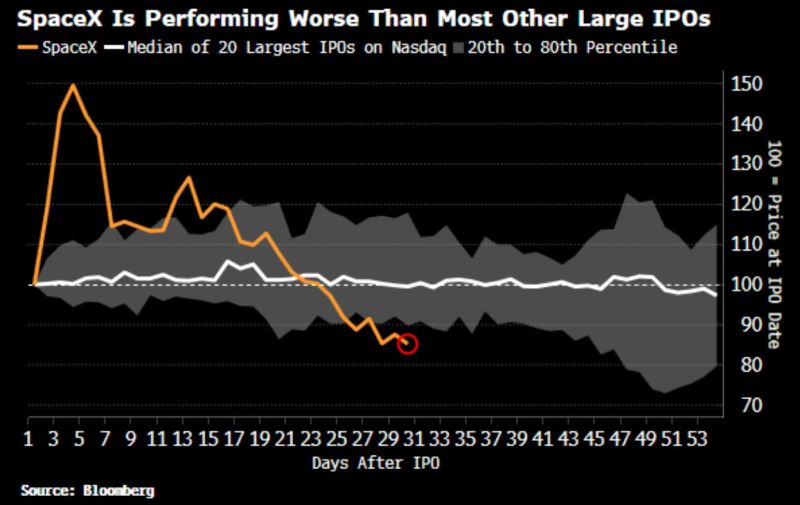

SpaceX, $SPCX, is down -50% from its peak.

Source: Hedgeye

Narrative violation. WSJ yesterday.

Source: David Sacks

Fed will deliver surprise rate hike this week, says Citadel

Source: Barchart

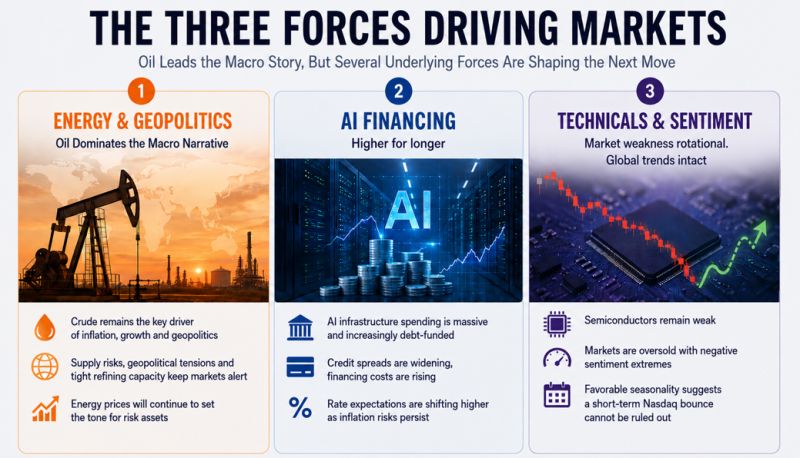

The three forces driving the market

Oil continues to dominate the macro narrative, but beneath the surface several other themes are gaining importance. AI financing is becoming a growing concern for credit markets, rate expectations are shifting higher, technicals across semiconductors continue to weaken, while an oversold setup and favorable seasonality suggest a short-term bounce in Nasdaq cannot be ruled out. Source: TME

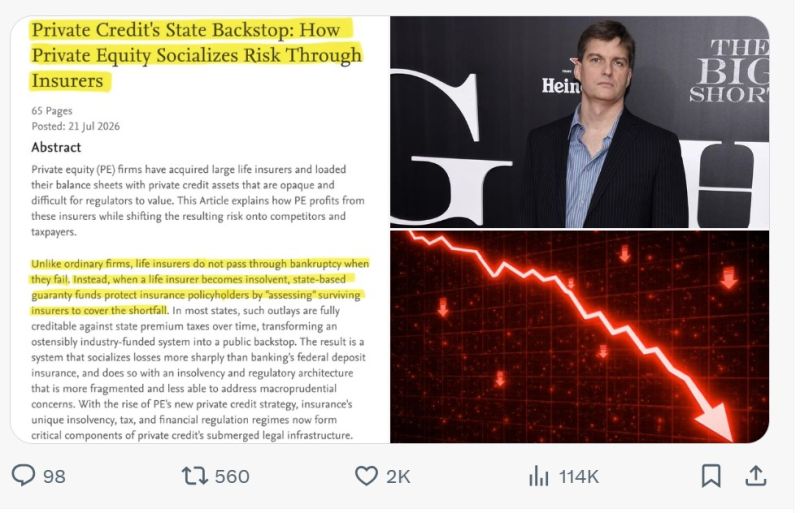

Michael Burry is warning that private equity may have found a way to shift losses onto the public.

