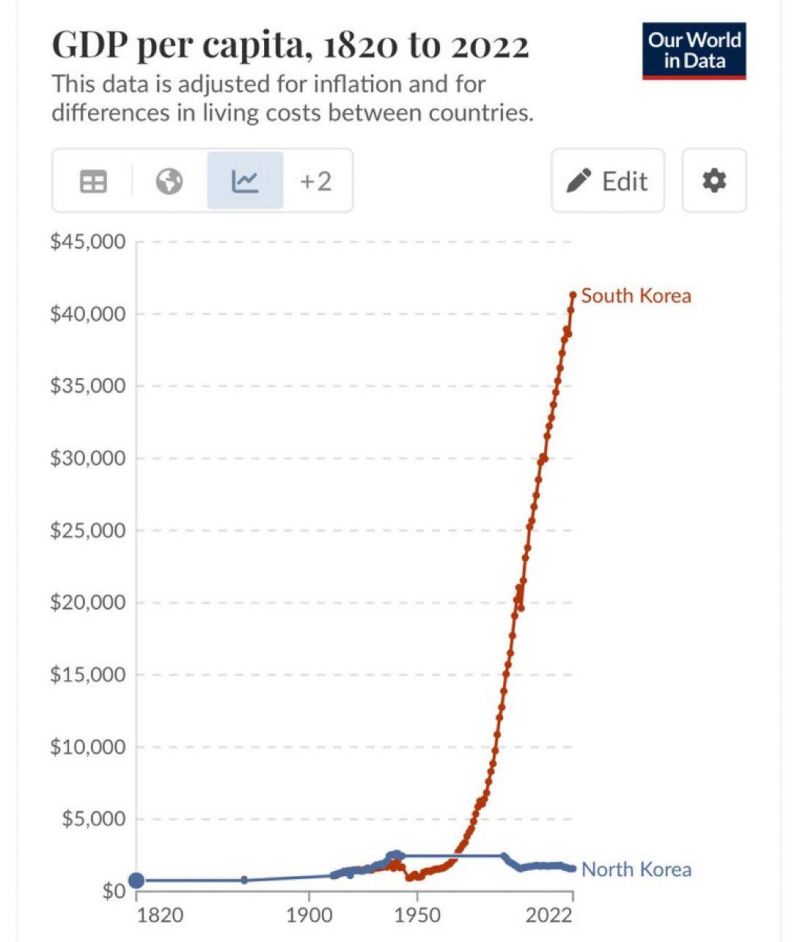

GDP per capita South Korea vs North Korea

Source: Jacob King

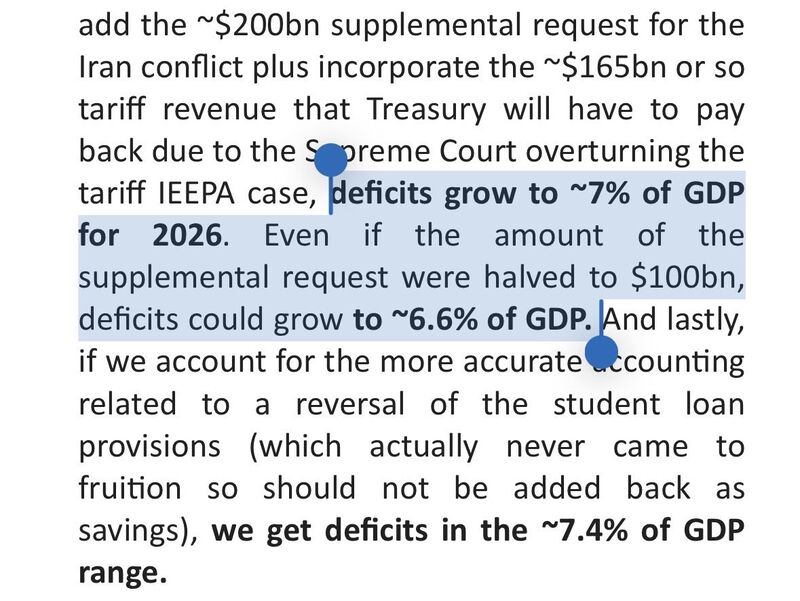

US budget deficits likely “grow to ~7% of GDP for 2026.

