February’s PPI inflation was HOTTER than expected, marking two consecutive PPI inflation reports that were WORST than expectations…

🔴 US February PPI • PPI MoM: +0.7% (est. +0.3%) • PPI YoY: +3.4% (est. +2.9%) • Core PPI MoM: +0.5% (est. +0.3%) • Core PPI YoY: +3.9% (est. +3.7%) ➡️ Inflation pressures remain above expectations. Market eyes now shift to Powell’s speech later today. Source: OnlyOptionsTrades

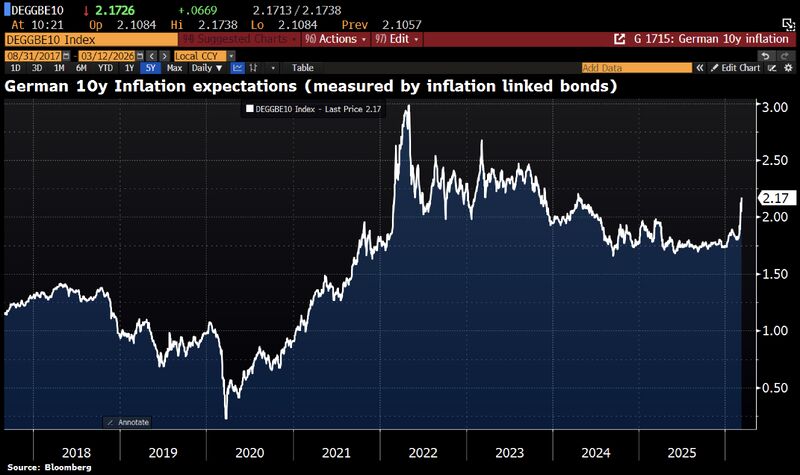

In germany, long-term inflation expectations are now rising sharply.

Over a 10y horizon, markets are pricing in inflation of 2.17%; well above the ECB’s 2% target and the highest level since 2024. Source: HolgerZ, Bloomberg

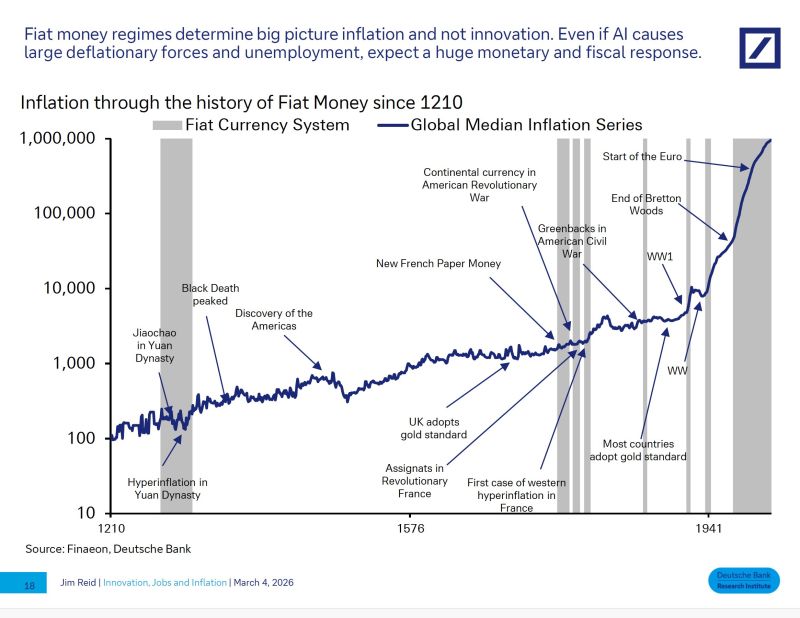

The effect of fiat money system on inflation

The KOSPI “VIX” currently trades more like an oil volatility proxy than a traditional equity vol index. Latest note on Korea here. Source: LSEG Workspace, TME

Fed Faces Uncertain Path as Inflation Data Lags Reality

February CPI data shows inflation cooling and core CPI at 2.5%, suggesting possible Fed rate cuts. But the report predates the U.S.–Iran conflict and oil spike. With softening jobs and rising energy costs, Fed policymakers face a tough March 18 decision amid conflicting signals between outdated data and current global shocks. Source: Bull Theory, Crypto Rover

Great chart by Bluekurtic Market Insights Bluekurtic -> Middle East producers have started reducing oil production.

A rise in oil prices to around $108 per barrel could add roughly 0.8 percentage points to U.S. inflation. The impact on Europe and the UK would be far more severe due to their greater dependence on energy imports.

