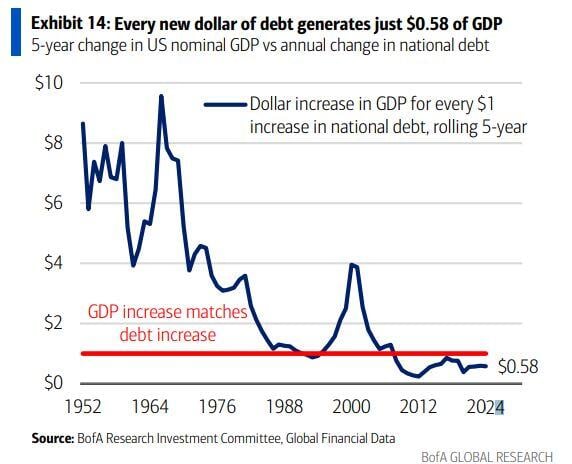

Unproductive debt...

Every new dollar of US debt generates just $0.58 of GDP Source: Mike Zaccardi, BofA

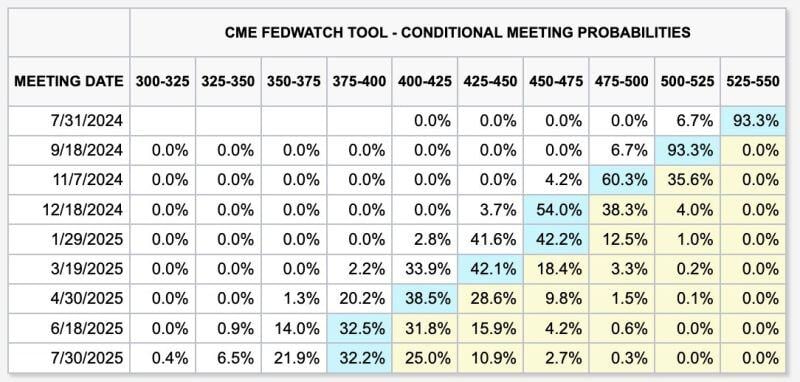

Markets now have a BASE CASE of 6 FED interest rate cuts over the next year.

The base case shows rate cuts at every meeting remaining in 2024 starting in September. Discussions of a 50 basis point interest rate cut have even begun to emerge. This feels a lot like January 2024 when the market went from pricing-in 3 rate cuts in 2024 to 7 in a matter of weeks. Source: The Kobeissi Letter, CME

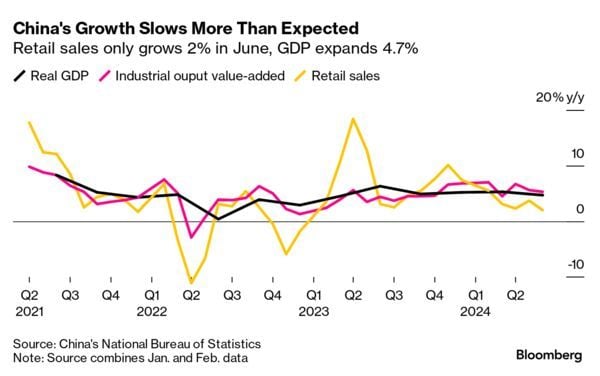

China Q2 GDP growth slowed more than expected (+4.7% yoy vs. +5.1% yoy expected), but the big surprise is just how weak retail sales were - growing only 2% in June.

-> China’s National Bureau of Statistics on Monday said the country’s second-quarter GDP rose by 4.7% year on year, missing expectations of a 5.1% growth, according to a Reuters poll. -> June retail sales also missed estimates, rising 2% compared with the 3.3% growth forecast. -> Industrial production, however, beat expectations up by 5.3% in June from a year ago, higher than Reuters estimate of 5% growth. -> Urban fixed asset investment for the first six months of the year rose by 3.9%, meeting expectations. Investment in infrastructure and manufacturing slowed their pace of growth on a year-to-date basis in June versus May, while real estate investment declined at the same 10.1% rate. The National Bureau of Statistics did not hold a press conference for the data release. China’s high-level policy meeting, the Third Plenum, kicks off Monday and is set to wrap up Thursday. Source: Bloomberg, CNBC

In Germany, the number of corporate insolvencies up by a third.