Even if the amount of the supplemental request were halved to $100bn, deficits could grow to ~6.6% ..” Source: Carl Quintanilla

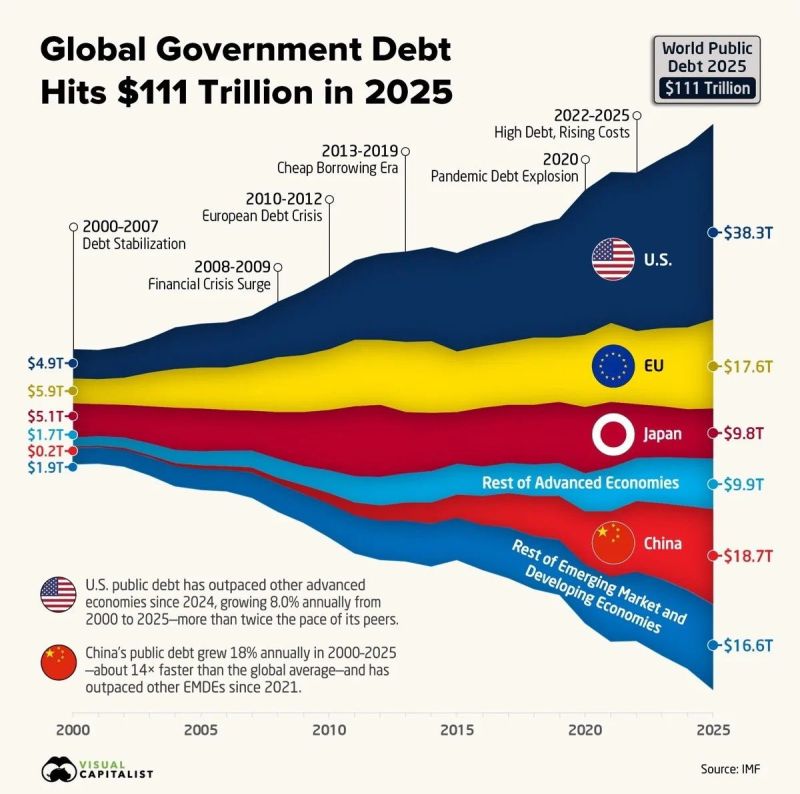

Global debt just crossed $111 trillion. Up from ~$20 trillion in 2000.

The U.S. (~$38T) and China (~$19T) now account for over half of it. For a decade, zero rates allowed this to build without pressure. That’s changed. New issuance now comes with a real cost. Interest expense is rising quickly, especially in the U.S. Source: Michael Chu, CFA, CFP Visual Capitalist

