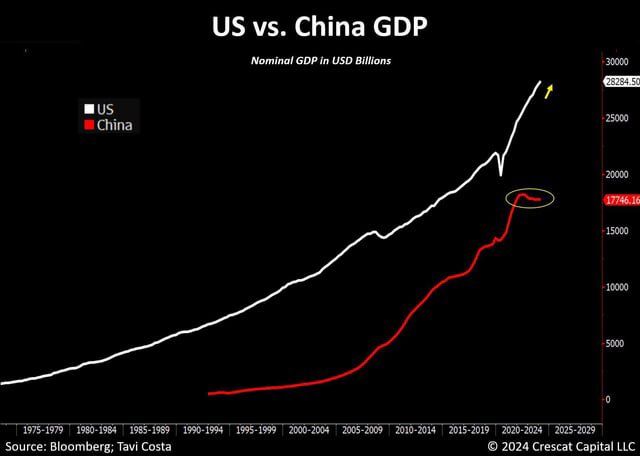

The dream of China surpassing the U.S. as the world’s largest economy is fading.

In 2021, China’s GDP was about 78% of the U.S.; by 2024, that share had fallen to roughly 64%, back to around 2017 levels, with the gap between the two economies doubling in just a few years. Note that we are talking about NOMINAL GDP. Over the last few years, the US has been generating inflation while China has been facing deflation or low inflation. This matters when you consider nominal GDP growth. Source: Terence Shen

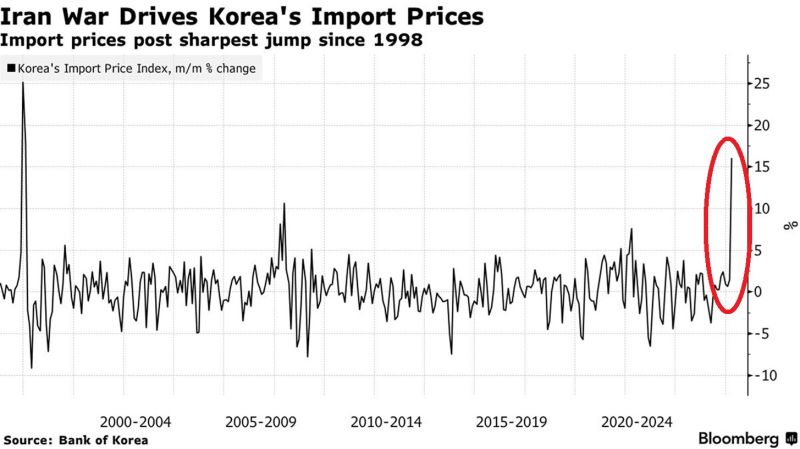

South Korea's import costs are surging at a pace not seen in nearly 30 years.

Import prices jumped +16.1% MoM and +18.4% YoY in March, the largest monthly spike since January 1998. This comes as Dubai crude oil prices nearly doubled in a month, to an average of $128.52 a barrel, while the Korean won weakened -2.6% against the US Dollar over the same period. As a result, raw material import prices, including crude and other mining products, rose more than +40% MoM, with oil-related products such as naphtha and jet fuel amplifying cost pressures for manufacturers. Higher import costs will filter through to consumer prices over time, eroding household purchasing power and dragging on domestic demand and economic growth. Source: Global Markets Investor

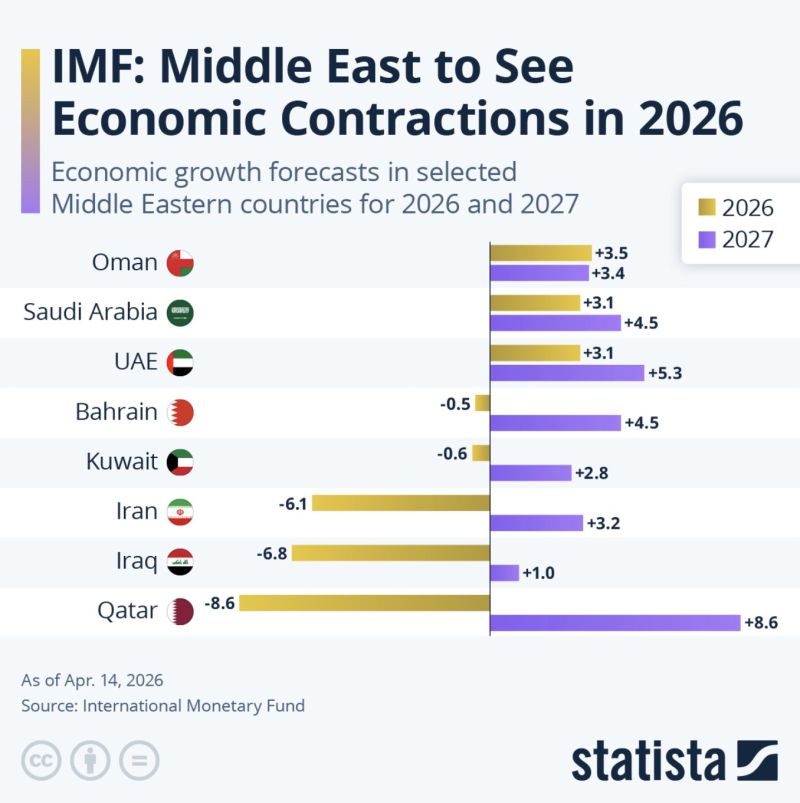

The IMF's growth forecasts are out.

