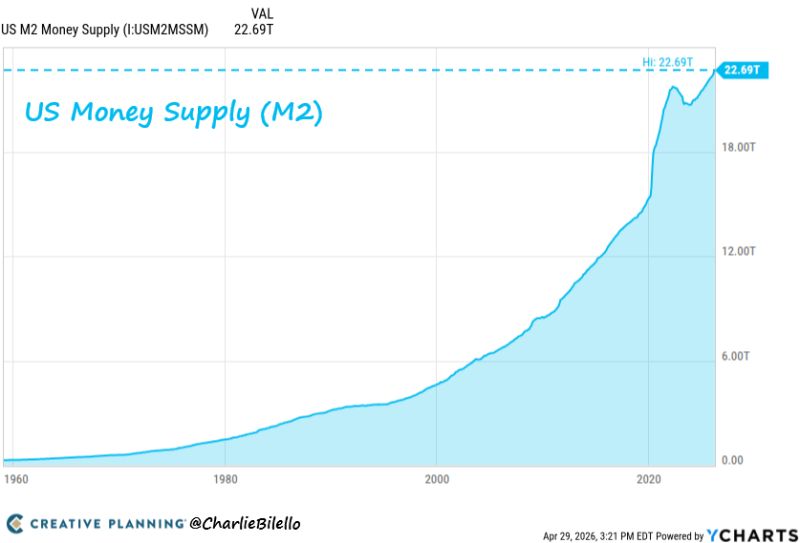

The Fed expanded the money supply by nearly $9 trillion under Powell.

Inflation has averaged >4% per year over the past 6 years. Powell's explanation? It was nearly all due to rolling “supply shocks" over which the Fed has no control. The truth: this inflation was made in Washington as it always is - from too much government borrowing/spending and too much government creation of money. Source: Charlie Bilello

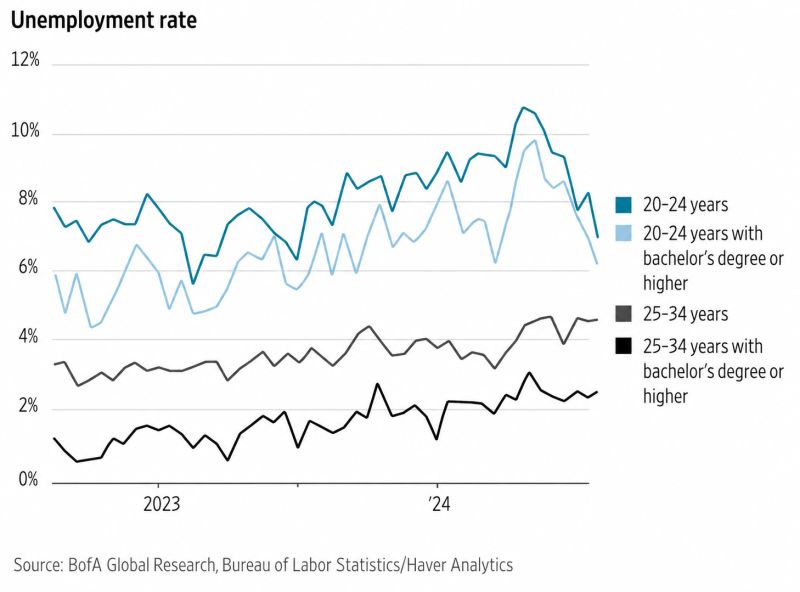

Young talents, don't believe all the negative headlines of AI killing jobs for graduates. Unemployment rate for 20-24 years in the US is actually plummeting...

Source: BofA

Market based inflation expectations are rising across the curve (1,2,5,10 year).

Source: Bloomberg, RBC

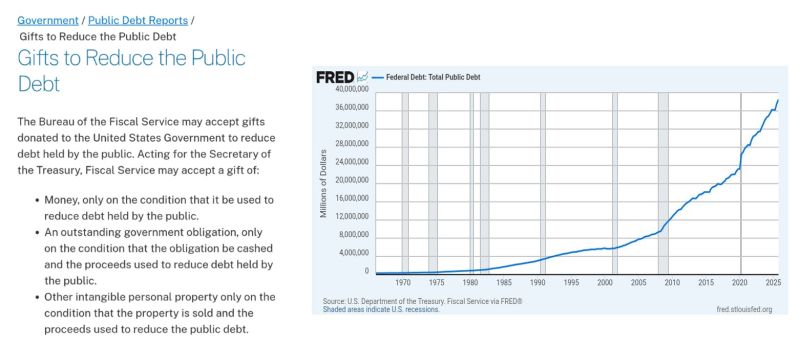

The US government is accepting donations to pay off its $39 trillion debt.

If someone donated $1 million every single day it would take 106,849 years to pay it off. Human civilization is only 5,000 years old. Source: Bull Theory, FRED

Japan's core inflation accelerated for the first time in five months, rising to 1.8% in March (versus +1.6% seen in February) as the Iran war fuels worries around energy prices.

