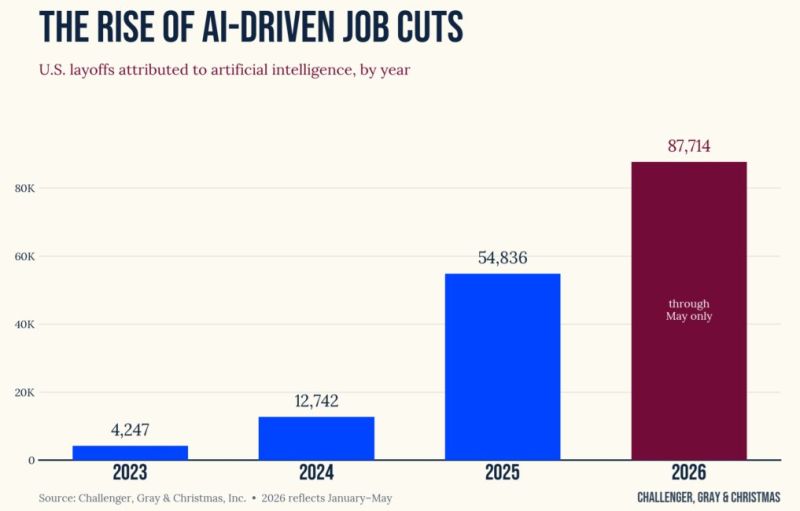

For the 3rd month in row, AI was the #1 reason for job cuts in the US.

88k job cuts were attributed to AI so far this year, a 60% increase over the AI-driven job cuts in all of 2025. Source: Charlie Bilello

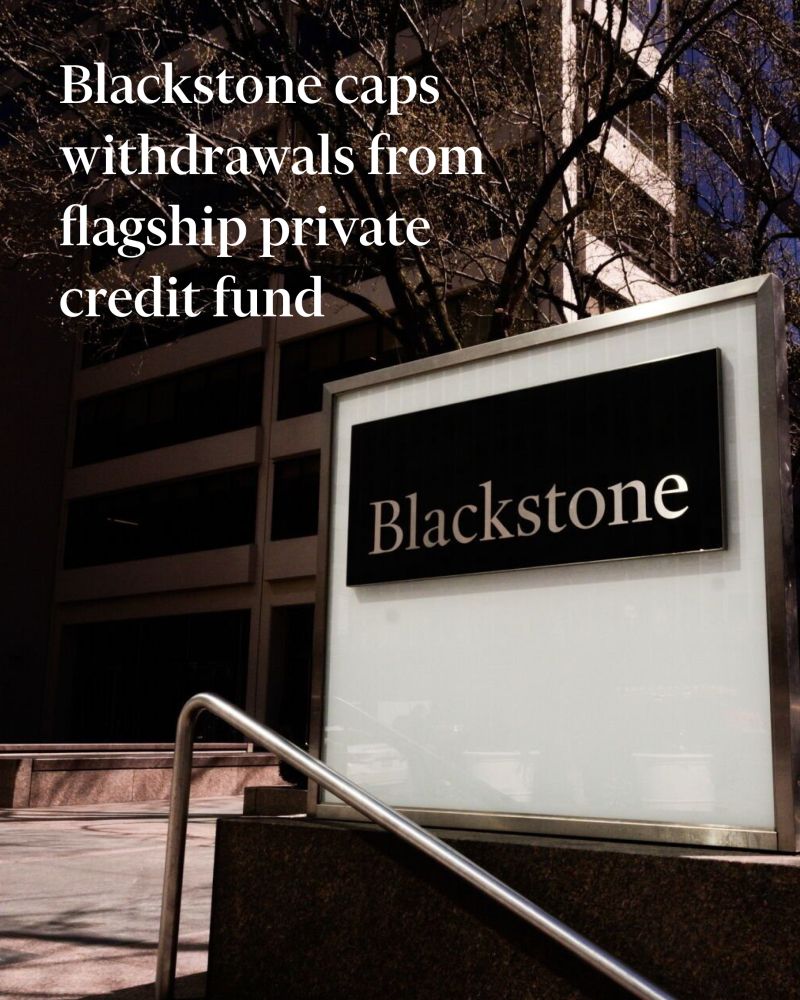

The world’s largest private investment group said investors in the $45bn Blackstone Private Credit Fund attempted to withdraw 10% of its net assets in the second quarter.

