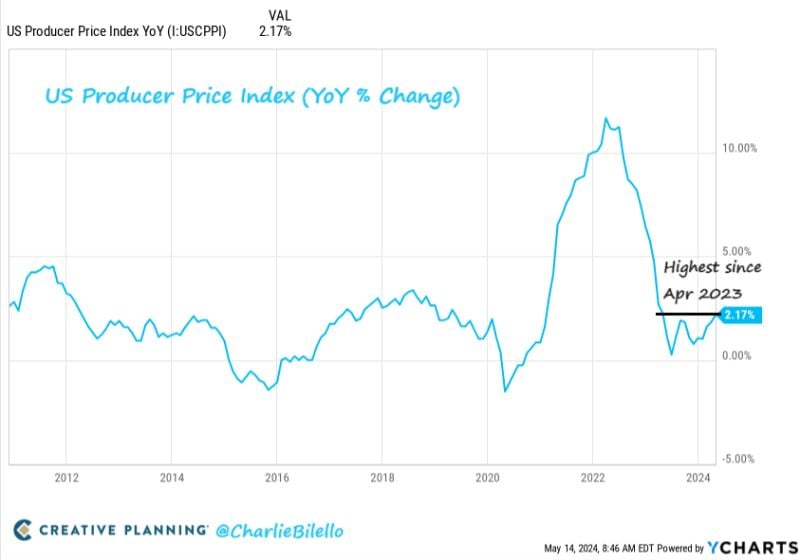

BREAKING: April PPI inflation RISES to 2.2%, in-line with expectations of 2.2%

Core PPI inflation was 2.4%, in-line with expectations of 2.4%. PPI inflation is now up for 3 straight months for the first time since April 2022. This is the highest PPI reading since April 2023. Note that revisions from last month’s PPI left people feeling it wasn’t as “hot” as initially thought on headline numbers. Source: Charlie Bilello

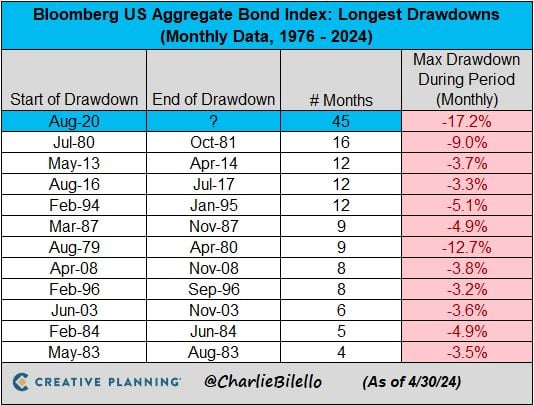

The US Bond Market has now been in a drawdown for 45 months, by far the longest bond bear market in history

Source: Charlie Bilello

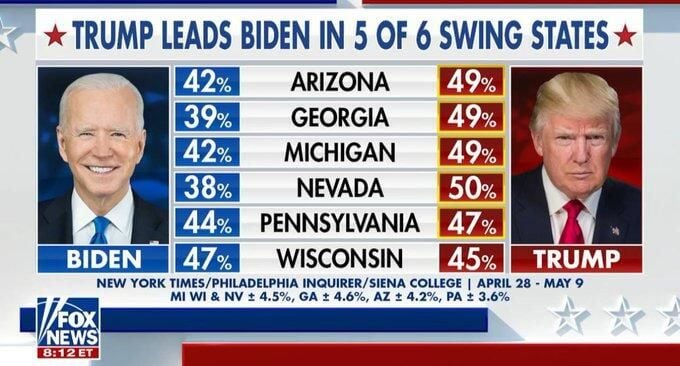

A new set of polls reveals that Donald Trump is leading President Biden in five out of six critical battleground states

as young and non-white voters grow increasingly dissatisfied with the current president. Source: www.zerohedge.com, FoxNews

