US Wholesale Inflation Surges in December

US wholesale inflation rose sharply in December as the producer price index (PPI) jumped 0.5% month-over-month, exceeding expectations, driven by higher service costs. Core PPI also accelerated, climbing 0.8% MoM and 3.6% YoY, well above forecasts. The surge pressures corporate margins, especially for companies lacking pricing power, and may influence inventory cycles and earnings revisions. Market reactions, particularly in bonds and high-multiple equities, often precede headline recognition, highlighting the importance of liquidity signals. Source: Bloomberg TV @BloombergTV

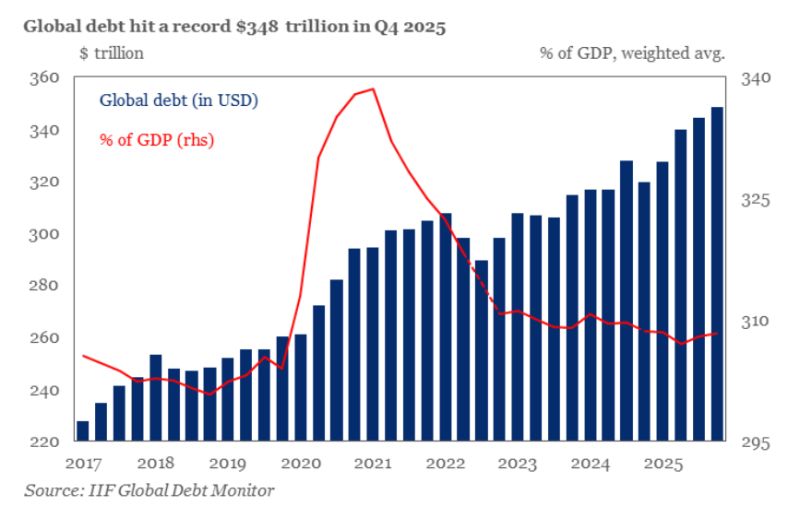

Global debt is surging as governments ramp up spending on national security and economic resilience.

Nearly $29tn was added to global debt in 2025, pushing the total to a record $348tn, according to IIF. Source: IIF, HolgerZ

The EU is freezing its trade deal with the U

The main political groups in the EU Parliament suspended legislative work on ratifying the deal on Monday, seeking clarity on Trump's new tariffs. The deal has already faced a rocky path, with the US expanding its 50% metals tariff to hundreds of additional products and Trump threatening to annex Greenland. The agreement, struck last summer, would impose a 15% tariff on most EU exports to the US while removing tariffs on US industrial goods. Source: Global Markets Investor, Bloomberg

