National Capitalism and the Trump Effect on Investment Pledges in the US 👇

Hyundai — $20 Billion UAE — $1.4 Trillion Saudi Arabia — $600 Billion Apple — $500 Billion Softbank, Open AI, Oracle — $100 Billion Nvidia — $100 Billion + Johnson & Johnson — $55 Billion Taiwan Semiconductor — $100 Billlion CMA CGM Group — $20 Billion Eli Lilly — $27 Billion Merck — $1 Billion GE Aerospace — $1 Billion Roughly $ 3 Trillion in new direct investment into America in the first few weeks of the Trump Administration. Source: Charlie Kirk @charliekirk11, FoxNews

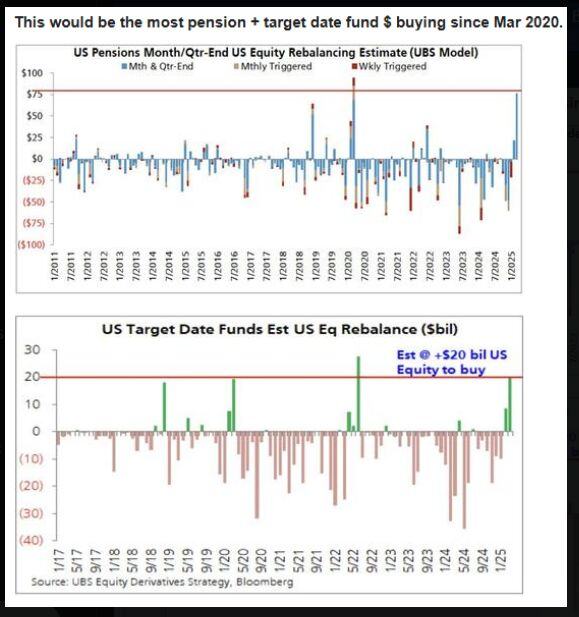

📢 Pension Funds and Target Funds could buy a combined $105 Billion of U.S. Stocks for monthly/quarterly rebalancing, according to UBS 🚀 🚀🚀

Source: Barchart

A major theme for the years to come...

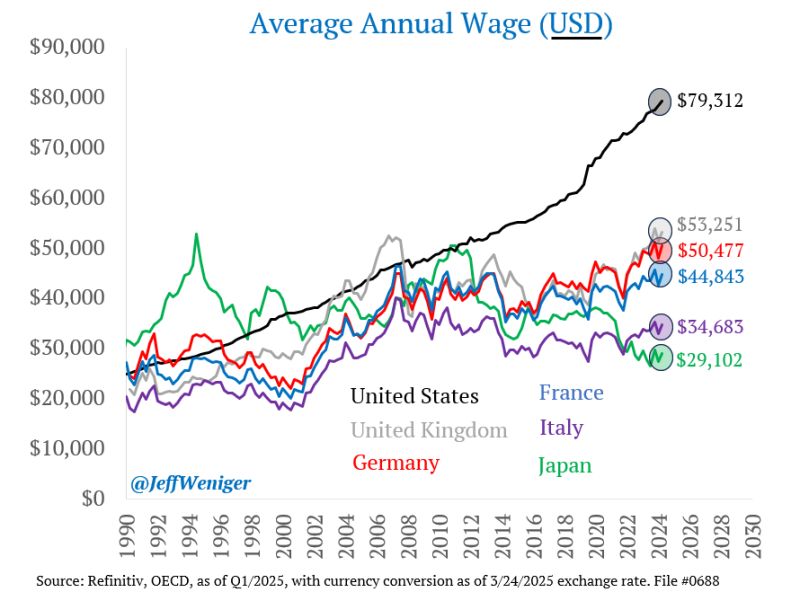

A massive wage arbitrage has opened between the US and its competitors. The overwhelming majority of people in the US have no idea just how much more money they make than the Japanese, French, British, etc. Source: Jeff Weniger

U.S. Earnings Revisions Index from @Citi has been negative for 13 consecutive weeks.

Source: Liz Ann Sonders, Bloomberg

The army of retail investors is fighting the US stock market:

Mom-and-pop investors have bought US equities for 7 days STRAIGHT ending Wednesday. Individuals have sold stocks on net only in 7 trading sessions out of 52 in 2025. Is the army of retail investors going to win? Source: Global Markets Investor @GlobalMktObserv

US tariffs on April 2nd: Will it be not as bad as expected?