In April 2024, the local courts reported 1,906 corporate insolvencies. The courts put the creditors' claims from the corporate insolvencies reported in April 2024 at ~€11.4bn. In April 2023, the claims had totaled ~€1.3bn. Source: HolgerZ, Bloomberg

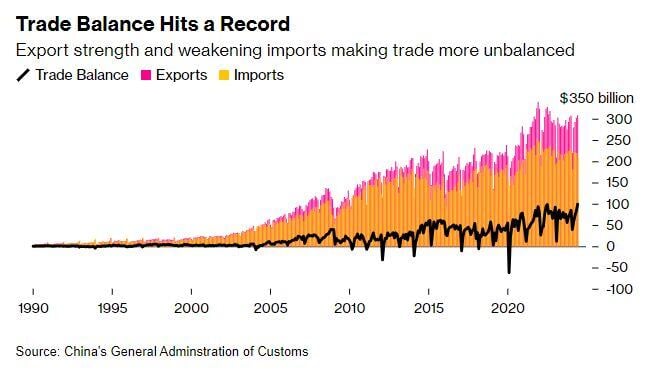

China posts biggest monthly trade surplus in at least 24 years, nearly $100B in June - Bloomberg

China’s trade surplus soared to an all-time high in June, with a jump in exports overwhelming an unexpected decline in imports and raising the risk of greater trade tensions. Exports rose to $308 billion, expanding for a third straight month to the highest level in almost two years, the customs administration said Friday. Imports fell to $209 billion, leaving a record trade surplus of $99 billion for the month. The growing imbalance has spooked China’s trade partners, who have responded with more tariffs on Chinese imports including electric vehicles. This tension has worsened ties between the European Union and Beijing, which this week opened a tit-for-tat probe into the EU’s trade barriers in what could bring the economies closer to a trade war. The surplus “reflects the economic condition in China, with weak domestic demand and strong production capacity relying on exports,” said Zhiwei Zhang, president and chief economist of Pinpoint Asset Management. However, “the sustainability of strong exports is a major risk for China’s economy in the second half of the year. The economy in the US is weakening. Trade conflicts are getting worse.” Source: Bloomberg