Source: FT

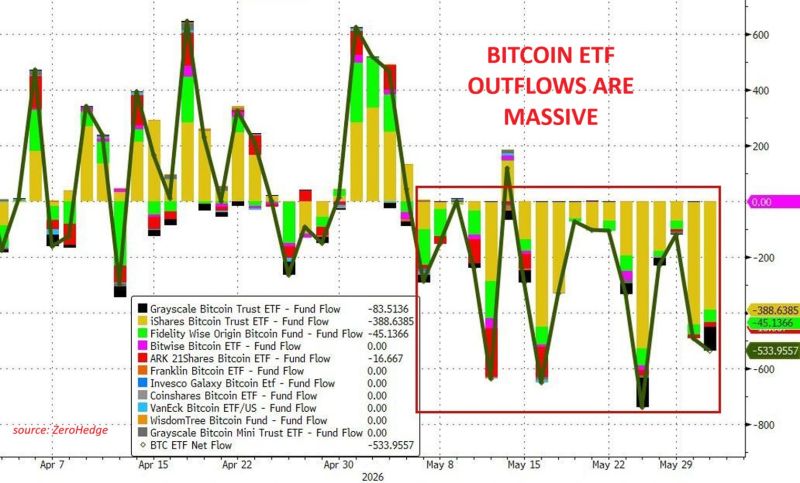

Crypto ETF outflows are MASSIVE

US Bitcoin ETFs posted net outflows of -$534 million in the most recent session, led by the ETF, $IBIT, at -$389 million. This extends a persistent trend of outflows over the last several weeks, with Bitcoin ETFs posting negative flows on the majority of trading days since early May. Overall, weekly crypto funds posted -$1.7 billion in outflows in the most recent week, in line with the highest weekly redemptions over the past year. In total, crypto funds saw over -$4 BILLION in outflows in just 3 weeks. Crypto market sentiment is deteriorating fast. Source: zerohedge, global markets investor

marvel $MRVL is up 245% since Nvidia announced a $2 billion investment on March 31 and has added $224 billion to its market cap in just 66 days.

Just 3 days ago Jensen Huang said "This is the next trillion dollar company." Since that single sentence, MRVL is up another 65%. At $278 billion today, Marvell needs to 3.6x from here to reach $1 trillion. Source: Bull Theory

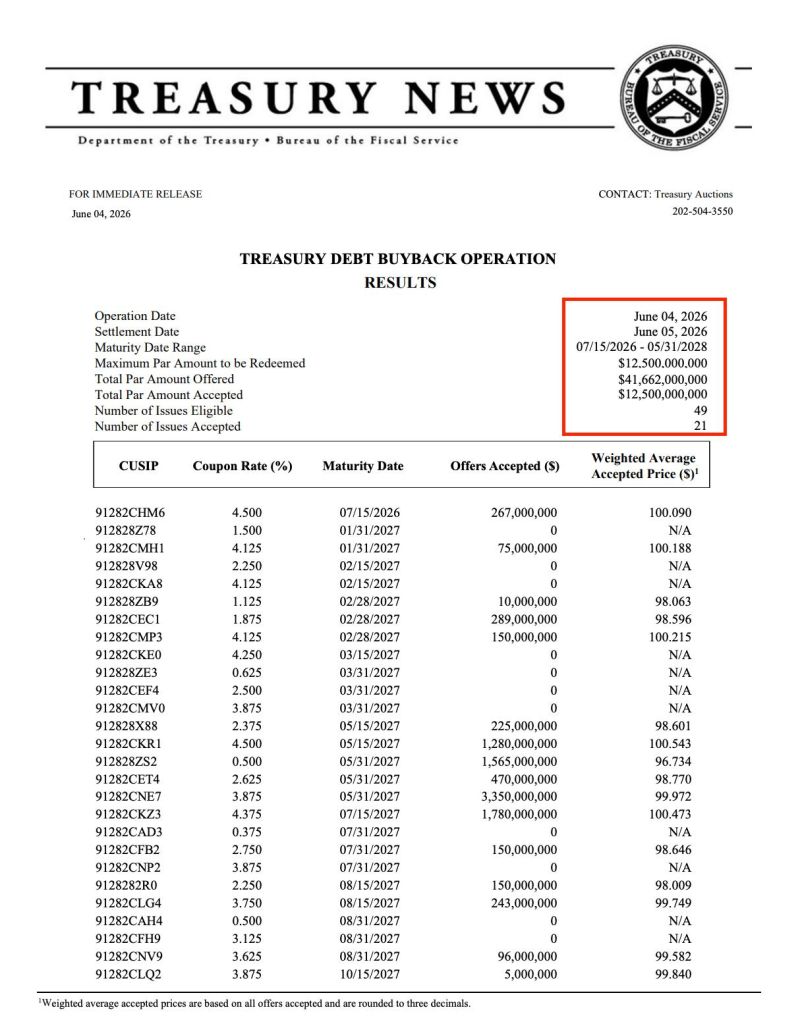

The US Treasury just bought back $12,500,000,000 of its own debt to improve liquidity.

