FED cuts rates by 50bp to 4.75%-5% range

The Federal Reserve lowered its benchmark interest rate by a half percentage point Wednesday, in an aggressive start to a policy shift aimed at bolstering the US labor market.Committee sees another half-point of cuts in rest of 2024Policymakers penciled in an additional percentage point of cuts in 2025, according to their median forecast.

Soft landing? Hard landing? Or no landing?

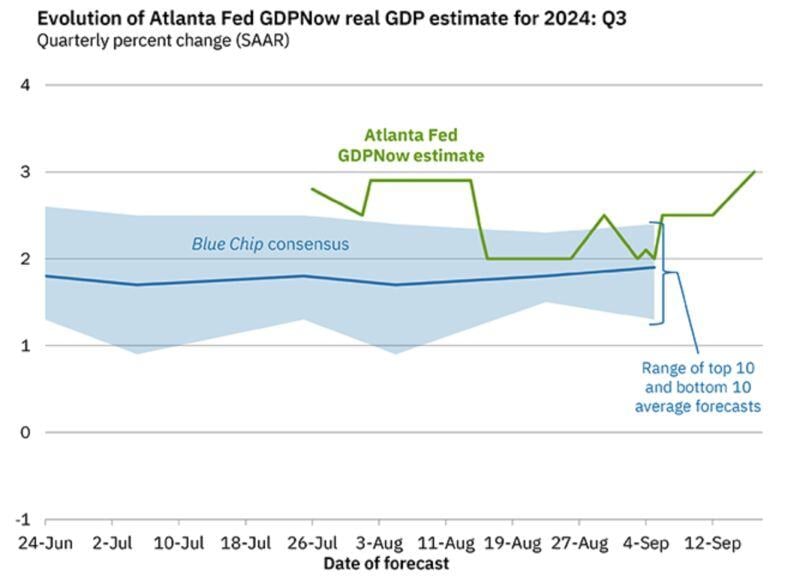

Atlanta Fed Q3 Real GDP growth Nowcast model just hit 3%...

Safe is risky. #DF24

Source: Vala Afshar @ValaAfshar on X, marketoonist.com

The US yield curve continues to steepen.

Yields on 10-year Treasuries are the highest vs 2-year yields going back to 2022. Source: Lisa Abramowitz, Bloomberg

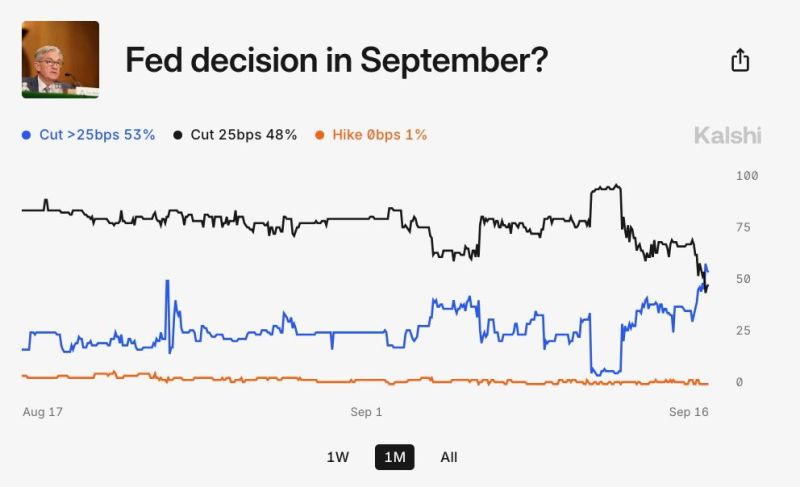

BREAKING: Prediction markets are now pricing-in a 48% chance of a 50 basis point Fed rate cut this week.