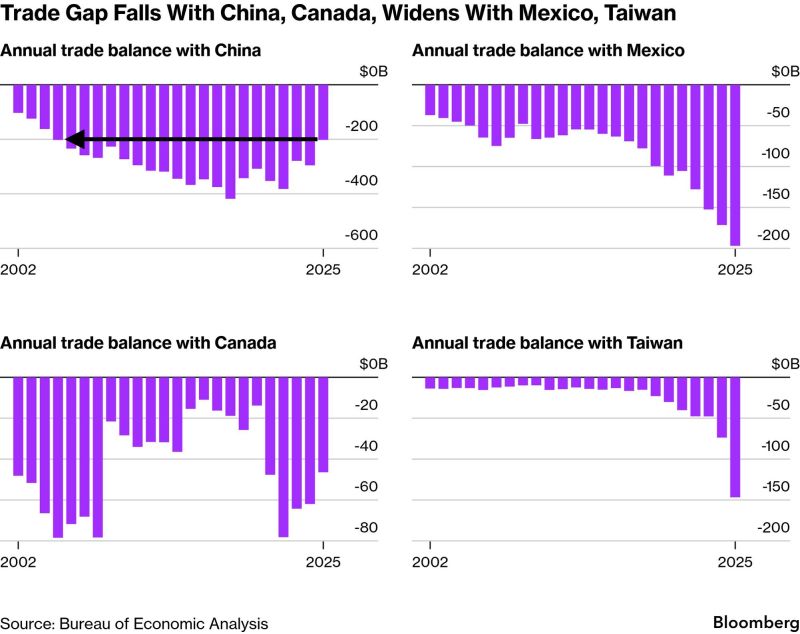

JUST IN: US Trade Deficit with China Shrinks to 21-Year Low

Source: zerohedge

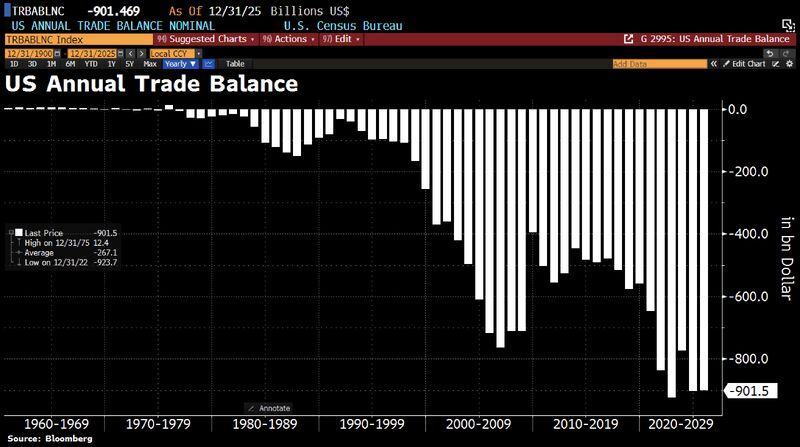

The U.S. trade deficit for 2025 remained in the red at $901.5 billion

This marks one of the largest gaps in history, slightly down (0.2%) from the $903 billion recorded in 2024, despite new tariff policies. December 2025 saw a sharp 32.6% rise in the deficit to $70.3 billion due to surging imports. Source: Bloomberg

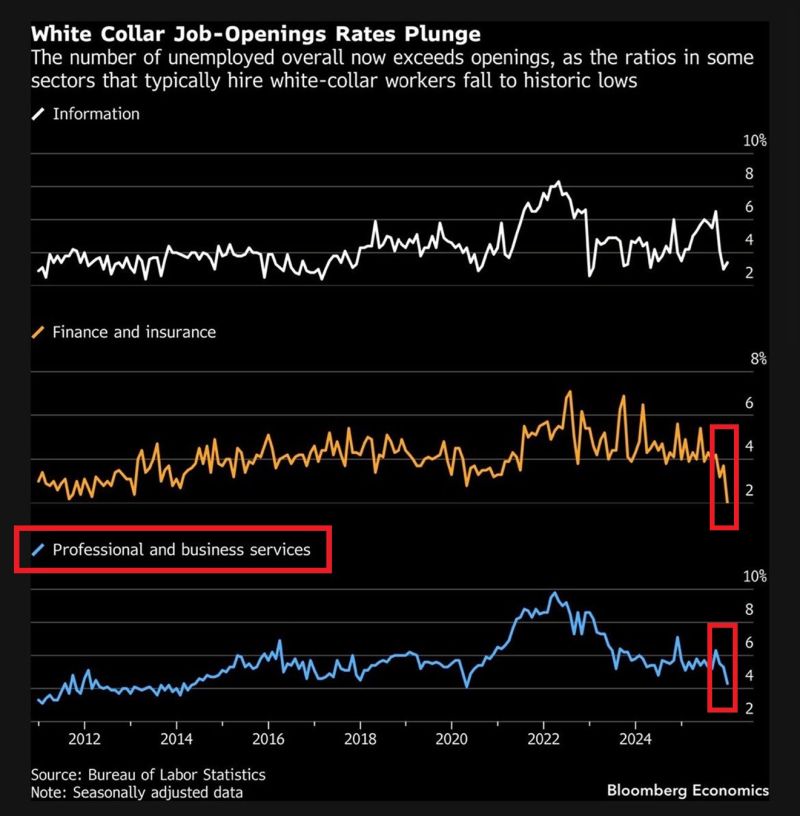

US white-collar recession is getting WORSE:

