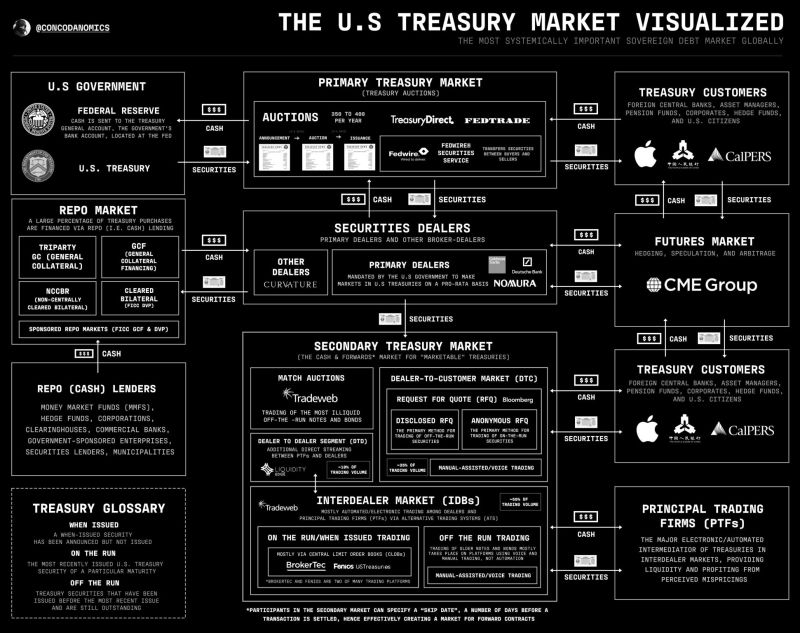

The U.S. Treasury market visualized

Source: X @concodanomics thru Audrey Wang, CFA🇭🇰

Prospective California homeowners currently in the market would need to make $221,200 annually to qualify to purchase a median-price, single-story home in California, typically costing $843,600

The latest figures show that California’s housing affordability rates continue to decrease. The figures released during the third quarter are down from 16% in the second quarter of 2023. For comparison, about 56% of California home buyers could afford a home during the first quarter of 2012, the index’s peak high. Source: Wall Street Silver

The richsession...

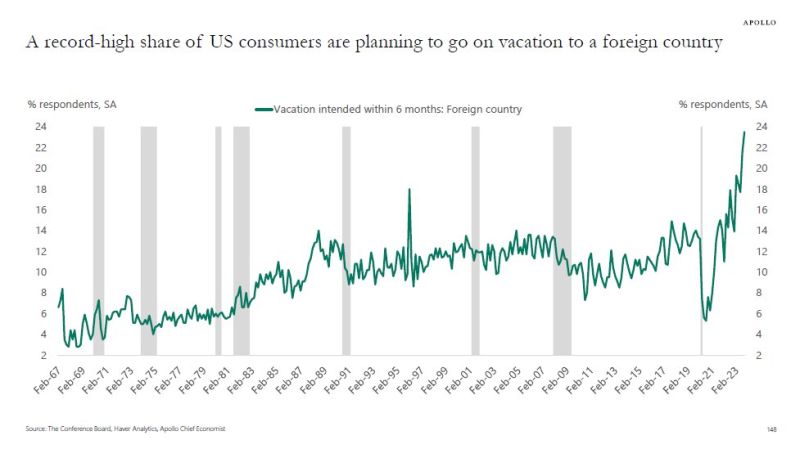

A record-high share of US consumers are planning to go on vacation to a foreign country within the next six months. Via Apollo/Slok

