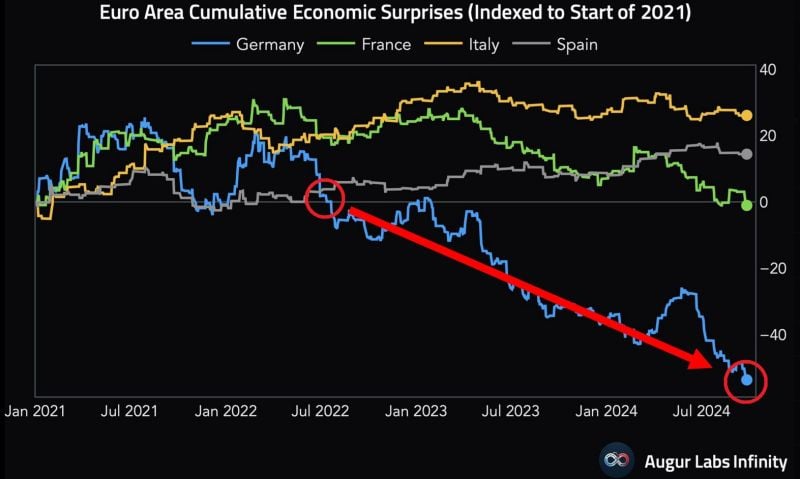

WHAT IS HAPPENING IN GERMANY ???

Most economic data in the world's third-largest economy has come below average economists' expectations over the last 2 years. Germany is also on track for 2nd straight year of SHRINKING GDP, for the 1st time since 2003. Chart: @AugurInfinity thru Global Markets Investor

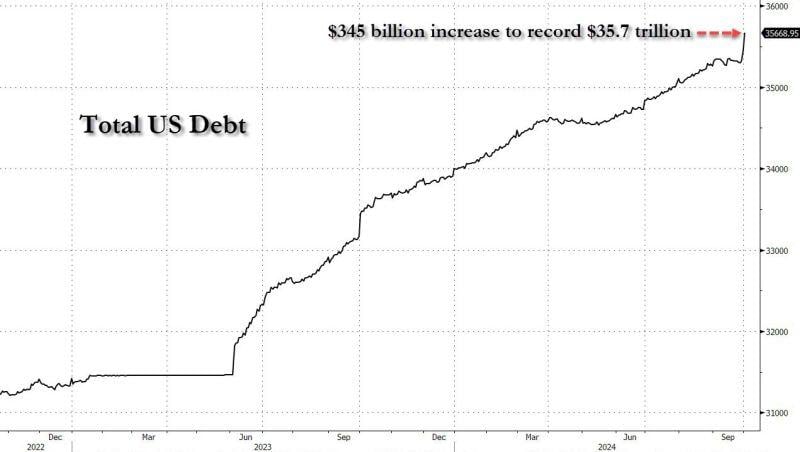

Total US debt explodes to $35.7 trillion on Oct 1, up $345 billion from Sept 27.

Source: www.zerohedge.com

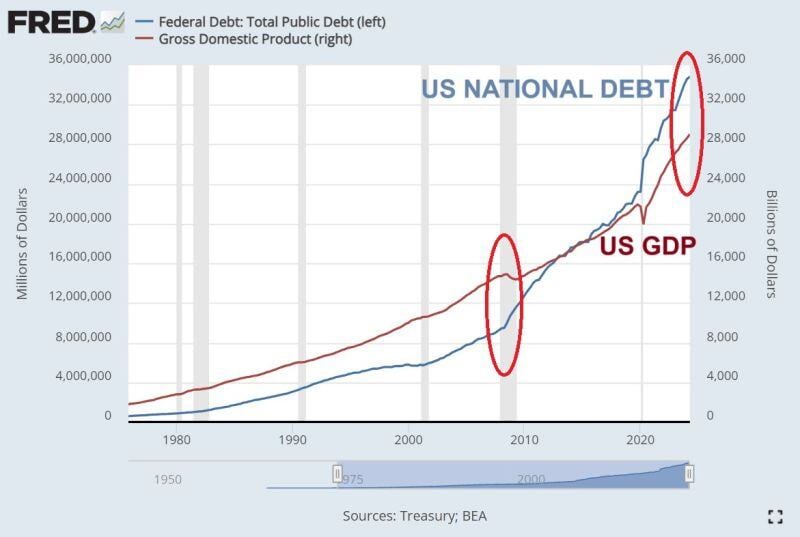

😱 The shocking chart of the day: US PUBLIC DEBT GROWTH HAS BEEN MASSIVE 😱

In 2008, the US federal debt was $9.4 trillion while the US GDP was $14.7T with the debt-to-GDP ratio at 64%. Now, the public debt is $35.7 TRILLION (Total US debt added another $345 billion between Sept 27 and October 1st...) and the US GDP is $29.0 TRILLION with the debt-to-GDP ratio at 122%... What is the pain thresold for the bond market ??? Source: Global Markets Investor, FRED