Job opening rates in key white-collar sectors are plunging to historic lows, according to BLS data. Finance and insurance rate is down to ~2%, the lowest in at least 14 years. Information sector openings are down to ~3%, near the cycle lows. Professional and business services FELL to ~4%, the 2nd-lowest in 12 years. All 3 sectors have seen openings fall -50% or more from their 2022 peaks. Source: Global Markets Investor, Bloomberg

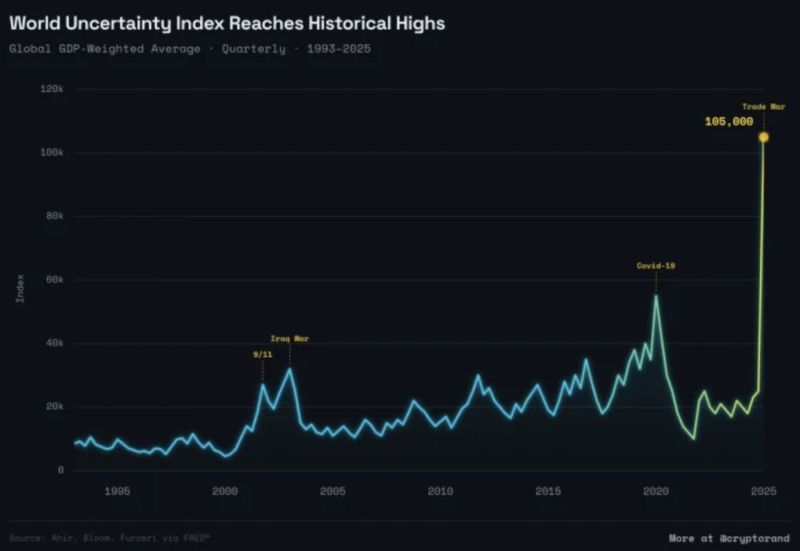

The World uncertainty index reaches the highest level in history, surpassing Covid, the Global Financial Crisis, and the Dot Com Bubble

Source: Barchart @Barchart

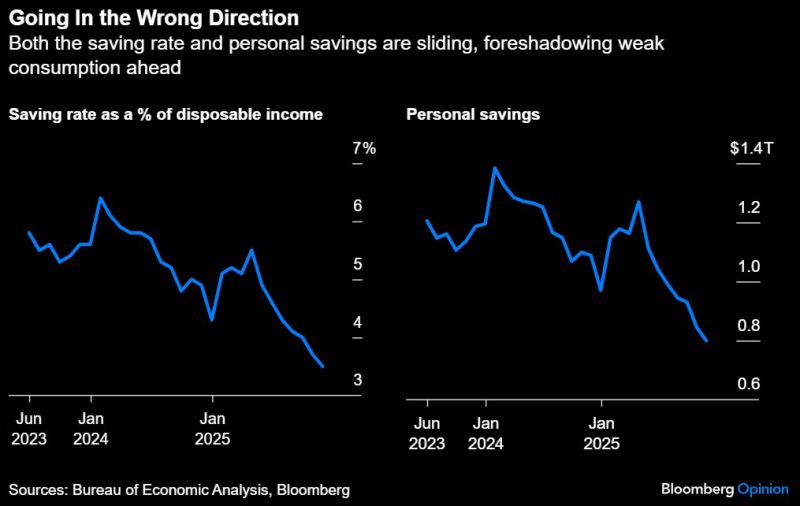

The K-Shaped Economy: Personal savings have dropped by -$469.2 billion since April, a decline of -37%.

The personal saving rate tumbled from 5.5% in April to 3.5% in November, the lowest since 2008, excluding the Covid-era distortions of 2020. Dwindling savings mean there’s less of a cushion to meet necessary payments, let alone make discretionary purchases. Delinquency rates on loans ranging from mortgages to credit cards rose to 4.8% in Q4, the highest since 2017. American's wallets are hurting. Source: Bloomberg, Hedgeye