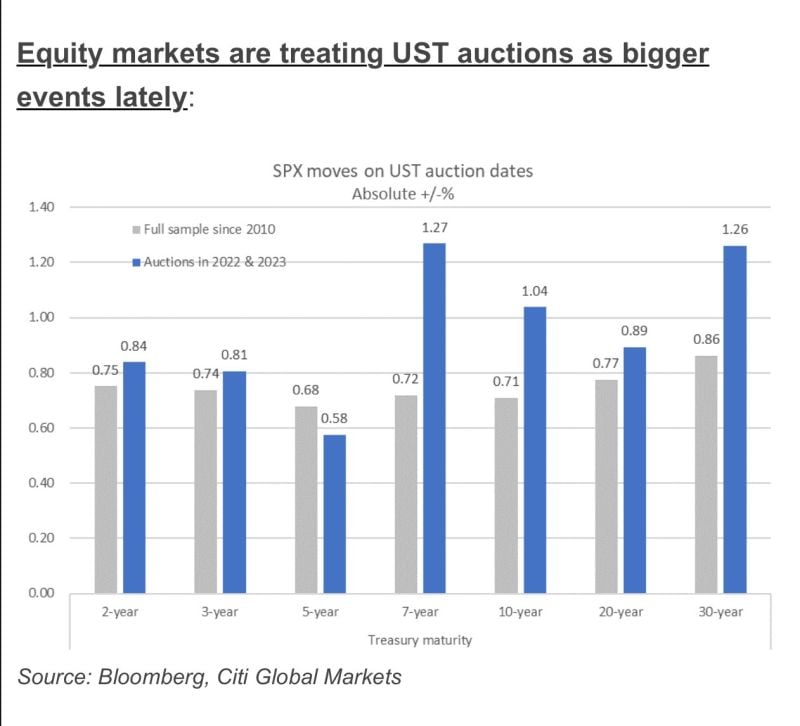

Stock markets care much more about US Treasury auctions now than they used to

Chart from Citi’s Stuart Kaiser thus Lisa Abramowitz

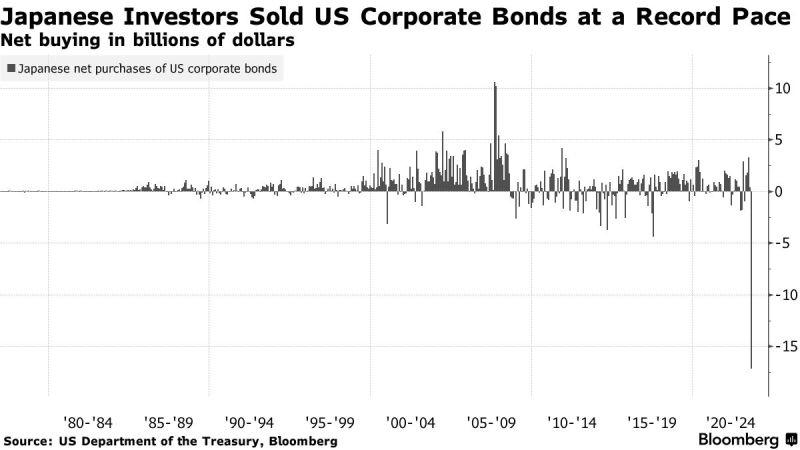

Japanese investors are selling US corporate debt at a record pace 👀

Source: Bloomberg

U.S. Banks have fallen to an all-time low against the S&P 500

Source: FT, Barchart

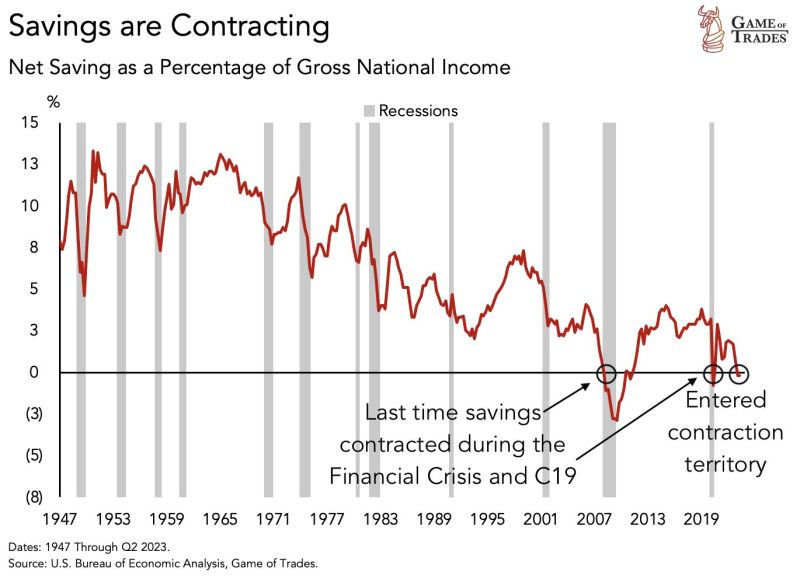

This has happened ONLY 2 times in the last 75 years. In the US, savings as a % of income is now contracting, indicating that people are find it VERY hard to save

The last 2 contractions happened in: - 2008 - 2020 High interest rate + high debt is a MAJOR problem for people Source: Game of Trades

Moody’s cuts U.S. credit outlook from stable to negative. Will markets just shrug it off on Monday?

Source: Trend Spider