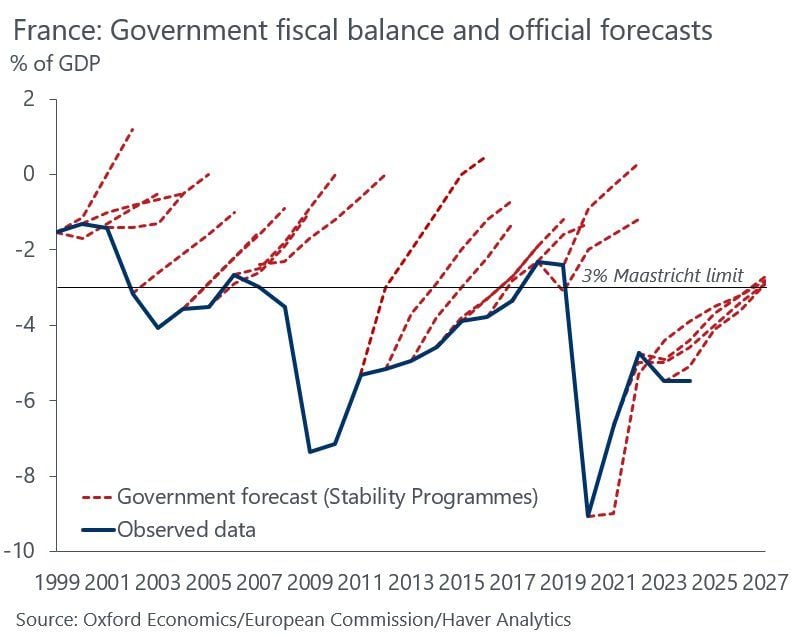

France has always missed its fiscal deficit forecasts

France has the highest tax burden in Europe, so cannot increase taxes without throttling growth. Spend is mostly pensions & local governments And with political paralysis there won’t be any structural reforms. Is a fiscal crisis looming? Source: Michel A.Arouet, Oxford Economics

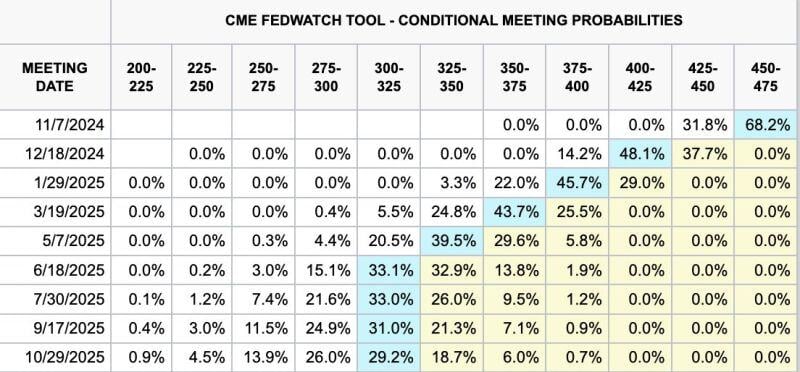

Fed Chair Jerome Powell just said the recent 50BPs interest rate cut shouldn’t be interpreted as a sign that future moves will be as aggressive - CNBC

“Looking forward, if the economy evolves broadly as expected, policy will move over time toward a more neutral stance. But we are not on any preset course,” he told the National Association for Business Economics in prepared remarks. “The risks are two-sided, and we will continue to make our decisions meeting by meeting” The market currently thinks there's a 68.2% chance Jerome Powell and the Fed cut rates by 25BPs at the next FOMC meeting Source: CME FedWatch Tool

