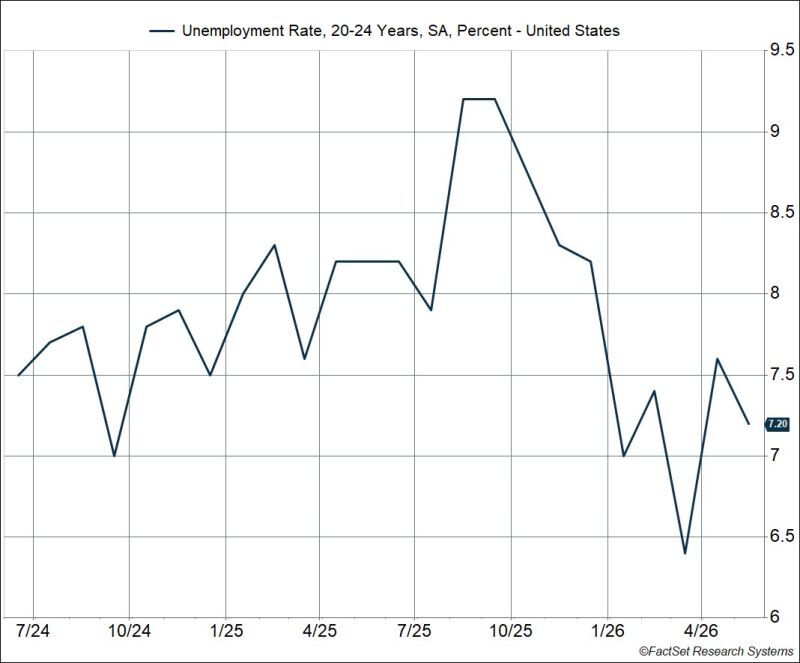

No, AI isn't taking young people's jobs.

Age 20-24 unemployment rate dropped again last month. Now to 7.2% from 9.2% last September. Source: Ryan Detrick, CMT

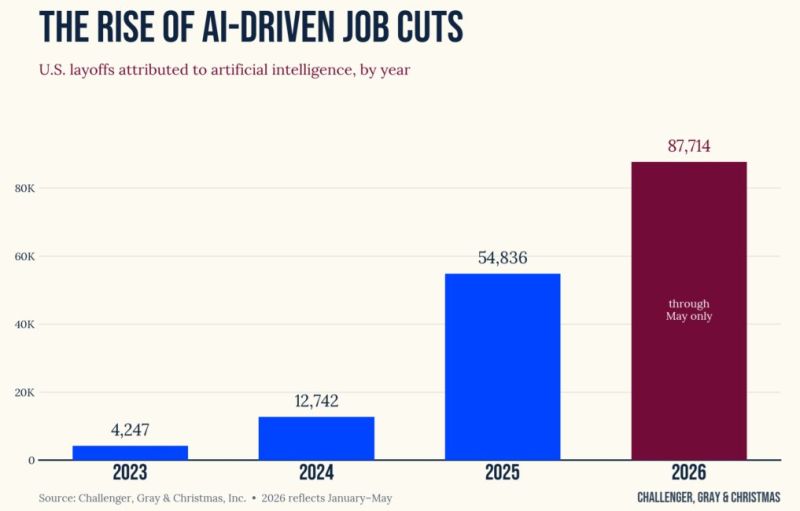

For the 3rd month in row, AI was the #1 reason for job cuts in the US.

88k job cuts were attributed to AI so far this year, a 60% increase over the AI-driven job cuts in all of 2025. Source: Charlie Bilello