Source: Bull Theory

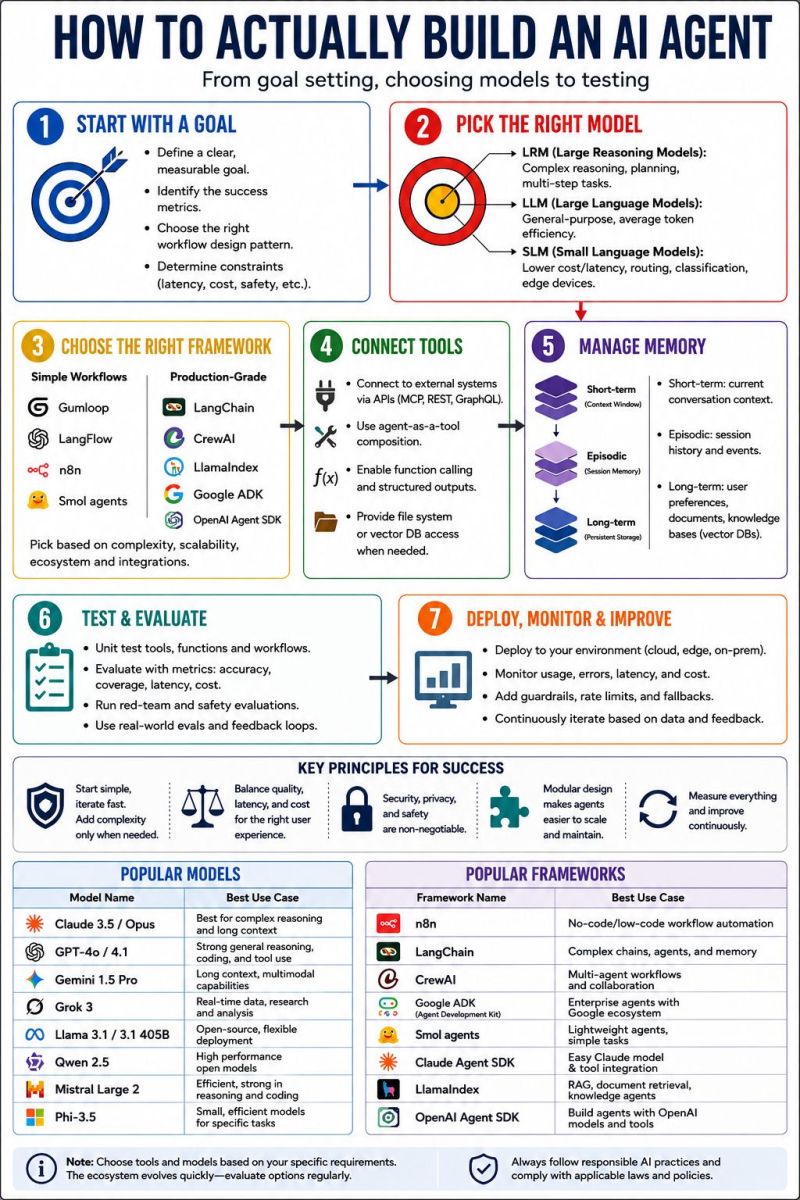

How to Actually Build an AI Agent (That Works in Production)

Source: Bekalu Tamene

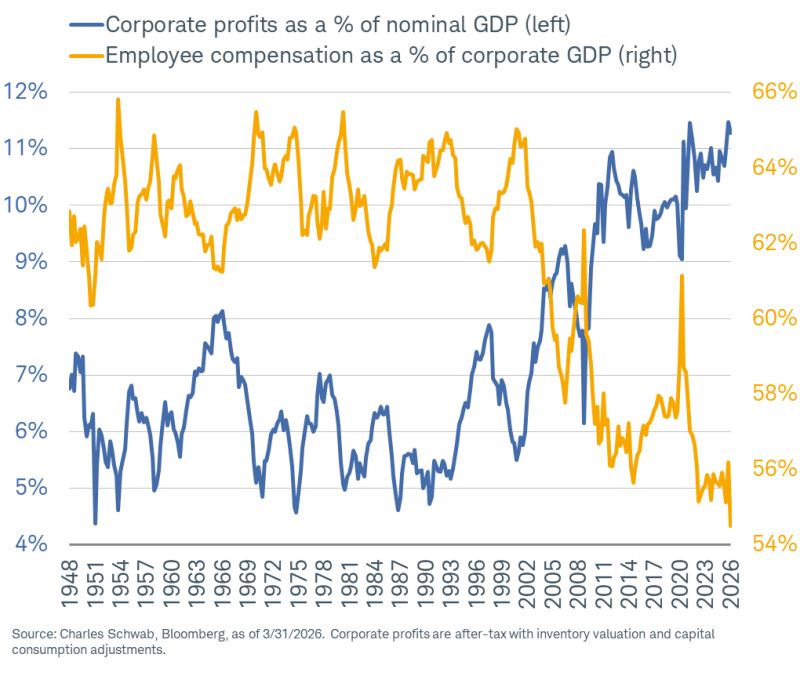

The K-shape economy

Corporate profits as a % of nominal GDP: right near an all-time high Employee compensation as a % of corporate GDP: all-time low Source: Kevin Gordon

Vanguard S&P 500 $VOO becomes the first $1 trillion ETF in history

Source: Hedgeye, Bloomberg