Warsh Senate Hearing — Key takeaways 👇

➡️ "Regime change" at the Fed: new inflation framework, revised communications, possibly fewer FOMC meetings per year. ➡️ Independence: vowed not to be Trump's "sock puppet," but declined to defend Governor Cook; said political comments on rates don't threaten Fed independence. ➡️ Dovish pivot: argues AI-driven productivity gains justify rate cuts despite 3.3% CPI. ➡️ Balance sheet is the key lever: accelerate QT, offset with lower short rates — implies a steeper curve. Confirmation at risk: Sen. Tillis (R-NC) blocking until DOJ drops Powell investigation; no clear path without him. Market read: mildly hawkish tone on the day — 10Y +4bps to 4.29%, equities turned negative intraday (but the fact that JD Vance to Pakistan for a second attempt at peace negotiations with Iran has been put on hold also explains bond yields rise and stocks pullback...) Note that prediction markets put only a 33% chance that Kevin Warsh is confirmed as Federal Reserve chair by May 15, when Jerome Powell’s term ends, according to Polymarket and Kalshi. Source: *Walter Bloomberg

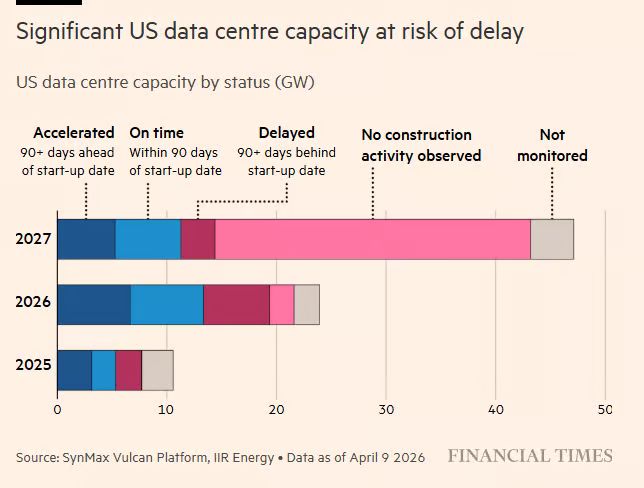

The US data center buildout is falling behind schedule:

Nearly 40% of US data center projects due to complete in 2026 are AT RISK of missing their deadlines by more than 3 months, according to SynMax satellite analysis and IIR Energy data. More than 60% of projects scheduled for 2027 have yet to begin construction as of April 2026. The 2027 pipeline alone represents ~50 gigawatts of planned capacity, equivalent to the output of ~50 nuclear reactors, with the majority still showing no construction activity, according to SynMax Vulcan Platform and IIR Energy. The primary constraints are chronic shortages of specialist labor, gas turbines, and transformers, along with permitting hurdles that are pushing labor costs up as much as +30% in remote locations. Is the US data center 'boom' hitting the wall? Source: Global Markets Investor, FT

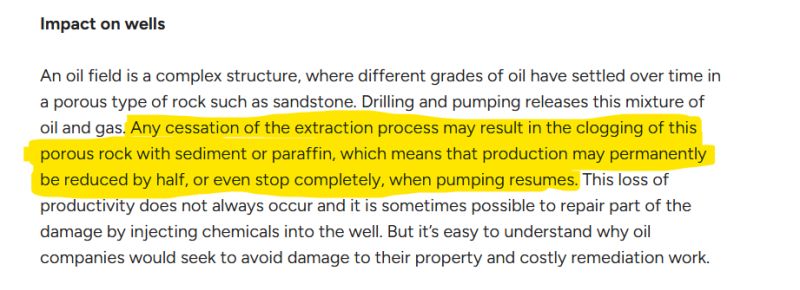

Part of US strategy: Iran is running out of storage for oil. Once they stop pumping, it can damage oil field production capacity.

You can't just flip the on/off switch on oil wells. If you stop, clogging happens. This can cause massive reduction in the amount of oil you get out of that oil well, requiring expensive and time consuming rework. Source: Wall Street Mav

Treasury Secretary Bessent has outlined a stark economic strategy: storage at Kharg Island is expected to reach capacity within days, potentially forcing Iran to halt oil production.

He describes the campaign as “Economic Fury,” warning that any individual or vessel involved in these shipments could face U.S. sanctions. This marks one of the most aggressive economic threats in the conflict so far. Unlike flipping a switch, shutting down oil wells is a complex process. Restarting them can take months and cost billions—and in some cases, production never fully returns. In essence, Bessent is signaling a strategy aimed at inflicting long-term damage to Iran’s oil infrastructure without the use of military force.

Don Tzu has dropped another quote.