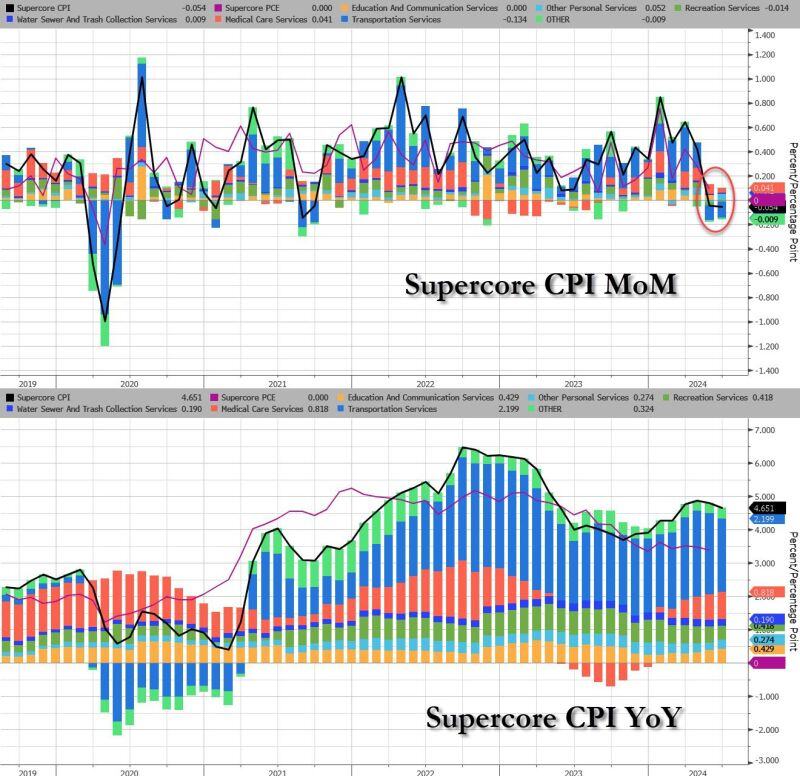

US supercore CPI is negative MoM for the 2nd month in a row

zerohedge.com, Bloomberg

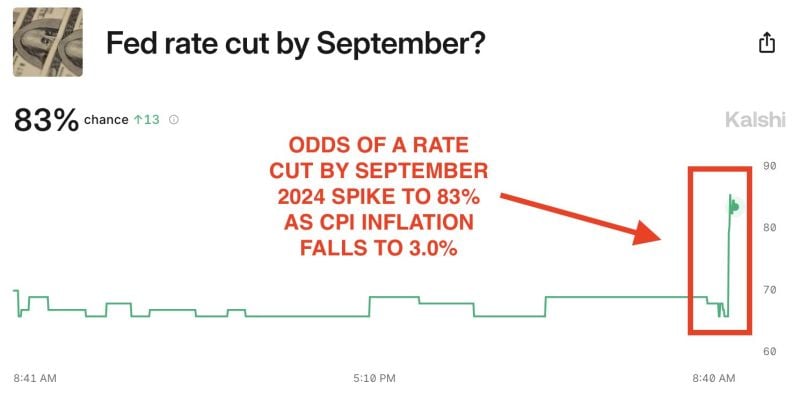

BREAKING: Odds of a Fed rate cut by September 2024 skyrocket to 83% after June CPI inflation, according to Kalshi.

June 2024 marked the first NEGATIVE month-over-month inflation print since May 2020. Headline inflation is now at a 12-month low and 100 basis points away from the Fed's 2% target. Prior to the CPI inflation report today, prediction markets saw a 67% chance of rate cuts by September. Exactly 1 year ago, the Fed stopped raising interest rates. Does the Fed have the green light to cut rates? Source: The Kobeissi Letter

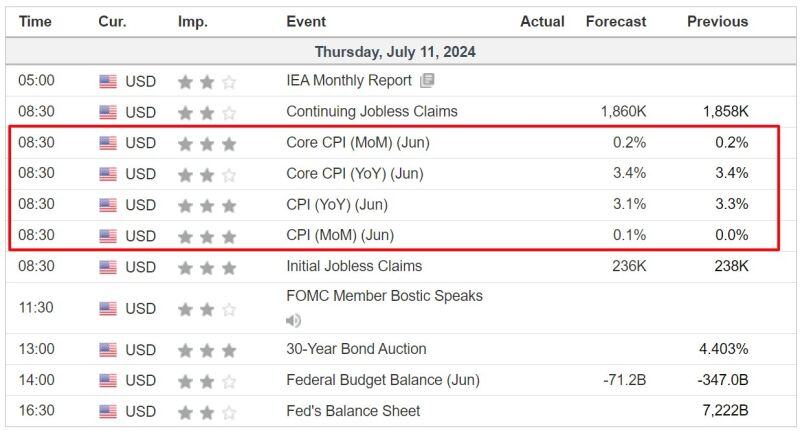

🚨 BREAKING NEWS: US CPI for June just came in at -0.1% MoM below expectations of 0.1% MoM

US CPI for June just came in at +3% YoY below expectations of +3.4% YoY Core CPI inflation fell to 3.3%, below expectations of 3.4%. This marks the 39th consecutive month with inflation at or above 3%. It's also the 3rd straight month with declining CPI inflation. Looks like a September rate cut is coming. Source: Jesse Cohen