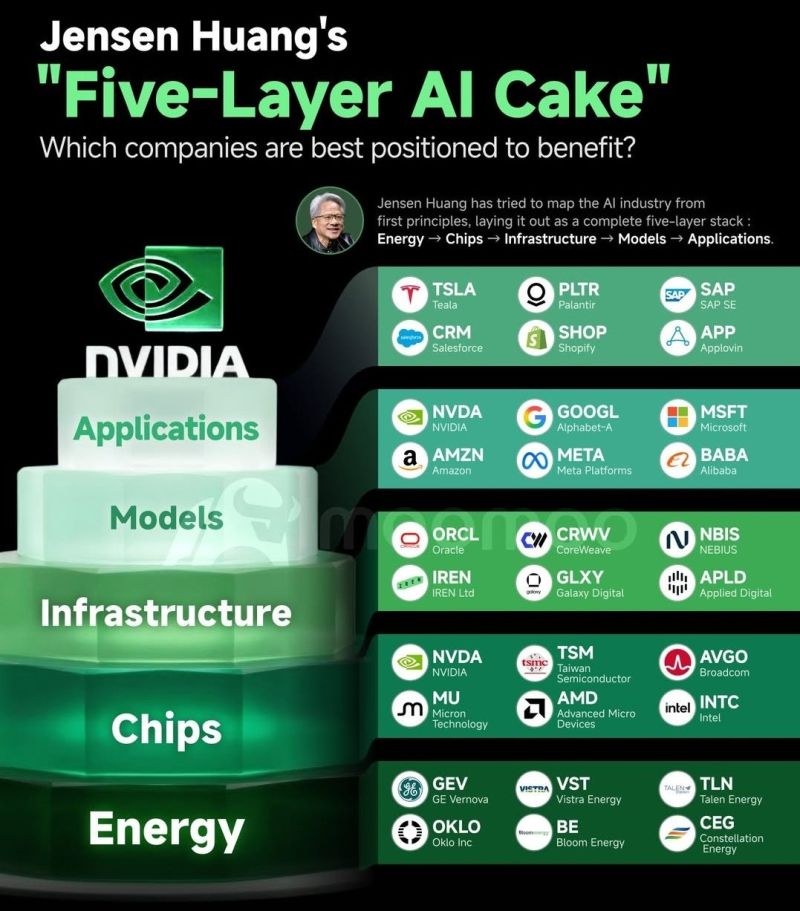

Jensen Huang shared a simple framework for understanding the entire Al economy the "Five-Layer Al Cake."

His message is clear: Al is no longer just software. It's becoming foundational infrastructure, similar to electricity or the internet. The 5 Layers of the Al Economy 1) Energy - The Power Behind Al Al requires massive electricity to run data centers and train models. This is why nuclear, renewable energy, and power infrastructure are becoming critical to the Al race. 2) Chips - Turning Power Into Compute Al chips convert electricity into computing power. Leaders like NVIDIA, TSMC, and Broadcom. dominate this layer with GPUs, advanced semiconductors, and high-bandwidth memory. 3) Infrastructure - The Al Factories Massive GPU clusters and cloud data centers coordinate tens of thousands of chips to "produce intelligence." Neo-Cloud leaders like Oracle, Nebius, Coreweave and Iren are building the backbone of Al compute. 4) Models - The Al Brain Large models process data and generate intelligence across language, science, robotics, and simulations. Competition is intensifying between companies like Meta, Microsoft, Amazon and Alphabet. 5) Applications - Where Value Is Created The top layer is where Al transforms industries: autonomous driving, Al agents, robotics, enterprise software, and more.

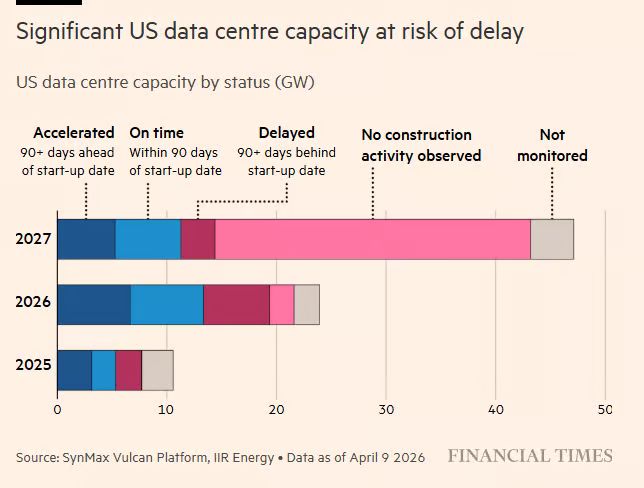

The US data center buildout is falling behind schedule:

Nearly 40% of US data center projects due to complete in 2026 are AT RISK of missing their deadlines by more than 3 months, according to SynMax satellite analysis and IIR Energy data. More than 60% of projects scheduled for 2027 have yet to begin construction as of April 2026. The 2027 pipeline alone represents ~50 gigawatts of planned capacity, equivalent to the output of ~50 nuclear reactors, with the majority still showing no construction activity, according to SynMax Vulcan Platform and IIR Energy. The primary constraints are chronic shortages of specialist labor, gas turbines, and transformers, along with permitting hurdles that are pushing labor costs up as much as +30% in remote locations. Is the US data center 'boom' hitting the wall? Source: Global Markets Investor, FT