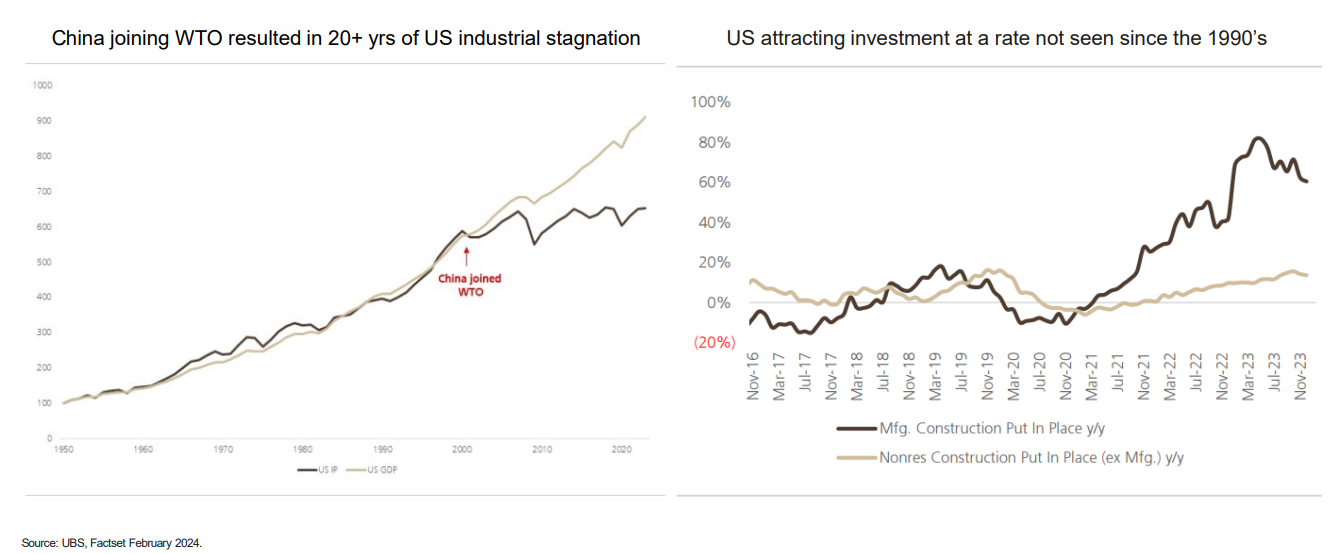

Trends in reshoring, electrification and AI are propelling US investment renaissance

Source: BNP Paribas Asset Management

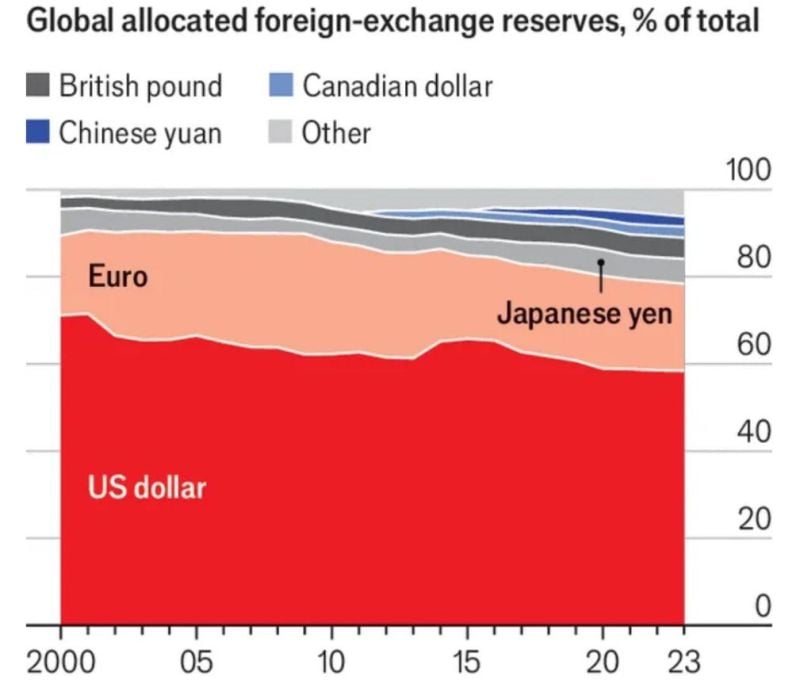

Global foreign exchange reserves.

The US dollar still dominates but share has been eroding sligthly Source: Michel A.Arouet

In case you missed it...

