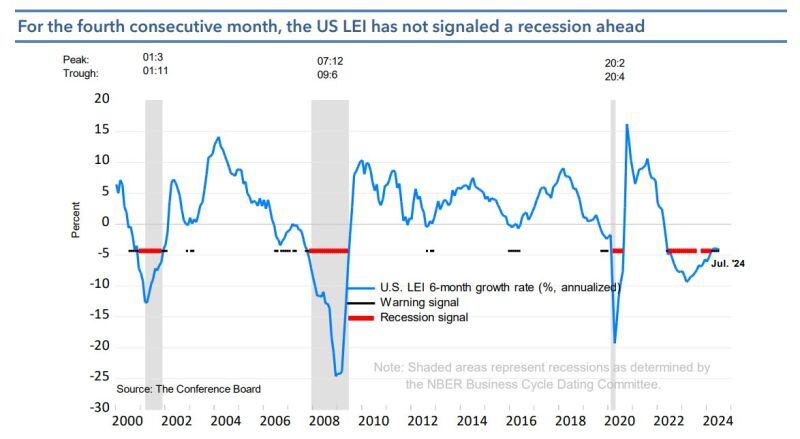

For the fourth consecutive month, the US LEI (leading indicators) has not signaled a recession ahead

Source: Mike Z.

BREAKING 🚨 Jerome Powell will indicate that the Fed is open to a 50 bps rate cut during his speech at the Jackson Hole, according to analysts from Evercore

BULLS, GET EVEN MORE EXCITED... Source: Stocktwits, www.investing.com

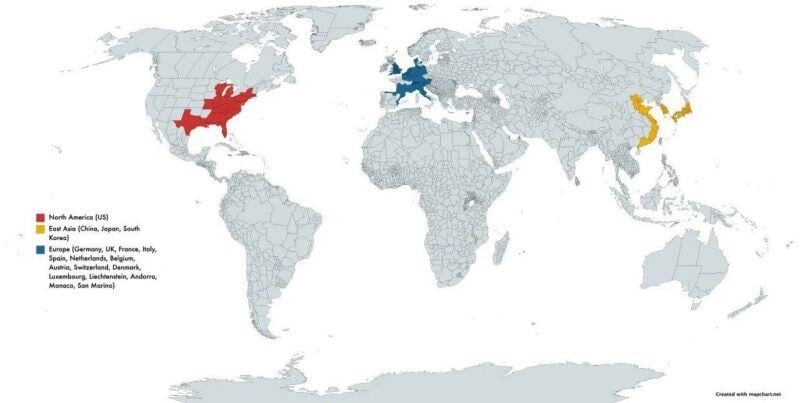

These 3 areas produce 50pct of the world's GDP

Source: Brian Roemmele

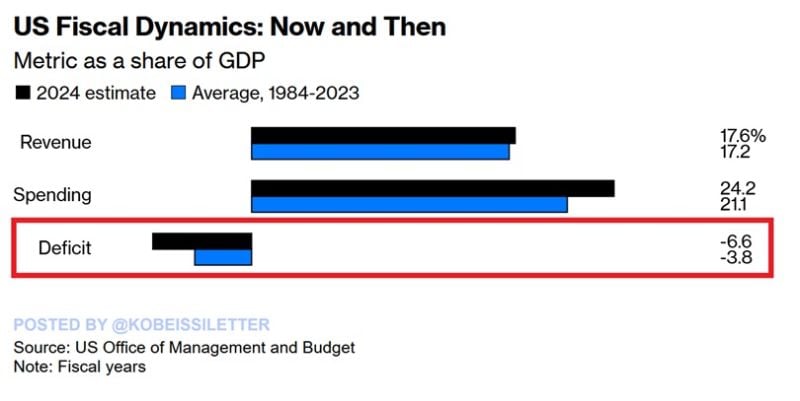

US government spending is expected to hit 24.2% of GDP in 2024, significantly above the previous 39-year average of 21.1%, according to the CBO.