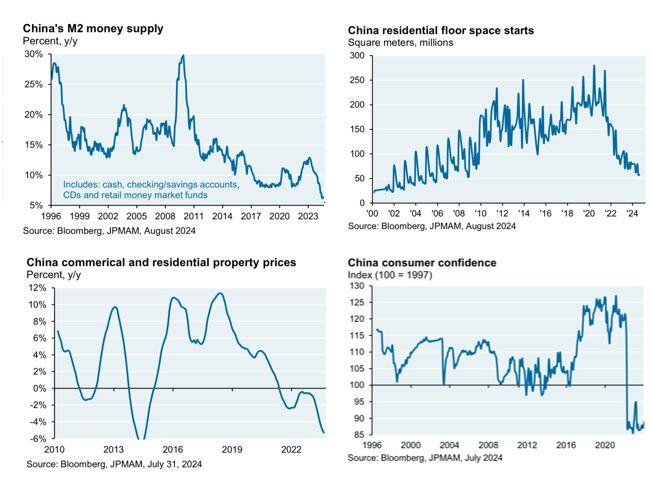

JPMORGAN, on China stimulus:

“.. I don’t think it’s an exaggeration to say that China is acting somewhat out of desperation given the severity of the declines shown in the charts below.” [Cembalest] This is very close to our thesis >>> We view this stimulus package as an emergency policy adjustment designed to halt the downward trend, NOT to engineer a higher level of economic growth going forward. The package addresses short-term risks, but medium- and long-term challenges remain: Unfavorable demographic dynamics Households’ sentiment has been hit hard in the past four years and will need time to recover durably, a necessary condition for higher domestic consumption Business and investors’ sentiment has equally been damaged by the succession of regulatory crackdowns and anti-bribery campaigns. The latest announcements are an encouraging sign for domestic and foreign equity investors, but only a small first step in rebuilding the confidence toward Chinese listed companies. Trade barriers have already increased for China’s exports to the US and Europe and this trend is unlikely to reverse, especially if Donald Trump is elected Source: Carl Quintanilla on X

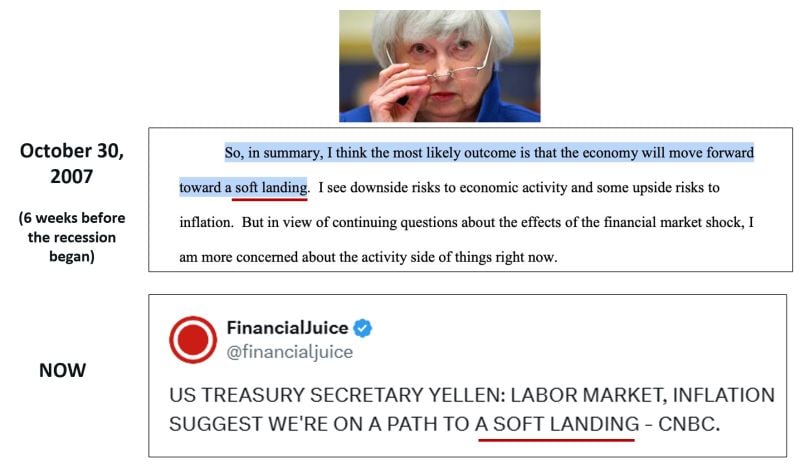

A soft landing of the US economy is our CORE scenario.

But we are well aware of the tail risk (hard landing and no landing). As a remainder, in 2007, Yellen talked about a soft landing 6 weeks before the recession began...

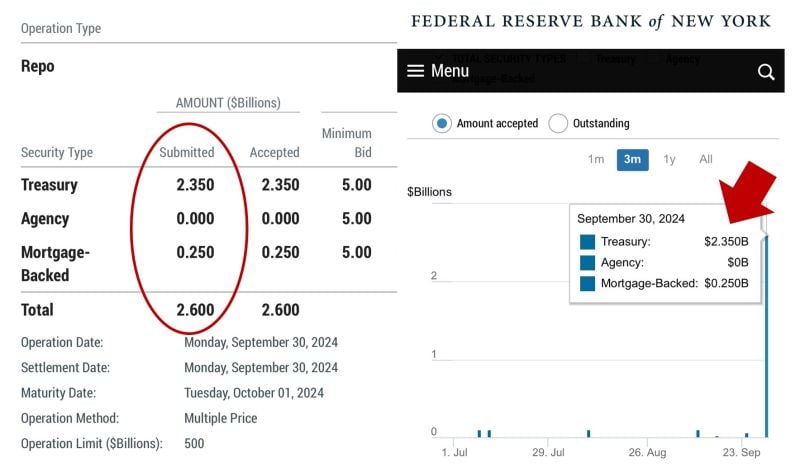

😱 The shocking chart of the day: THE FED REPO FACILITY FOR EMERGENCY LIQUIDITY HAS BEEN TAPPED FOR 2.6BN$! 😱

Is a big bank in troubles ??? Source: JustDario on X