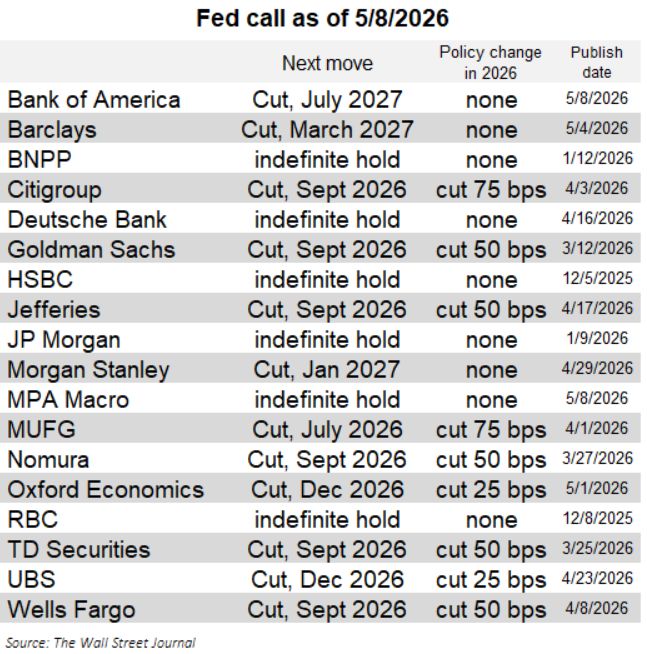

More sell-side firms and Fed watchers are removing/delaying cuts from their outlook, including a couple forecasters after the April NFP.

Half now see no cuts this year (and risks are clearly tilted to this group continuing to grow given inertial nature of these forecasts). Source: Nick Timiraos

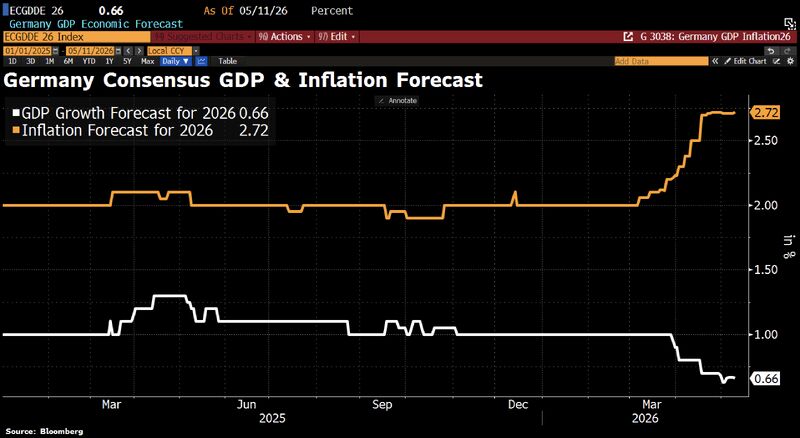

Germany appears to be heading towards stagflation.

Consensus GDP forecasts for 2026 have been revised down from more than 1% to just 0.66%, while inflation forecasts have climbed above 2.7%. Against this backdrop, the ECB is now expected to raise interest rates twice – at least, that is what markets are pricing in. Source: HolgerZ, Bloomberg

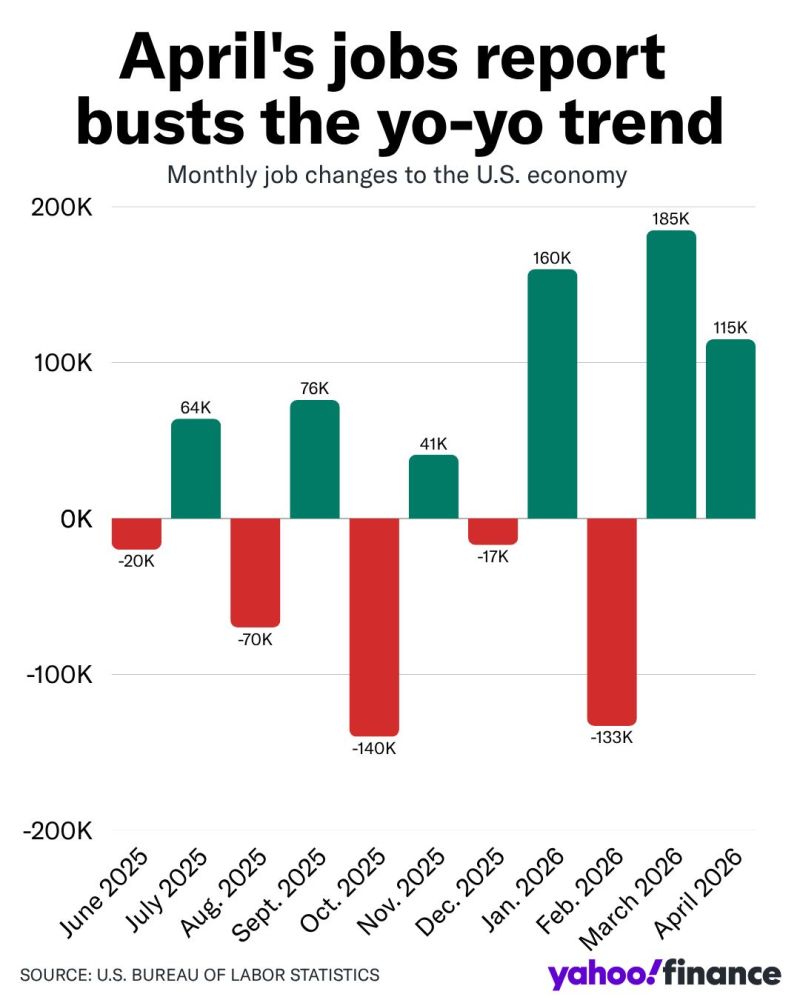

US job growth continued to strengthen in April, Goldilocks is back but read the fine print.