Odds of a 50 basis point rate cut have gone from 2% to 48% in just 5 days, according to Kalshi. This will be the first Fed policy decision without a 90%+ consensus since 2020... Source: The Kobeissi Letter

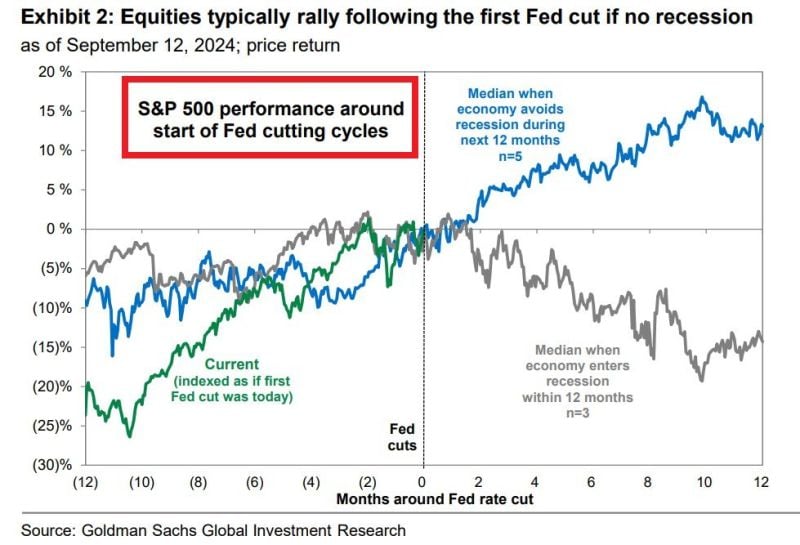

FED WILL CUT RATES ON WEDNESDAY FOR THE 1ST TIME IN 4.5 YEARS Stocks usually fall ~15% within 12 months following the 1st cut if there is a recession

If no recession, stocks rise by >10%. Key caveat is, that we will know if there was a recession a few months after the cut. Source: Global Markets Investor

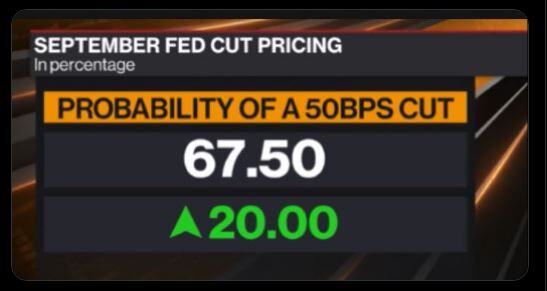

Market pricing now suggests a 50bps cut from the Fed is now base case (nearly 70% probability)

Source: Bloomberg, David Ingles

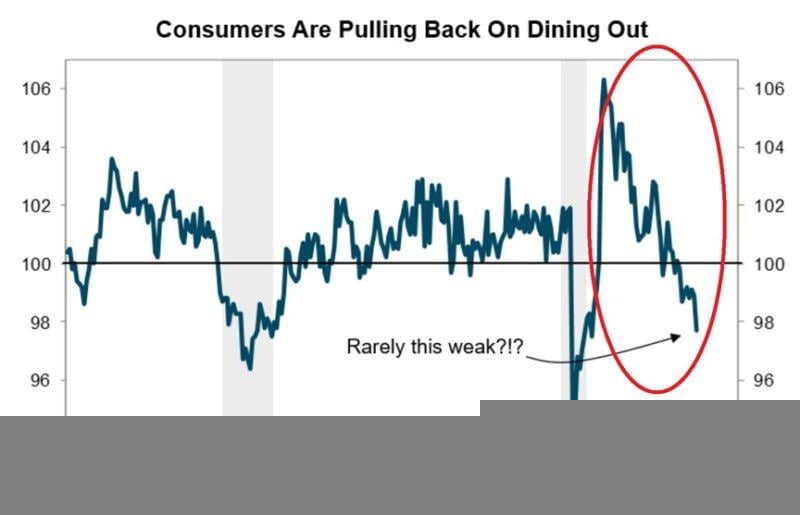

BREAKING: The Restaurant Performance Index (RPI) fell -1.3% in July to 97.7 points, the lowest level since the 2020 lockdowns

This index tracks the health of the restaurant industry in the US by measuring sales, customer traffic, labor, and overall business conditions. Since 2021, this metric has fallen by ~8.0%, marking the largest drop since it was launched in 2002. Such a low level in the index has only been seen during recessions. Americans are pulling back on dining out as prices have been sharply rising and recently hit new all-time highs. Since 2020, food prices away from home have increased by 27.0%, and fast food prices have jumped by 31.0%. Eating out is becoming a luxury... Source: The Kobeissi Letter, Trahan Macro Research