This could be a problem for sugar prices which already hit 12-year highs back in May

Source: Barchart

Market-implied inflation expectations over the next 5-10 years have risen to the highest levels in more than a year

Traders are starting to game out a future with sustainably higher inflation and higher long-term bond yields. Source: Bloomberg, Lisa Abramowiz

The lagging effects of higher interest rates ?

Yellow Corp. filed for bankruptcy and will remain shuttered after the trucking firm’s long-running financial woes (rising bond & loan payments) were compounded by a dispute with its labor force (wage inflation). The firm closes after nearly 100 years and leaves 30k employees jobless (this will likely be reflected in a lower payroll print for August). Source: Bloomberg

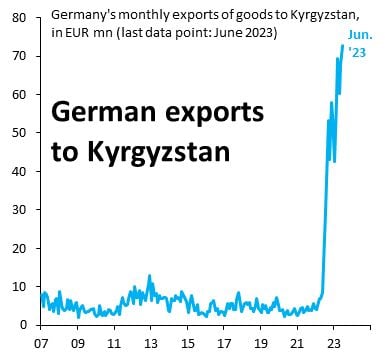

German exports to Kyrgyzstan are up 2000% in the past 3 years

Value of these exports is small, but this is just one of many examples showing how hard it is to police export controls on western goods to Russia. Source: Robin Brooks

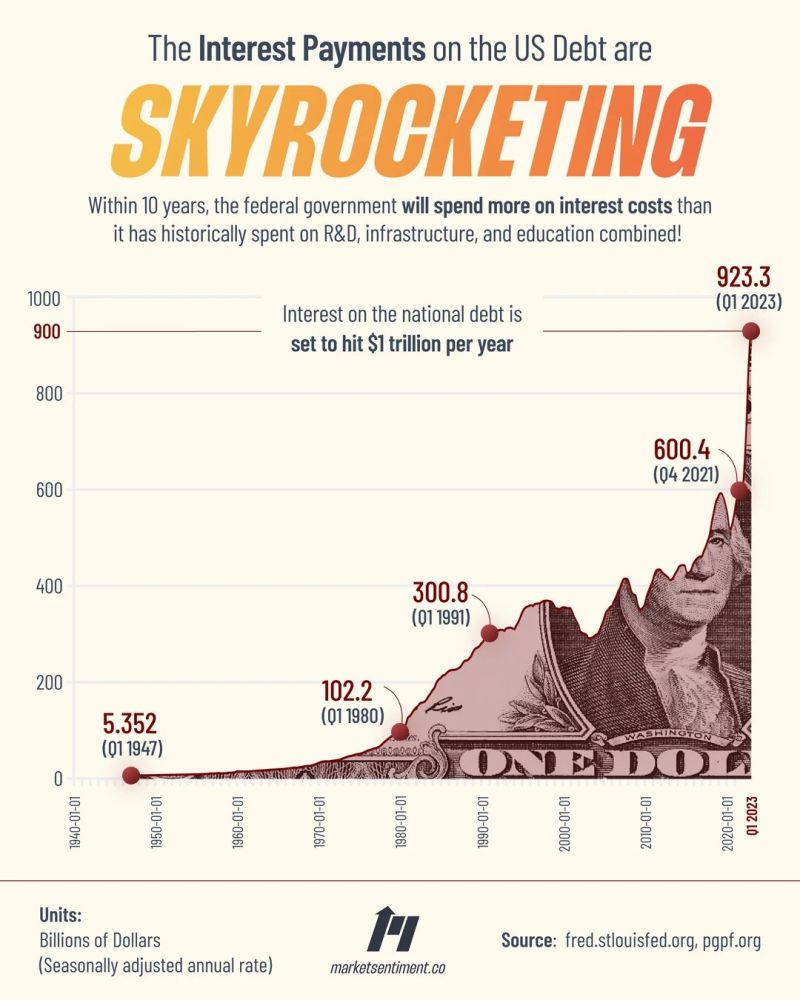

Interest payments on US government debt are soaring

source: Markets & Mayhem

Shorting US 10y bonds seems to be one of the most crowded trades at the moment

Among the shorts, Billionaire investor Bill Ackman. To his opinion, if long-term inflation is 3% not 2%, the 30y Treasury yield could rise to 5.5%. In contrast, Warren Buffett has announced buying positions in 10y US Treasuries. Source: Bloomberg, HolgerZ

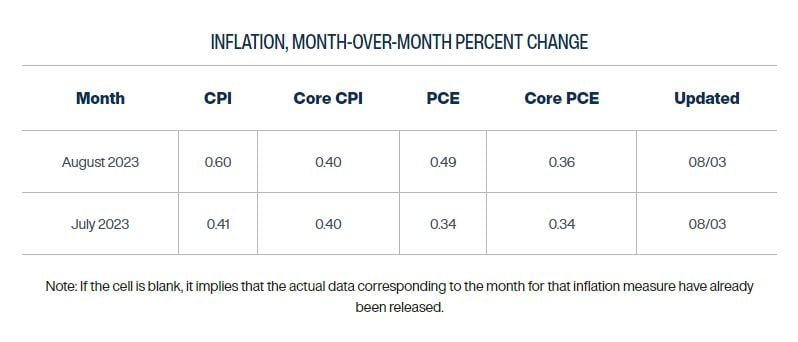

Consumer price inflation is creeping higher again on a month-over-month basis, driven in part by higher gas prices, according to the Cleveland Fed's forecast

Source: Lisa Abramowicz

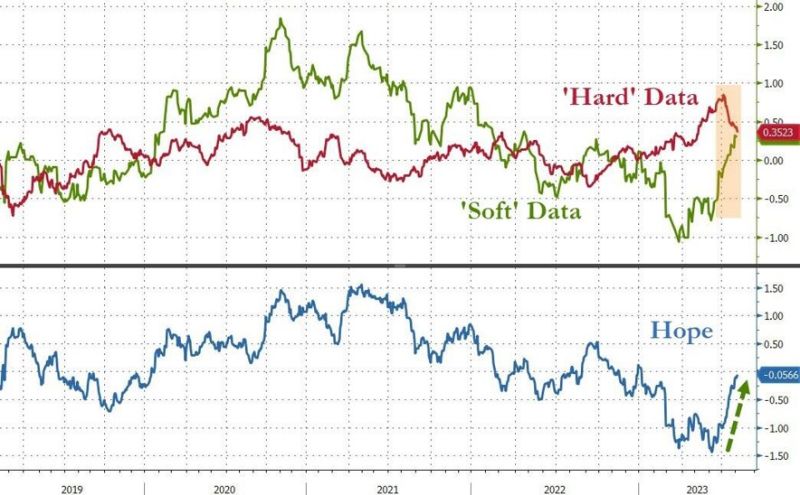

The Citi US Economic Surprise Index is at the highest levels since early 2021

That being said, there has been some divergence recently between "hard" and "soft" data. Indeed, 'Hope' has been in charge of macro data recently with 'soft' survey data surging back in its mean-reverting manner as 'hard' real data has been fading (led down by industrial, personal finance, and housing data)... Source: Bloomberg, www.zerohedge.com