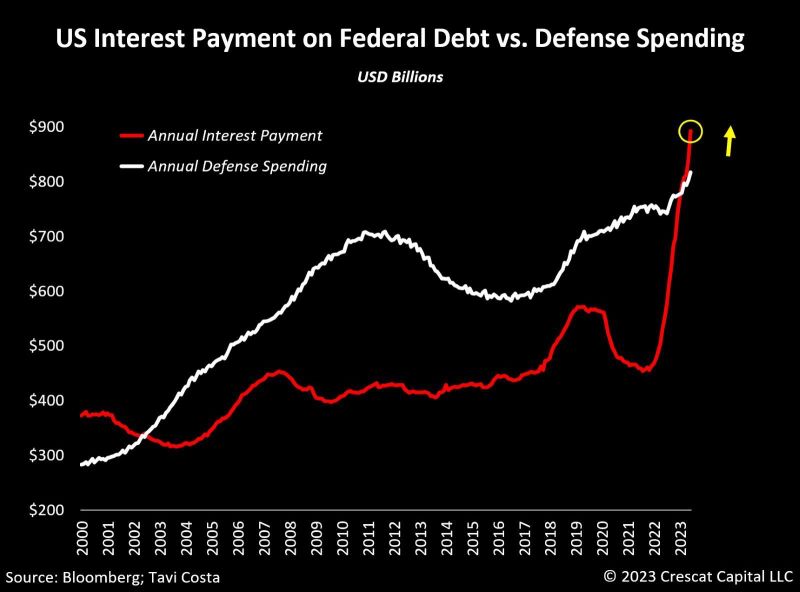

As highlighted in the Kobeissi Letter and in the chart below from Tavi Costa >>> Annualized interest expense on US Federal debt is nearing $1.1 TRILLION

To put this in perspective, 2023 defense spending was $821 billion. This means the US is on track to spend 34% MORE on interest expense than defense spending. In 2023, the US government produced $4.4 trillion in revenue. This means that 25% of receipts in the entire 2023 are equivalent to Uncle Sam's annual interest expense. Rising rates and falling tax revenue are both occurring at the same time. A tricky combination

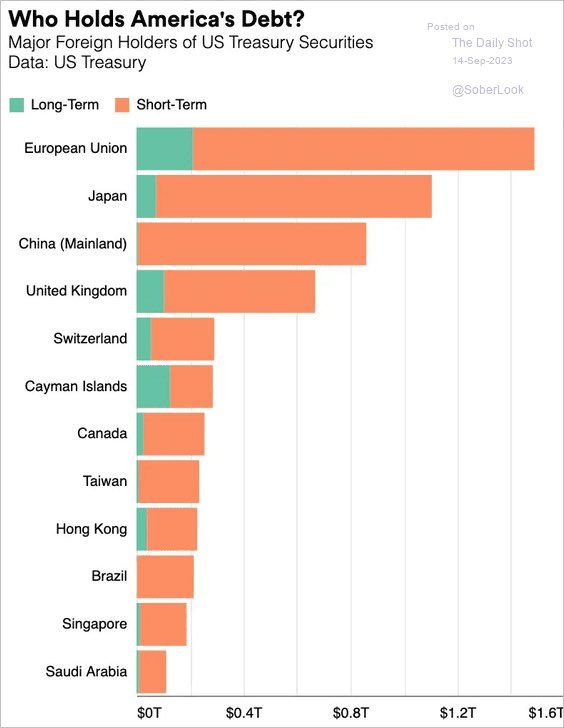

WHO HOLDS AMERICA' DEBT?

Source: WinSmart, The DailyShot

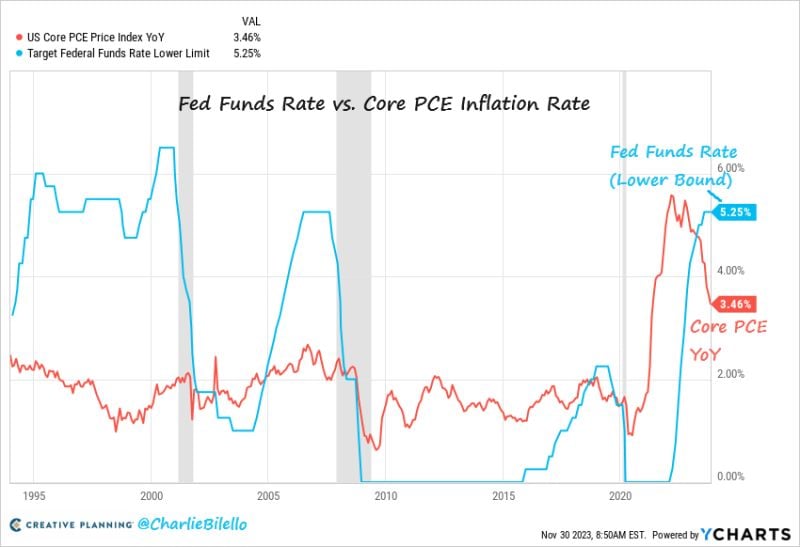

The Fed's preferred measure of inflation (Core PCE) moved down to 3.5% in October, the lowest since April 2021

The Fed Funds Rate is now 1.8% above Core PCE, the most restrictive monetary policy we've seen since 2007. Source: Charlie Bilello