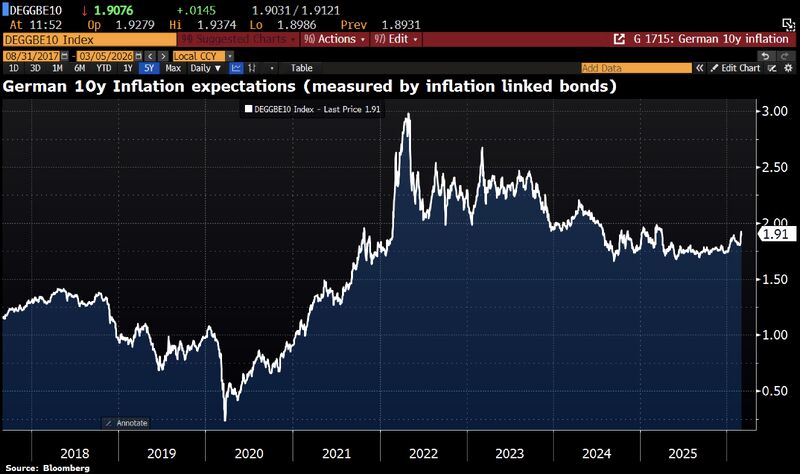

Long-term inflation expectations in Germany have barely moved despite the recent escalation in the Middle East.

The 10y breakeven inflation rate, a common market measure of expected inflation over the next decade, only nudged to 1.91%; still below the 2% threshold and well under the roughly 3% levels seen after Russia invaded Ukraine. This suggests that markets do not currently expect the conflict to have lasting inflationary effects. Source: Bloomberg, HolgerZ

Don’t lose sight of the big picture!

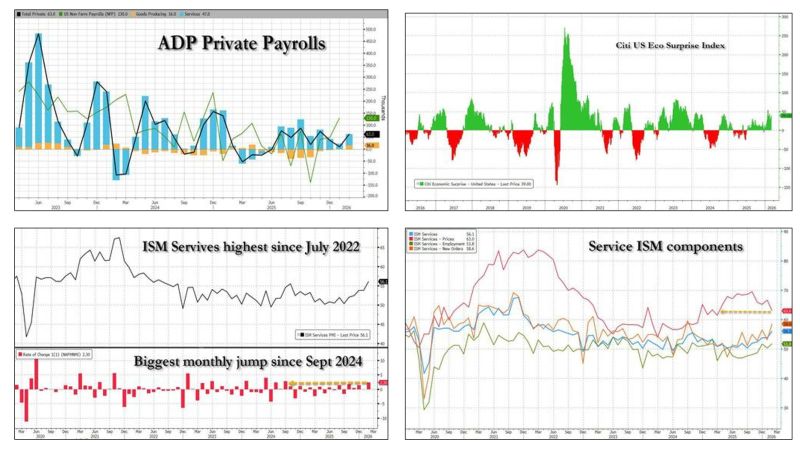

Investors are currently facing major unknowns: 1/ A major conflict in the Middle East. In this context, we believe investors should not lose sight of what we think remains a positive backdrop for stocks; 2/ The pendulum around AI which continues to swing between fear and excitement; 3/ Uncertainties about tariffs. But in this context, it is key to NOT OVERREACT to headlines and to keep in mind that the overall context remains positive for stocks: 1/ Corporate earnings continue to strengthen within and beyond AI 2/ The Fed maintains a bias toward easing 3/ The U.S. economy appears to be on track for another year of solid growth. On the later, US economic news published yesterday were impressive, starting with the solid ADP and ending with the blowout Service ISM number. The ADP number was the day's first positive surprise, as private jobs surged 3x from January and beat estimates, as they rose to 63K, the highest since November. Then it was the Service ISM print which smashed expectations (a 6-sigma beat), rising the most since Sept 2024 to the highest level since July 2022. The stagflation narrative was crushed, as the ISM's Prices Paid index tumbled to an 11 month low while everything else rose. The Citi US eco surprise index jumped from 30 to 39 in one session following the unexpectedly strong economic data. This set of very positive data was good enough to offset some of the scary news on the war front and propelled risk assets higher yesterday. Source: zerohedge

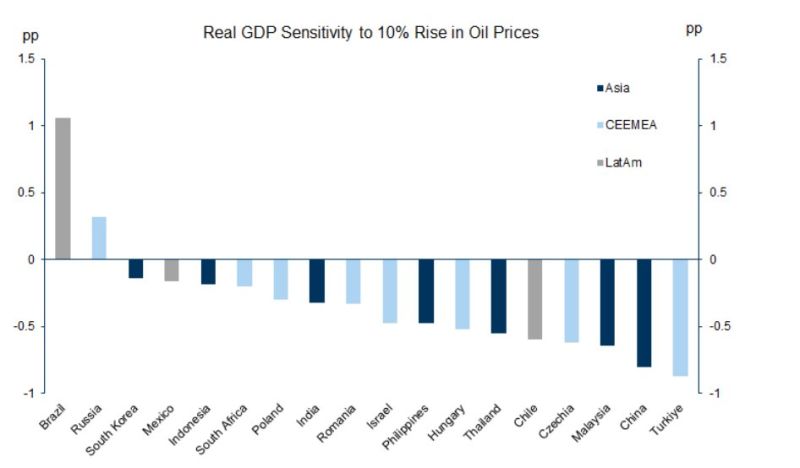

Research from Goldman shows that rising oil prices hurt emerging market economies as a whole.

While emerging markets typically depend more heavily on commodity exports compared to developed markets, they also use a greater share of commodities relative to their GDP. This makes them vulnerable to the indirect consequences of higher oil prices, such as slowed global economic growth. Noteworthy exceptions include Brazil and Russia. Source: Goldman Sachs, Markets & Mayhem