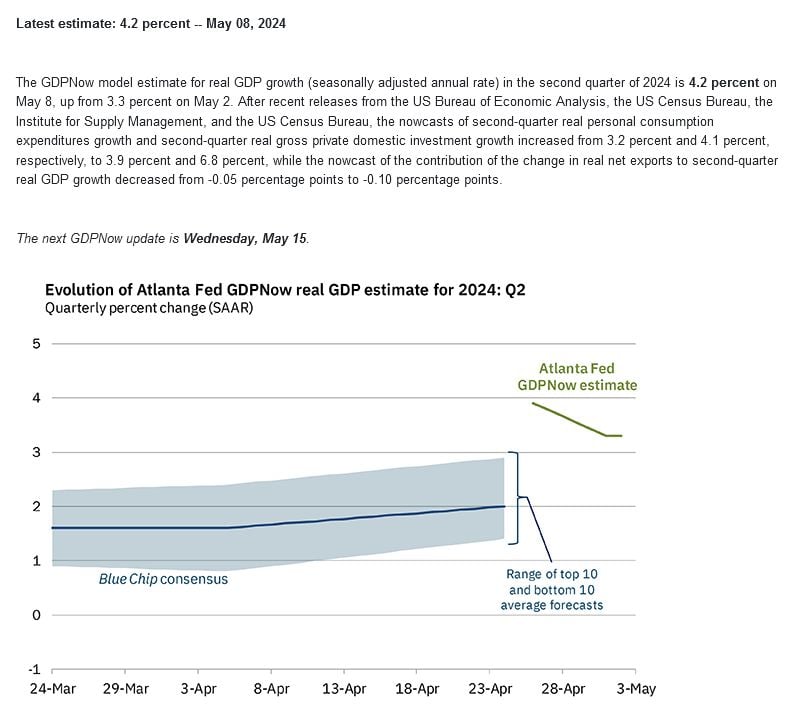

Atlanta Fed US Q2 GDP Now latest 4.18%, vs last 3.31%...

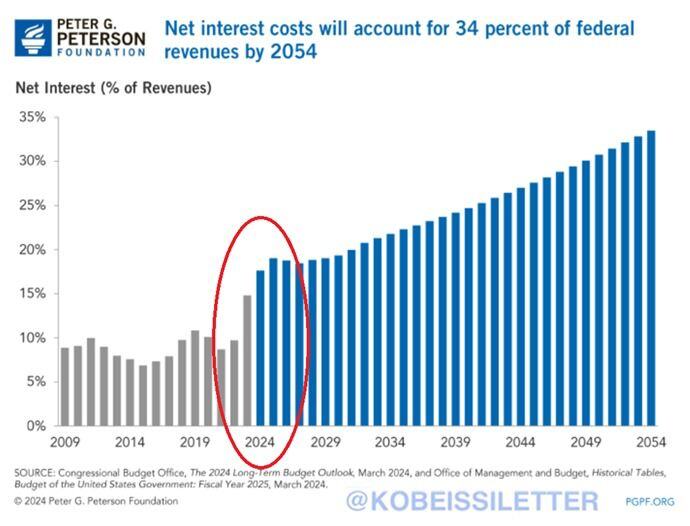

Shocking stat of the day by The Kobeissi Letter:

US net interest payments as a percentage of federal revenues are set to reach 34% by 2054. This means that ONE THIRD of all government revenue would be spent only to service the national debt. Over the past 8 years, the percentage has already doubled to ~15% and is at its highest in 3 decades. Meanwhile, nominal annualized interest payments have crossed above $1 trillion for the first time ever. We could see $1.6 trillion in annual interest expense by the end of the year if the Fed leaves rates steady. The US government needs lower interest rates more than anyone - i.e Fiscal policy leads monetary policy. Source: The Kobeissi Letter, Peter G.Peterson

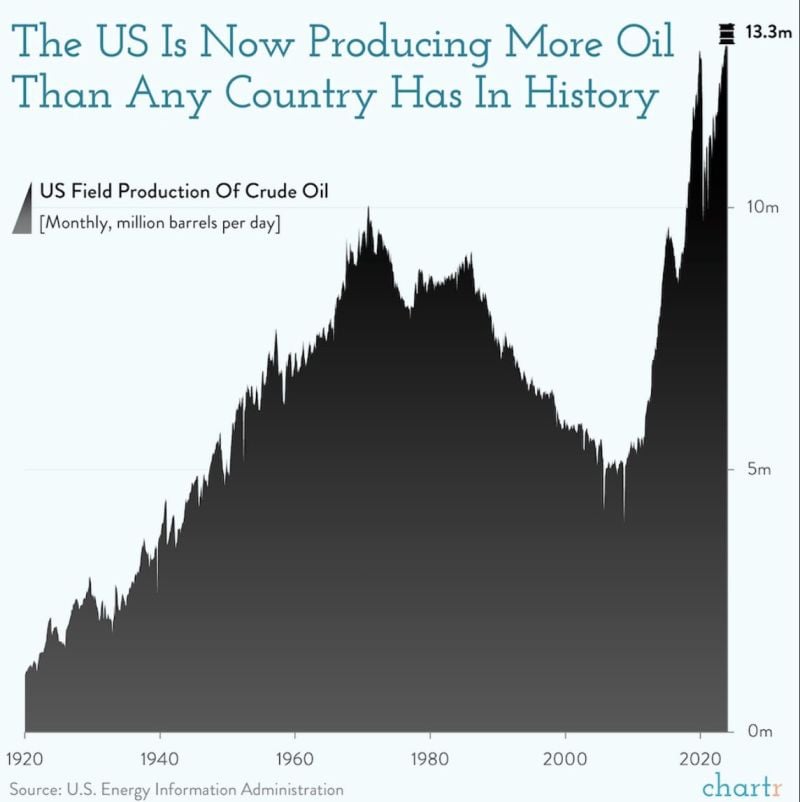

And the Winner is…

Source: Chartr