Apollo, KKR and Blackstone have acquired life insurers and loaded them with $849 billion of hard-to-value private credit, more than double the 2014 level. If an insurer fails, state guaranty systems protect policyholders. The cost is initially borne by other insurers, but they can offset those payments against state taxes, ultimately reducing public tax revenue. The risk is no longer theoretical. Bankruptcies such as First Brands and Tricolor exposed valuation problems in private credit. Burry argues AI could be the next test, as data centre financing increasingly relies on similar opaque debt structures. If those investments disappoint, the losses may extend well beyond Big Tech and into the insurance system that ultimately protects millions of policyholders. Source: Bull Theory

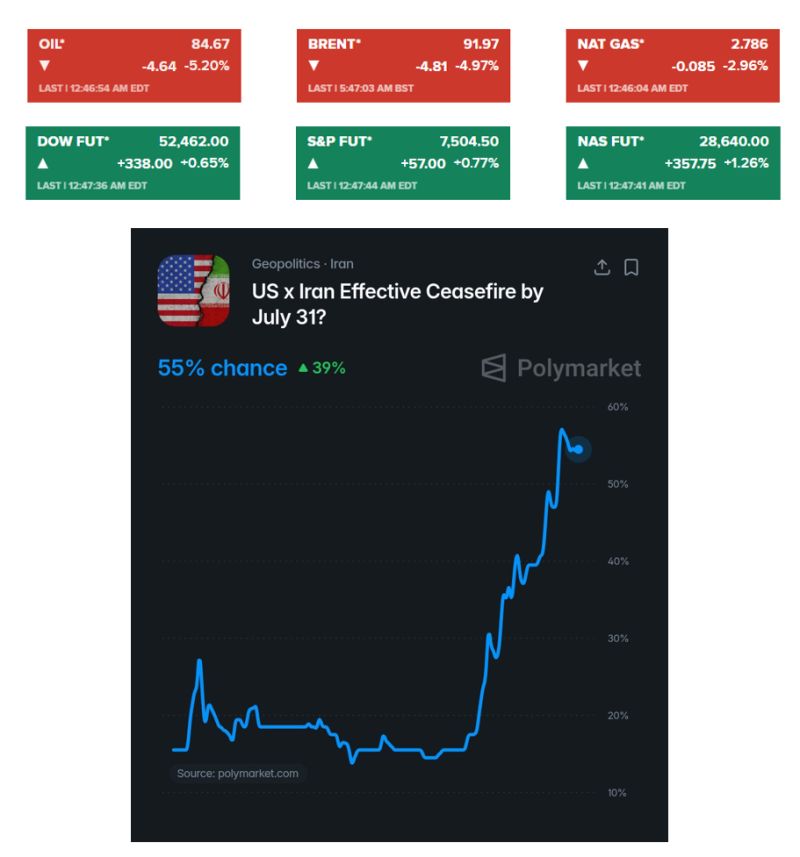

Oil slides 5% and US stocks indices futures jump as Iran reportedly signals halt to attacks if U.S. pause holds.

Iran has indicated it will stop carrying out attacks as long as the U.S. also refrains from striking, Reuters reported. There is now a 55% chance that the United States 🇺🇸 and Iran 🇮🇷 will sign a ceasefire this month, according to Polymarket traders Source: Evan, CNBC

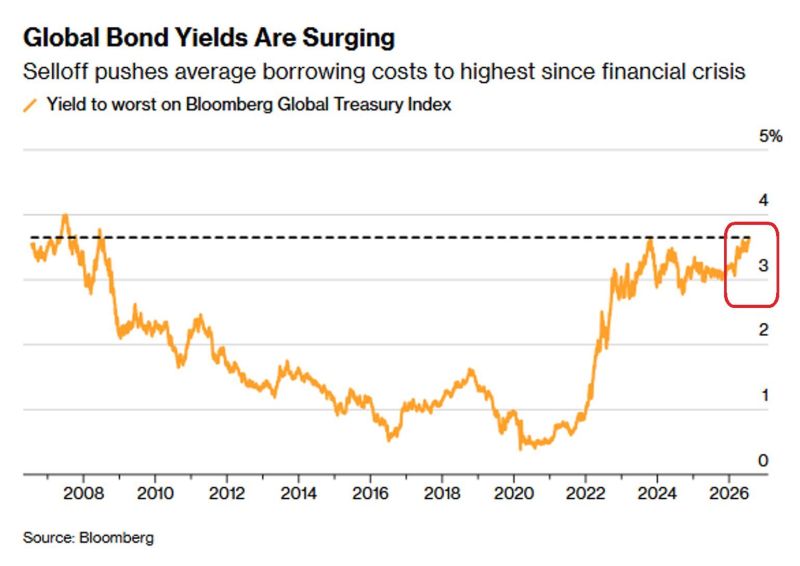

Global bond yields hit highest level since 2008

Source: Hedgeye, Bloomberg

WSJ: "Nvidia $NVDA is in talks to provide a roughly $250 billion backstop for OpenAI as part of a massive data-center project

It is one of the most ambitious financial transactions yet in America’s artificial-intelligence boom The guarantees from Nvidia would help the ChatGPT maker lease a 10-gigawatt project that SoftBank’s energy subsidiary is developing in southern Ohio, people familiar with the matter said. In total, the project could cost more than $500 billion, including the chips that would go inside the data centers. It would be the largest data-center project announced to date".