A “Trump put” ahead? Some articles caught a lot of bullish notice this weekend. S&P Futures are going UP this morning Source: Bloomberg, WSJ

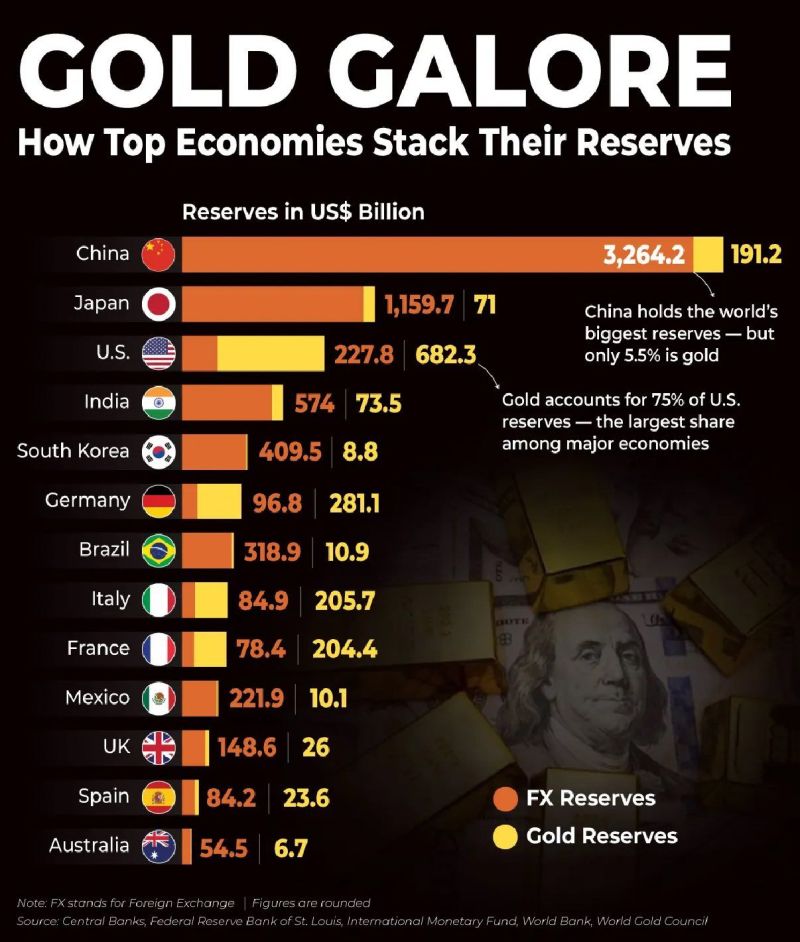

How Top Economies Stack Their Reserves...

Gold account for 75% of US reserves, the largest share among major economies. China holds the world's biggest reserves - but only 5.5% is gold... Source: Brad Moseley

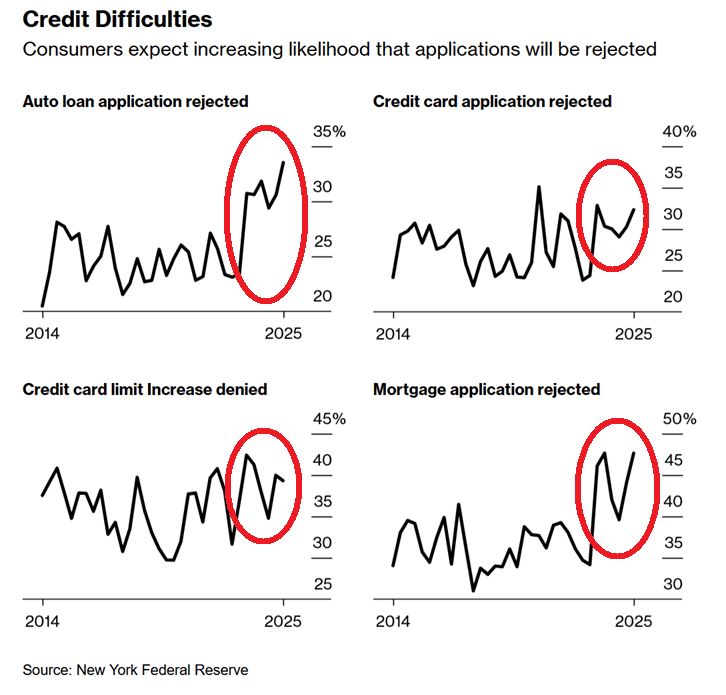

Americans expect credit application REJECTIONS at a higher rate than ever:

The perceived likelihood of credit application rejections: Auto loan: 34%, the highest on record Mortgage: 48%, the highest on record Credit card: 32%, the 3rd-highest ever Card limit increase: 39% Source: Global Market Investors, Bloomberg