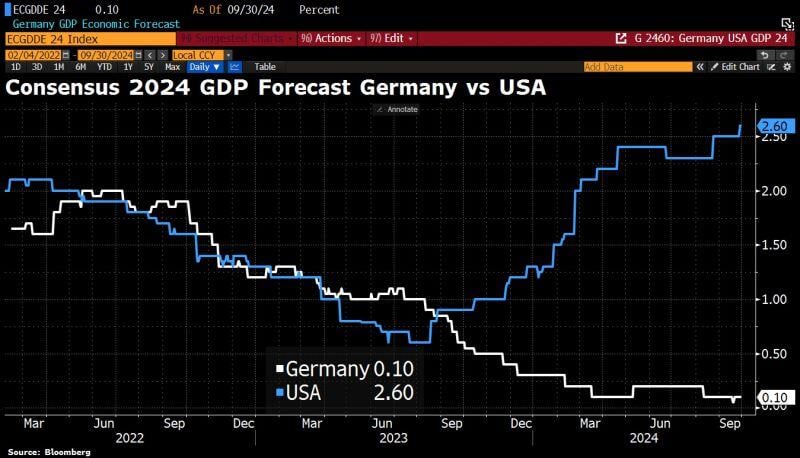

German government has abandoned hopes of achieving any economic growth in 2024.

Officials now expect stagnation at best, down from the previously projected 0.3%. This new forecast is even below consensus of +0.1%. As a result, Germany is falling further. Source: HolgerZ, Bloomberg

Global money supply is rising once again, having increased by $7.3 trillion over the past year.

That is the highest growth rate in two years. Source: Bloomberg, Tavi Costa

THE WEEK AHEAD...

👉 In the US >>> 🚨 Fed Chair Powell Speaks - Monday September ISM Manufacturing data - Tuesday JOLTs Jobs data - Tuesday ADP Nonfarm Employment data - Wednesday Initial Jobless Claims - Thursday 🚨 September Jobs Report - Friday 👉 In the rest of the world >>> 🚨 October OPEC Meeting - Wednesday In Europe, the flash CPIs will continue to come in for Germany and the Eurozone. Highlights in Asia include the Tankan survey and industrial production in Japan, as well as PMIs in China.

For those who wonder why the German economy is so important for global Macro...

As shown below, their weakening economy will impact the rest of Europe. Source: Michel A.Arouet, The World in maps

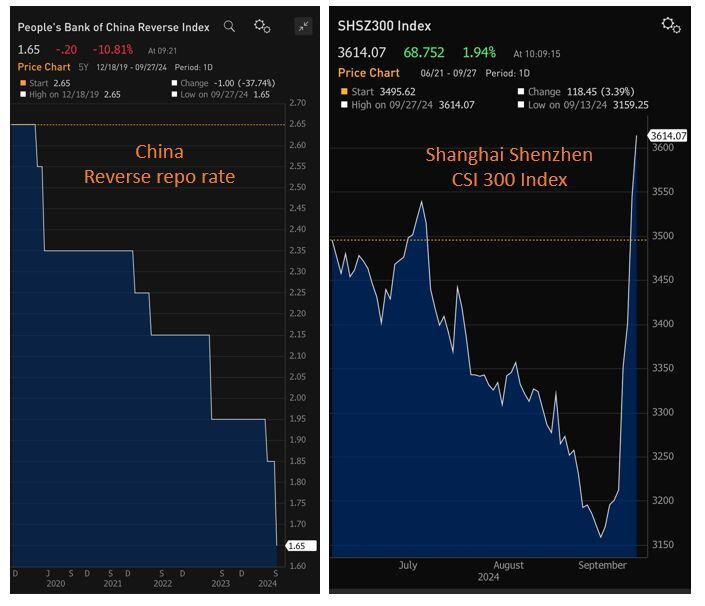

China keeps giving. Another rate cut today >>>

*PBOC CUTS 14-DAY REVERSE REPO RATE TO 1.65% FROM 1.85% Meanwhile, Chinese stocks going vertical Source: Bloomberg, David Ingles

