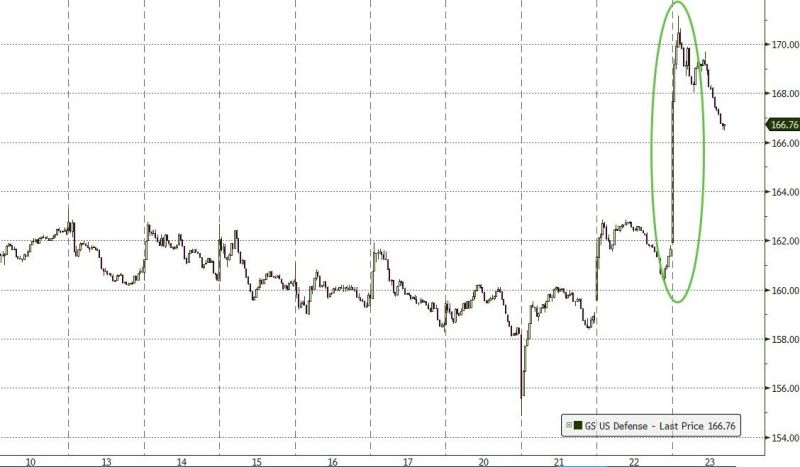

Look who is back... GS defense spending basket has been surging over the last few days on Middle East escalation...

Source: Bloomberg

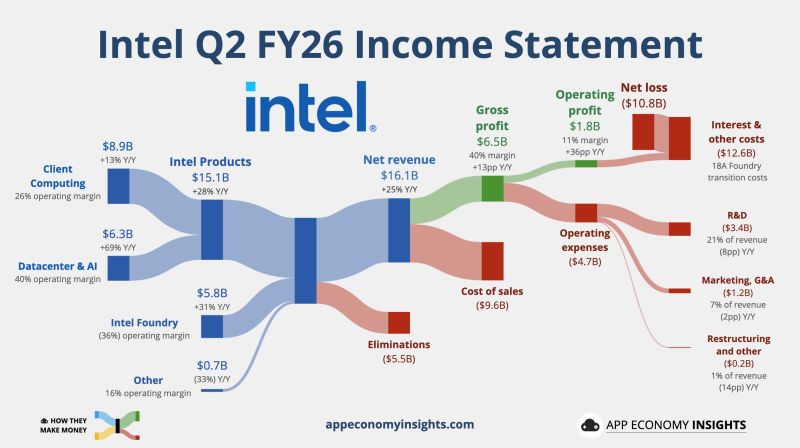

Intel reported better-than-expected second-quarter results on Thursday

Notching its fastest revenue growth rate for any quarter since 2011 and issuing guidance that topped expectations. The stock rose about 4% in extended trading. Intel shares are up over 170% so far in 2026 as of Thursday’s close after soaring 84% last year, when the U.S. government took a 10% stake in the company as part of an effort to support U.S. chip manufacturing. However, the stock has been in a slump more recently, dropping 28% in July. $INTC Intel Q2 FY26: • Revenue +25% Y/Y to $16.1B ($1.7B beat). • Non-GAAP EPS $0.42 ($0.20 beat). Q3 FY26 Guidance: • Revenue ~$15.8-16.8B ($1.2B beat). • Non-GAAP EPS $0.38 ($0.10 beat). Source: App Economy Insights, CNBC

The narrative of 'punish the spenders

(the hyperscalers - in red below) and celebrate the receivers' (the semiconductors - in green below) is still ongoing. Source: zerohedge

Alphabet $GOOGL closed below its 200-day moving average for the first time in over a year

Source: Barchart

President Trump told Axios on Thursday that he's seriously considering restarting major combat operations in Iran

Including strikes that would be bigger than the ones carried out during Operation Epic Fury. In a brief interview, Trump acknowledged that such a decision would have consequences and stressed he hasn't made a determination yet. Trump didn't give a deadline for his decision. Two other U.S. officials confirmed no call has been made and no new orders have been given to the military. The current escalation has caused oil prices to eclipse $100 per barrel. A return to all-out war is highly unpopular in the U.S. "I am considering a massive attack. Bigger than ever before. I am close to making a decision. We are all set for it," the president said. Trump said Israel "would join in two minutes if I ask them to," but added that "we don't need anybody" to launch a new operation against Iran. He also said there would be "consequences" for Israel joining the strikes, hinting at Iranian retaliation against Israel. Source: Axios