At the same time, revenues are projected to reach 17.6% of GDP, just 0.4 percentage points above the 1984-2023 average. As a result, the US deficit is estimated to hit 6.6% of GDP, almost DOUBLE the 39-year average. In nominal terms, the deficit is set to hit $1.9 trillion in 2024, the highest level since 2021 when the deficit was $2.8 trillion in response to the pandemic. US government spending relative to GDP is expected to rise rapidly while revenue stagnates. Multi-trillion Dollar deficits are the new normal. Source: The Kobeissi Letter

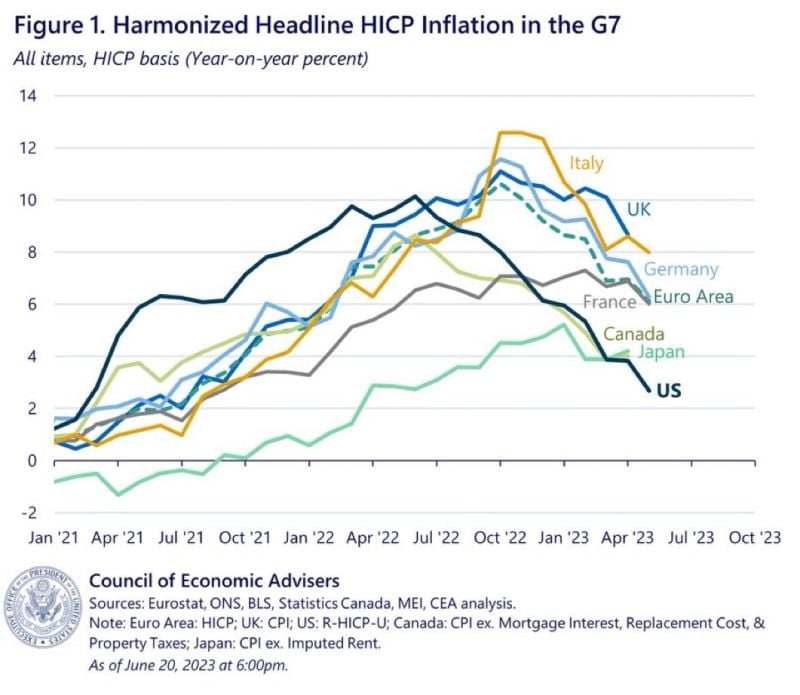

What’s the best explanation for why inflation has fallen so much more in the United States than any other G7 country?

Source: Erik Brynjolfsson @erikbryn on X

'While cyclicals have trailed defensives recently, they are still priced for an economic expansion.'

https://lnkd.in/eH8idMiZ ht @dailychartbook thru Jesse Felder on X, Bloomberg

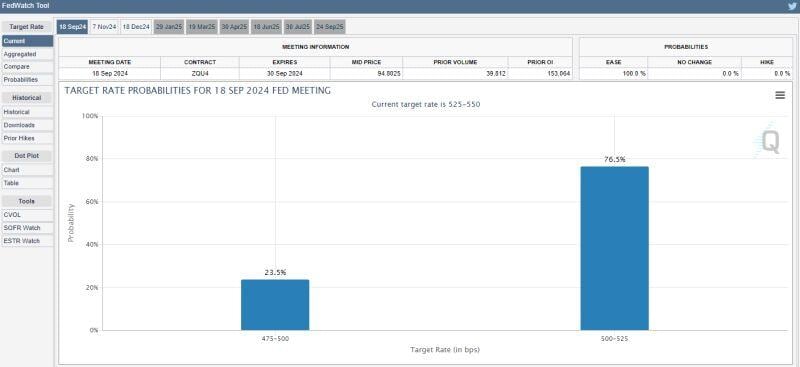

JUST IN 🚨: Odds of a 50 bps interest rate in September has plummeted to less than 25%

Source: Barchart

JP Morgan's Jamie Dimon wants to hit US millionaires with the "Buffet rule" to tackle the national debt

Source: Business Insider