Qatar seems to be the worst hit from the Middle East War, with recovery set for 2027. Source: Statista

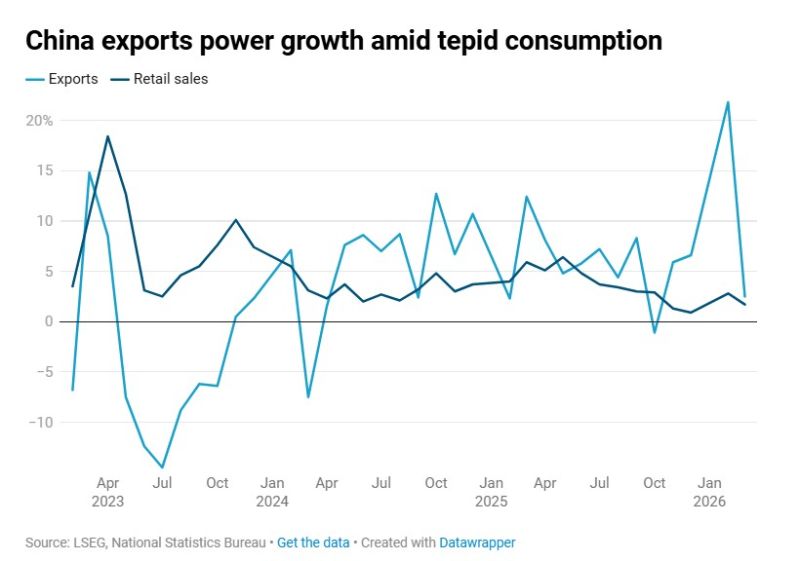

China’s economy gathered steam in the first quarter

Robust exports offset sluggish domestic consumption, though an energy shock stemming from the Iran war threatens to sap global demand and undercut that momentum. ➡️ Gross domestic product grew 5% in the three months to March, accelerating from 4.5% in the prior quarter. ➡️ Urban fixed-asset investment climbed 1.7% in the first quarter from a year earlier. ➡️ China’s retail sales grew 1.7% in March from a year earlier. Industrial output expanded 5.7%. ➡️ The urban survey-based unemployment rate in March was 5.4%, picking up from 5.3% in February. In the first quarter, China’s exports grew 14.7% from a year earlier in terms of U.S. dollars, the fastest pace since early 2022, according to EUI. That said, that growth has stalled as the Middle East conflict rages on. As the world’s largest oil importer and a heavily export-reliant economy, China is vulnerable to an oil shock that’s already slowing trade, pushing up factory costs, and darkening the outlook for the rest of the year. Source: CNBC

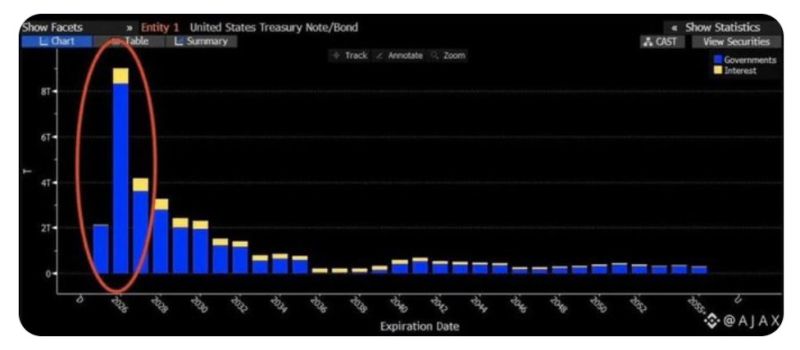

$8 TRILLION.

That’s how much US debt is coming due this year. Every dollar borrowed since 2020… Now needs to be refinanced in 2026. Back then? Interest rates were basically zero. Today? They’re staring at 4.5%+. — This isn’t just a number. It’s a pressure cooker: • $8T rolling over at higher costs • Oil prices creating fresh uncertainty • Inflation picking up again • Growth slowing down — Same debt. Very different world. And here’s the real issue: The US doesn’t just have a debt problem… It has a refinancing problem. Because when trillions reset at higher rates, everything becomes more expensive — fast. — So what’s the priority? Keep bond yields low. At all costs. Because if yields spike… This $8 trillion wave turns into something much bigger. Source: Crypto Tice

We can always use a bit of good news, right?

This chart from BofA shows that the US economy has become more and more resilient to oil shocks over time. Source: Markets & Mayhem

Talking about a K-shape economy...

The gap between Wall Street and Main Street has never been bigger: ➡️ Main Street: US consumer sentiment is down to 47.6 points, the lowest level in history. ➡️Wall Street: the S&P 500 is trading just 3% from its all-time high. ⚠️ Since the 2020 pandemic, consumer sentiment has fallen -50%. During the same period, the S&P 500 has rallied +205%. This comes as inflation, rising housing costs, and a weakening job market are increasingly squeezing the average American household. Meanwhile, 87% of all equities are held by the wealthiest 10% of households. Asset owners are the biggest winners in this economy. Source: The Kobeissi Letter, zerohedge

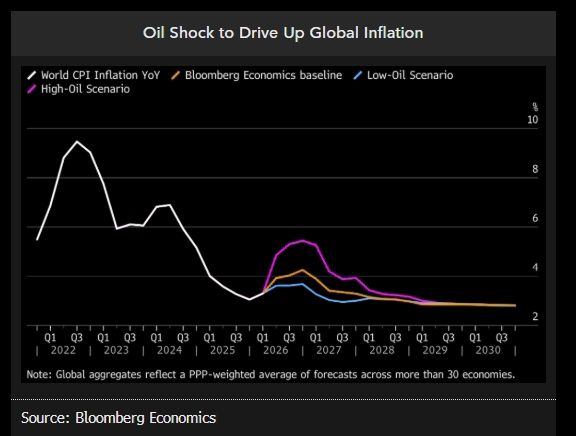

The oil shock's impact on global inflation is likely to be temporary and short-lived.

Source: Bloomberg