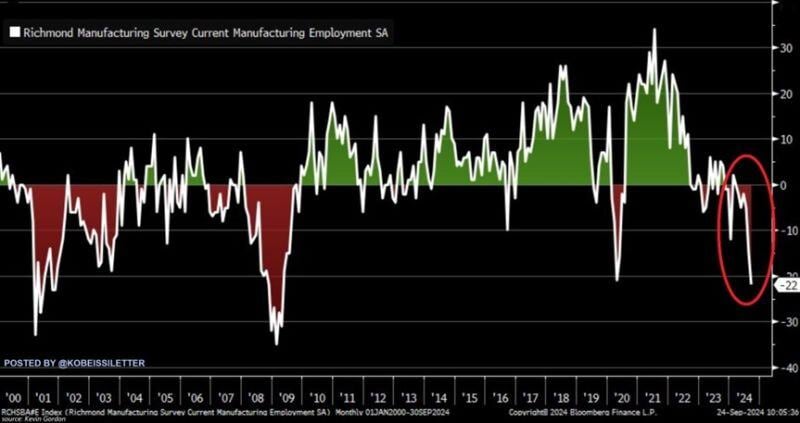

BREAKING: The Richmond Fed Manufacturing Employment Index plummeted to 21 points in September, its lowest level since April 2009.

The index has been in contraction for the majority of 2024 and even sits below pandemic lows. Furthermore, employment expectations for the next 6 months fell to -12 points, the lowest since April 2020. Overall business conditions are now at their worst since May 2020 and second-worst since 2008. Source: The Kobeissi Letter, Bloomberg

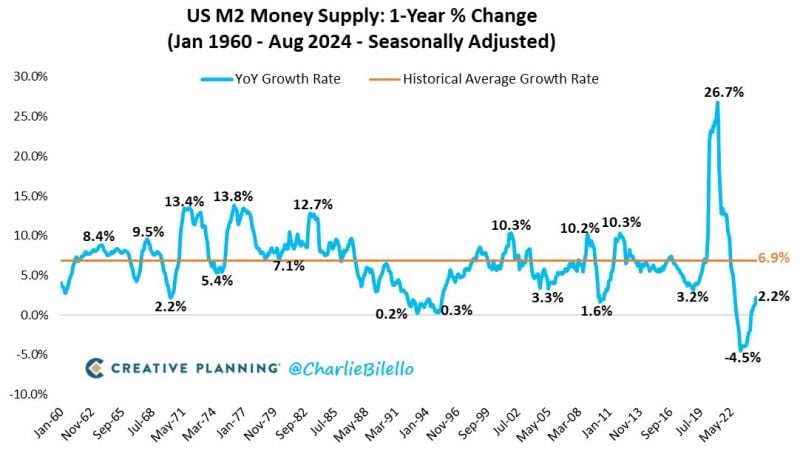

The US Money Supply grew 2.2% over the last year, the biggest YoY increase since September 2022.

The return of money printing? Source: Charlie Bilello

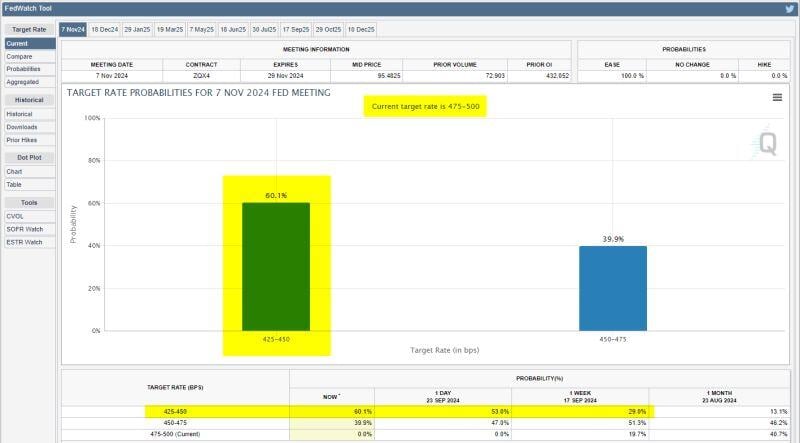

Market pricing for another 50 bps rate cut at the Fed's next meeting two days after the election is now up to 60%.

@CMEGroup