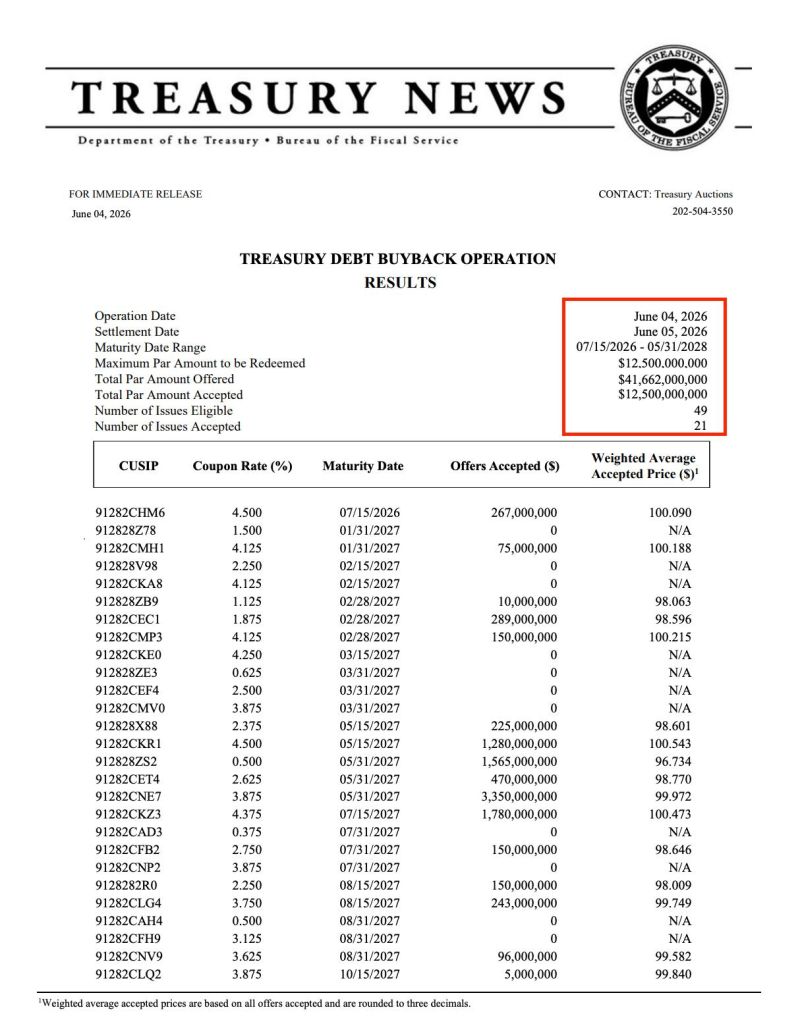

The US Treasury just bought back $12,500,000,000 of its own debt to improve liquidity.