The Core CPI number is matching forecasts and is staying below BOJ’s 2% target for a second month. Headline inflation came in at 1.5%, compared with 1.3% in February, staying below the central bank’s 2% target for a second straight month. The so-called “core-core” inflation rate, which strips out prices of both fresh food and energy, dipped to 2.4% from February’s 2.5%, marking its lowest level since October 2024. Rising oil prices have prompted government subsidies to cap gasoline costs, though these may be expensive to sustain. Analysts warn prolonged high energy prices could push core inflation toward 3%, while weakening household purchasing power. The Bank of Japan is expected to hold rates steady for now but maintain a bias toward future hikes as inflation expectations rise and economic risks persist. Source: CNBC

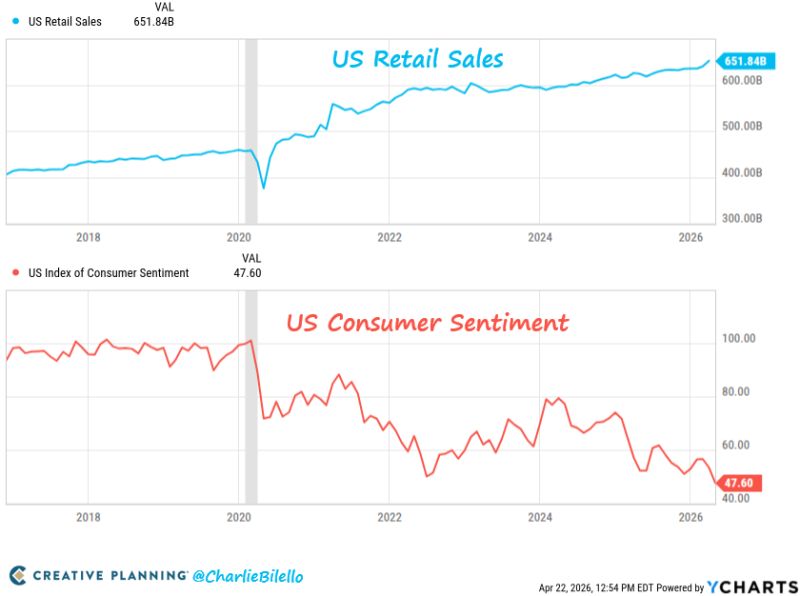

In case you missed it... US Retail Sales hit another all-time high while Consumer Sentiment is at its lowest level in history.

Watch what they do, not what they say. Note however that retail sales chart looks less fancy when you consider real data (instead of nominal) Source. Charlie Bilello

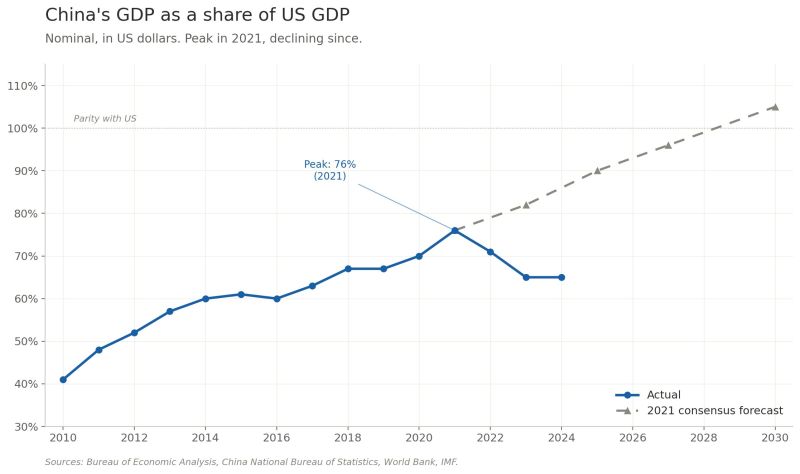

The United States has a long track record of outlasting its rivals. The Soviet Union collapsed.

Japan, once predicted in the 1980s to eclipse the American economy, is now significantly smaller. China now appears to be on a similar trajectory. In 2021, China’s GDP had risen to 76% of that of the United States, and many analysts believed it would surpass the U.S. before 2030. That expectation has since unraveled. By 2024, the U.S. economy stood at $29.2 trillion compared to China’s $18.9 trillion—a gap that has widened for three consecutive years. Meanwhile, China’s working-age population is declining, its fertility rate has dropped to around 1.0—well below replacement level—and there is little immigration to offset the demographic decline. Yet America benefits from believing it faces a formidable rival. The belief is what keeps it competing. Source: Martin Varsavsky

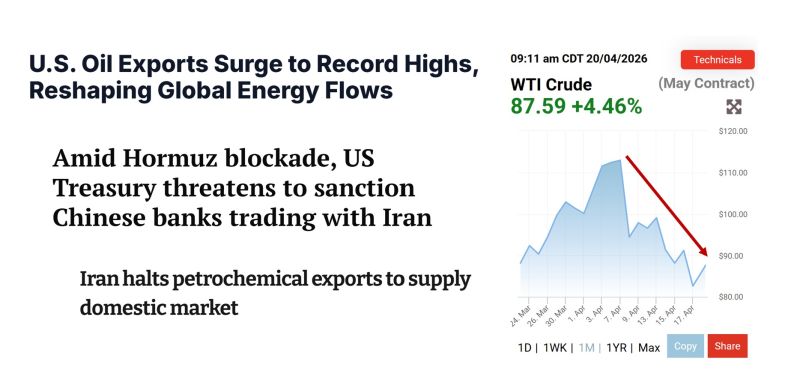

The US blockade of the blockade seems to work rather well for the US.

It's substantially reduced Iran's oil exports (and inflow of hard currency), seized an Iranian ship and threatened secondary sanctions on Chinese banks that deal in Iranian oil. Meanwhile, oil prices are down from their highs. And the US is exporting record volume of il & gas. Kudos! Source: Robin Brooks