Today's US jobs report delivered exactly what risk assets wanted to see: a labor market strong enough to dispel recession fears, soft enough to keep the Fed in play. The headline numbers: ▪️ NFP: +115K — nearly double the consensus, despite Middle East war headwinds ▪️ Unemployment: 4.3% — steady, still well below the 4.5% line in the sand ▪️ Average hourly earnings: +0.2% MoM — below 0.3% consensus ▪️ Weekly hours worked: higher — demand-side resilience ▪️ Participation: 61.8% — softer than the 62.0% expected ▪️ Net revisions: -16K — March revised up, February down Why this matters for portfolios: The wage print is the story. Combined with this week's ULC and ECI data, the message is unambiguous: the labor market is less an inflation engine. That's a rather good news for the Fed (but don't expect them to cut in June) — and for duration, equities, and risk assets broadly. But here's the uncomfortable second-order read: What's "good news" for markets, muted wage growth, contained earnings — is the same data point feeding a deeper structural story: labor's declining share of GDP. Resilient demand. Constrained supply (retirements, fewer immigrants). And compensation that no longer keeps pace with productivity or capital returns. Markets celebrate. The Fed's job looks slightly easier. But the economic, social and political implications of this divergence are only beginning to surface. Source chart: Yahoo Finance

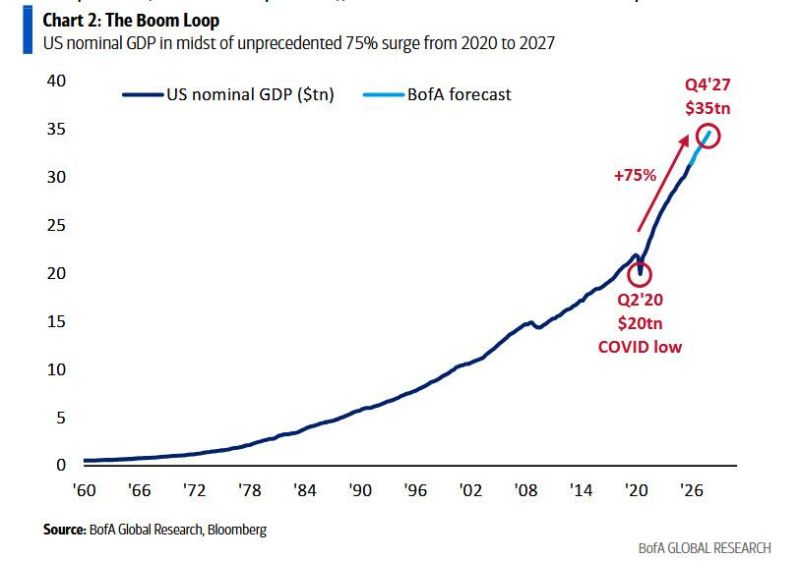

Investing at the time of high nominal growth...g all this money to build data centers with no revenue models. It's all going bust." (Clone)

BofA writes that nominal GDP is in the midst of a 75% boom in 7 years, from $20tn in ‘20 to $35tn in ‘27... In that kind of macro context, equities historically outperformed bonds. Period. Source: BofA, zerohedge

There is a manufacturing boom underway in America.

Source: Anthony Pompliano

The 189K initial jobless claims print yesterday was the lowest print since 1969 !

Meanwhile, Meta, Nike, Morgan Stanley, Amazon all cutting heads. But the number still prints like full employment !!! So what's going on? It seems the "low-hire low-fire" economy is turning as a "roach motel" for the unemployed: can't get in, can't get out. 💀 Source: Markets & Mayhem

On the other side of the world, China’s economic signals are shifting.

While trade dynamics fluctuate, attention is turning to its energy position. Estimates suggest China holds roughly 1.4 billion barrels in oil reserves—enough to cover about six months in a worst-case disruption scenario . At the same time, efforts by BRICS nations to move away from the U.S. dollar in oil trade have made limited progress, with the dollar still dominating global transactions. China has long relied on discounted oil imports from countries like Iran and Venezuela, but geopolitical pressures may complicate that strategy. Amid global tensions and proxy conflicts, the broader strategic rivalry between the U.S. and China remains a defining theme. Source: NY Times, Rothmus on X

US economic data keeps surprising to the upside, while European data keeps surprising to the downside.

That gap just keeps growing, according to Bloomberg economic surprise indexes. Source: Bloomberg, Lisa Abramowicz