Source: Bull Theory

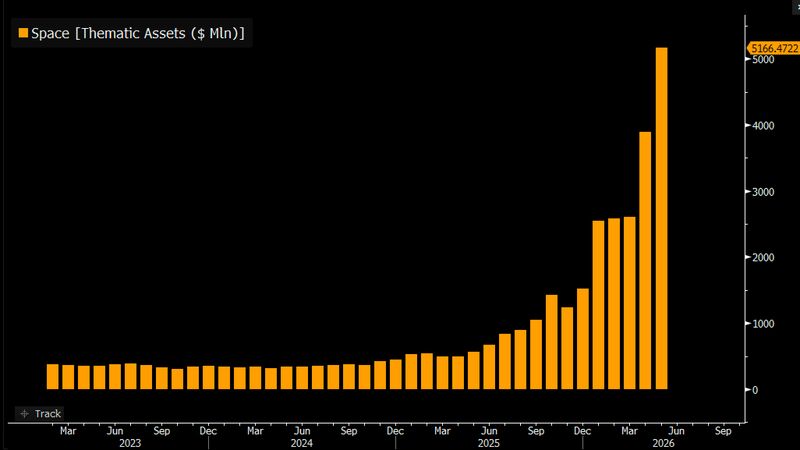

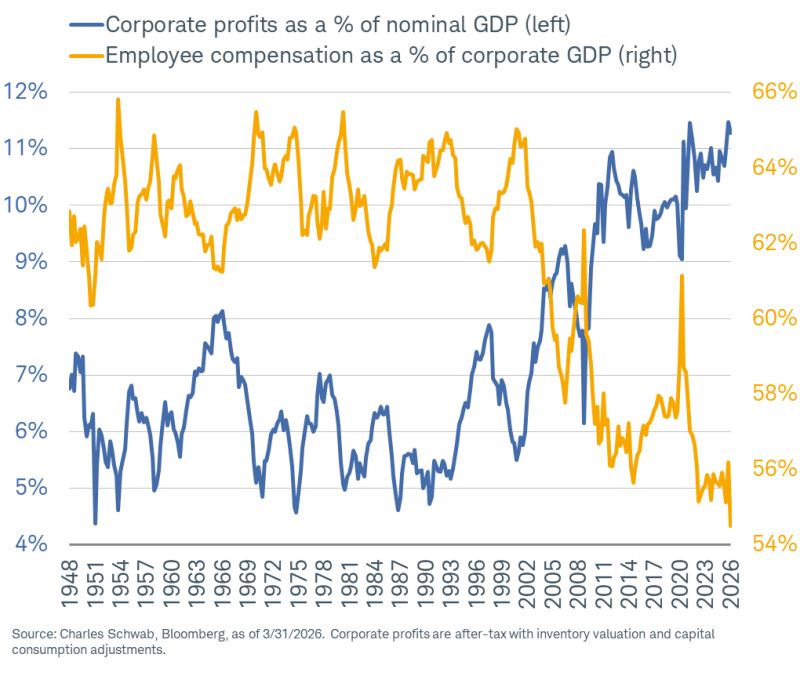

The K-shape economy

Corporate profits as a % of nominal GDP: right near an all-time high Employee compensation as a % of corporate GDP: all-time low Source: Kevin Gordon

In case you missed it... Better than expected ADP jobs data combined with Services PMI strength and soaring factory orders sent the US Macro Surprise Index ripping to its strongest since Sept 2023...

Source: zerohedge

ISM manufacturing PMI accelerates to 4-year high with improving production, new orders, and employment.

Prices remain 2nd highest since 2022. Source Bloomberg

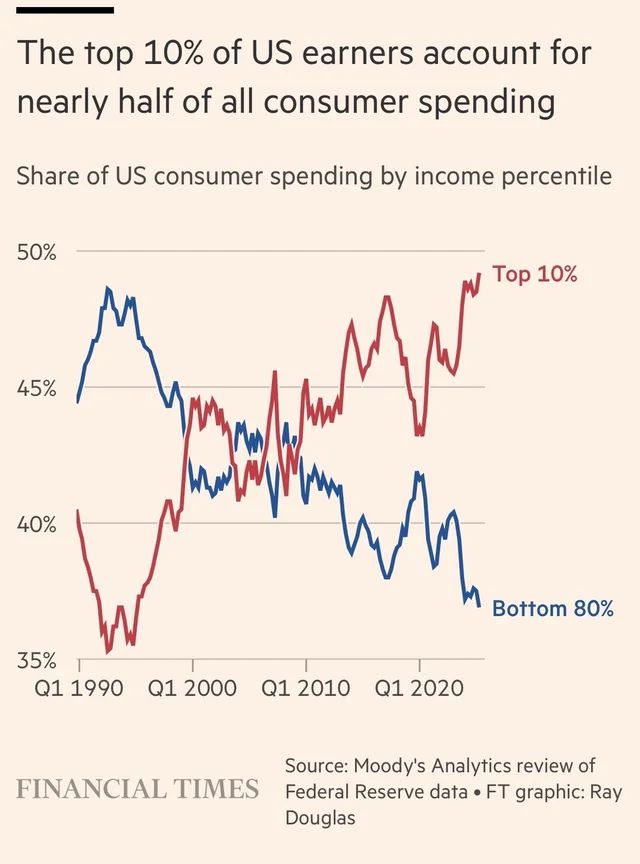

ONLY 10% OF AMERICANS ARE NOW KEEPING THE ENTIRE US ECONOMY FROM CRASHING.

28 million people are driving 49% of everything Americans spend. The other 221 million account for just 37%. This is the highest concentration of consumer spending ever recorded in US history. Every 1% rise in the stock market increases consumer spending by 0.05%. Markets are up double digits this year. The entire consumer economy is now a direct function of where the S&P 500 closes every day. The bottom 80% have nothing left to contribute. National household debt just crossed $18 trillion. Credit card balances hit a record $1.2 trillion as lower income households borrow just to cover basic expenses against prices that are 25% higher than 2020. Deloitte projects that a 10% stock market correction would cause real consumer spending growth to fall to just 0.2% in 2027 and drop 1% in 2028. The 28 million people keeping this economy running are fully invested in the stock market. The US economy has never been this dependent on this few people. And those people have never been this dependent on the stock market. Source: Bull Theory, FT

Bloomberg's US Macro Surprise data slumped yesterday with headline and core PCE printing below expectations on a MoM basis

Initial jobless claims a little weaker than expected, GDP disappointing, personal consumption weak (income unch), core capital goods orders declined, and a plunge in new home sales... Source: zerohedge