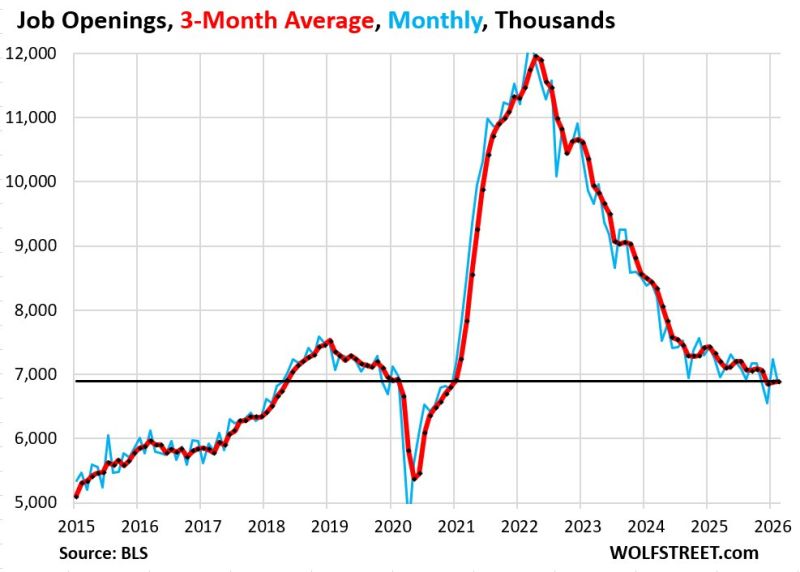

In case you missed it... The US job market continues to deteriorate

Job openings fell -358,000 in February to 6.88 million, giving back most of the January jump. The 3-month moving average continues to fall, now at ~6.89 million, now below the 2018-2019 pre-pandemic levels. There are now just 0.9 job openings for every unemployed worker, near the lowest of the current business cycle. By comparison, the ratio peaked at 2.0 in 2022, meaning available jobs per unemployed worker have been cut in half. Total separations have also dropped to a decade low, suggesting employers are neither hiring nor firing, effectively freezing the labor market in place. The job market is quietly weakening beneath the surface. Source: Global Markets Investor, wolfstreet

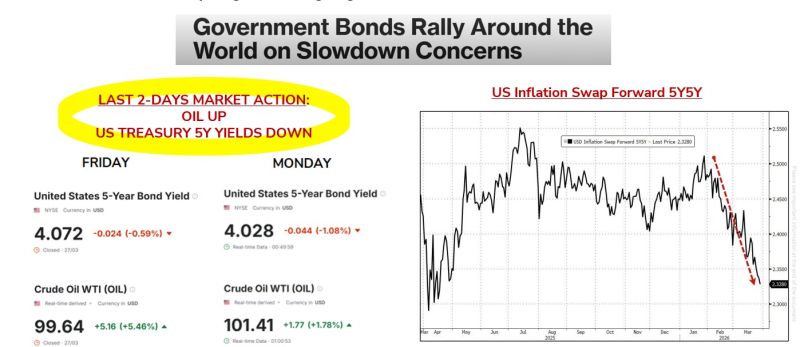

Fixed Income: Are markets starting to price in “growth fear” (instead of inflation fear”) ?

•A notable bid to bonds on Friday (decoupling from the correlation-one with oil and stocks) suggests inflation fears are ebbing, and attention is shifting to growth concerns. Monday market action gives the same message… •5Y5Y inflation swaps signal the ongoing decline in medium-term inflation... Source: Bloomberg, www.zerohedge.com

This is not Apple, Tesla or even Nvidia. It’s the U.S. National Debt.

Source: Not Jerome Powell

U.S. National Debt just hit $39 trillion

The last trillion was added in just 146 days. That’s $6.85 billion every single day. Or $79,282 every second. Interest costs now exceed $1T annually. Source: Hedgeye

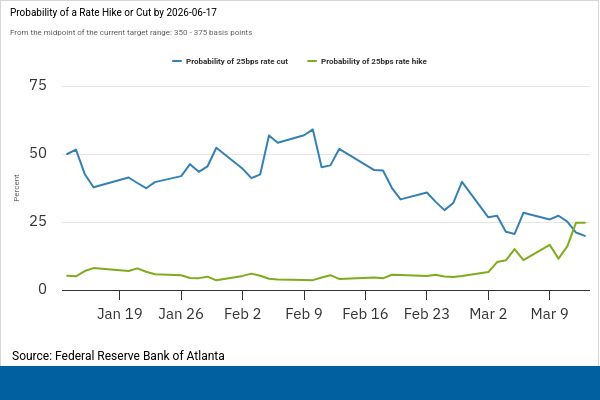

The odds of a rate hike over the next three months is now higher than the odds of a cut.

A month ago, no one would have believed this. Source: Ryan Detrick, CMT