Source: TT3

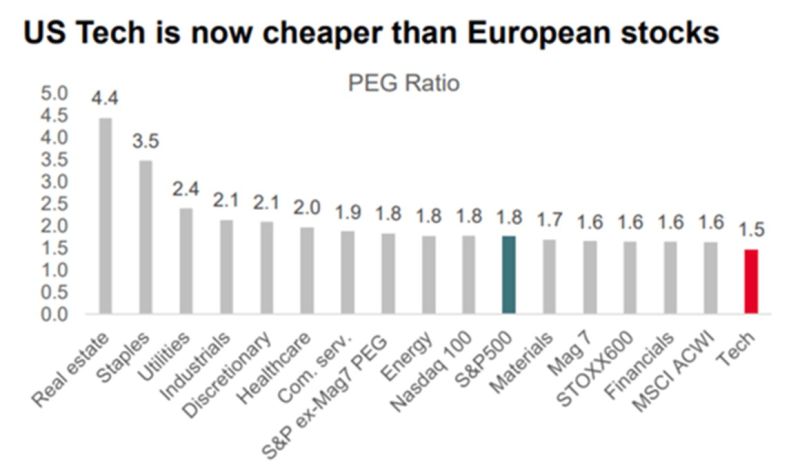

SocGen notes that Tech has one of the lowest PEGs..

Source. SocGen

Avis Budget Group ($CAR) could experience another extreme short squeeze similar to 2021, when the stock surged 722% in 41 days before collapsing 54% in a week.

Fast forward to 2026 and $CAR - Avis Budget - is up 656% in a month!!! The US government shut down. Airport security workers stopped getting paid. Thousands quit. 4-hour queues. Passengers abandoned flights. Road trips surged. Add a massive short squeeze and you get a 600% move. So what's going on? ---------- In 2021, the surge was driven not by fundamentals but by market positioning. At the time, Avis was heavily shorted because many investors viewed it as weaker than Hertz—citing valuation concerns, exposure to used car price volatility, and a less attractive balance sheet. Meanwhile, a popular hedge fund strategy involved a pair trade: long Hertz (fresh out of bankruptcy with an EV narrative) and short Avis. This created a crowded short position. The situation reversed when Avis delivered a strong earnings surprise and broader industry news (including Hertz-related developments) disrupted expectations. As the stock price rose, short sellers faced mounting losses, margin pressure, and forced liquidations. Since closing a short requires buying the stock, this triggered a feedback loop: rising prices forced more short covering, which pushed prices even higher. This self-reinforcing cycle—not fundamentals—drove the explosive rally. Once most shorts had exited and buying pressure faded, the stock rapidly collapsed. Today’s conditions—crowded positioning, limited float, and market structure—mirror that setup. If similar dynamics unfold, prices could again detach from fundamentals and rise sharply due to forced buying rather than intrinsic value. Source: Bull Theory

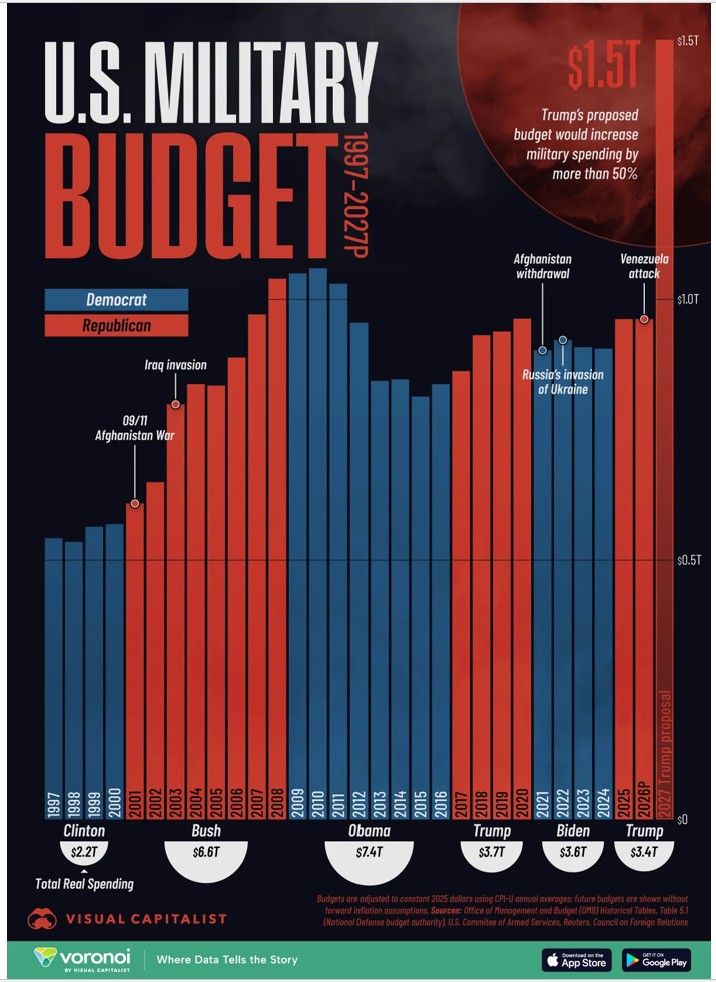

The Pentagon just proposed the largest defense budget in U.S. history at $1.5T or +42% in one year.

• $65.8T (warships & support ships) - Largest shipbuilding program since Kennedy. • $54.6T (autonomous warfare) • $6.1T (next-gen B-21 bomber) • 85 F-35 jets • 18 battle force ships • 16 non-battle force ships • Golden Dome missile defense • 12 critical munitions restocked • critical minerals supply chain investment Record drone investment. 44,000 new troops. The Iran war costs are not included. That’s a separate bill. America is no longer preparing for a war. It’s preparing for wars (with a "s")👁️ Source: Visual capitalist, Voronoi