Carnage in hyperscaler bond land:

Investment Grade bond spreads for hyperscalers are exploding every day, as credit investors refuse to fund memory chip purchases any longer. CDS (inverted in red on the chart below) are following. How long will it take for the hyperscaler stocks (in blue) to follow ? Source: zerohedge

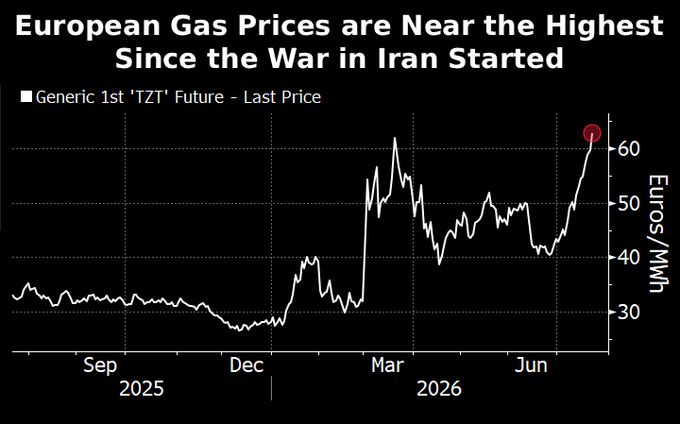

European gas futures are back near their highest level since the Iran war started

The reason: Europe is losing the LNG bidding war. Imports down 35% y/y over the last month; China's up 8%. TTF is back near its post-Iran-war high — not because Europe wants more gas, but because it has to pay up to get any. The cargoes aren't disappearing, they're just sailing east. US exporters are indifferent to which. Source: Jack Prandelli on X, Bloomberg

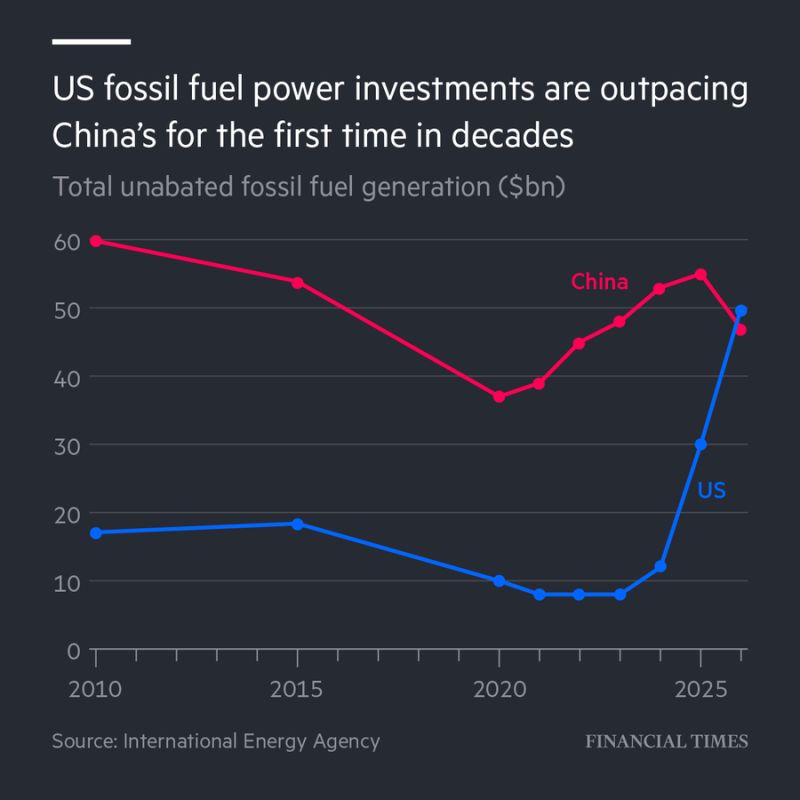

U.S. fossil fuel power investment is now outpacing China's for the first time in decades

Source: Hedgeye, FT, IEA