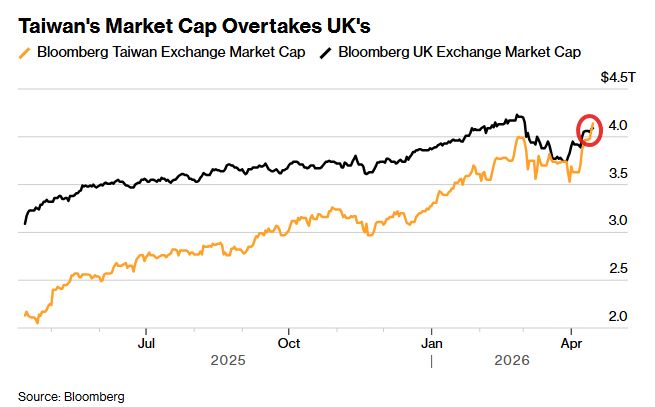

The power of the AI trade...

While Taiwan’s $977 billion economy is less than a quarter of the UK’s $4.3 trillion, last week Taiwan overtook the UK in stock market capitalization at $4.14 trillion, making it the world’s seventh largest, according to data compiled by Bloomberg showing the combined value of companies with a primary listing on the island. The UK’s market was valued at around $4.09 trillion. Source: Bloomberg, Neil Sethi

Looking for a "Anthropic proxy"?

It seems that SK Telecom ($SKM) offers stronger exposure to Anthropic than Zoom ($ZM) due to a larger and more valuable stake. SKM owns ~1.07% versus ZM’s ~0.6%, making its holding worth about $8.6B vs. $4.8B at an $800B valuation. As a result, Anthropic represents a much bigger portion of SKM’s valuation. Investors effectively get more Anthropic exposure per share with SKM, while its core business appears undervalued. Despite recent gains, SKM is still seen as a better proxy for Anthropic ahead of a potential IPO. Source: Negligible Capital

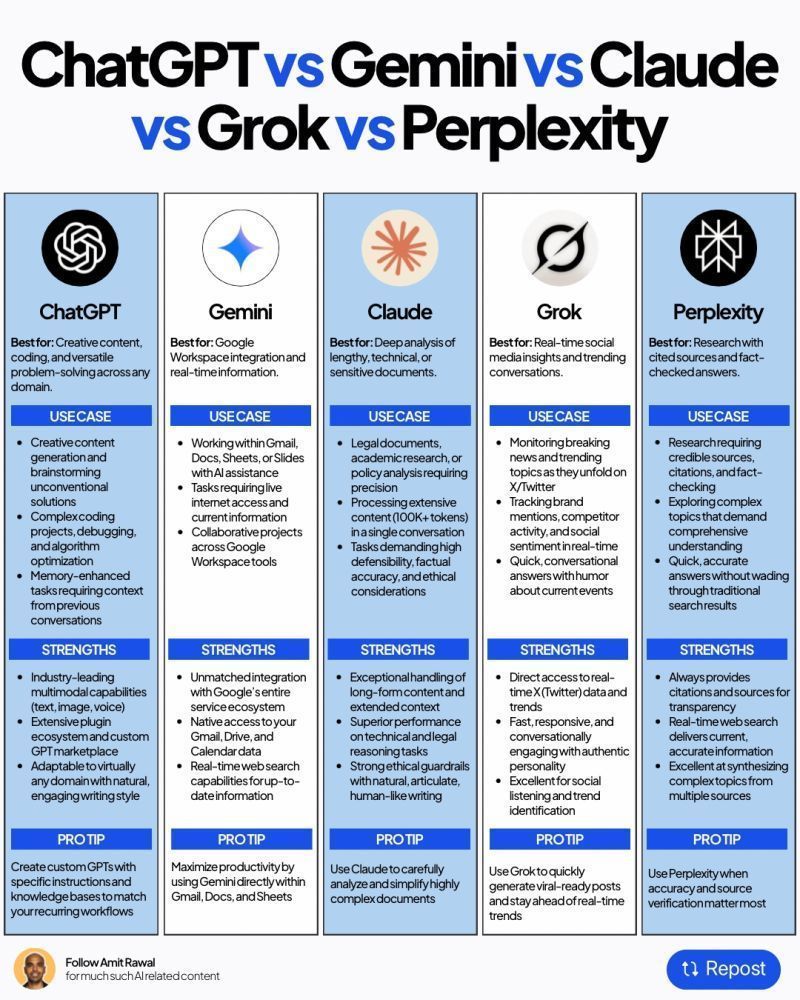

ChatGPT vs Gemini vs Claude vs Grok vs DeepSeek.

Everyone’s asking, “Which one’s the best?” Truth is: there’s no single winner. Each AI has its own lane. Source: AI Evolution

Anthropic is receiving investment offers at an $800B valuation according to Business Insider.

This means Anthropic and OpenAI might be at near equal valuations now. Crazy how fast Anthropic has scaled enterprise versus OpenAI. $SKM should fly on this. $800B is over 2x where they last raised, which was at a $380B valuation. Source: Bloomberg, Negligible Capital

From the FT: OpenAI investors question $852bn valuation as strategy shifts

OpenAI’s $852bn valuation is facing scrutiny as it shifts strategy toward enterprise AI, competing with Anthropic while maintaining ChatGPT’s consumer lead. Some investors worry the company is unfocused and vulnerable, especially as Anthropic’s rapid revenue growth challenges its position. The Claude-maker’s annualised revenue surged from $9bn at the end of 2025 to $30bn at the end of March, driven by demand for its coding tools. Anthropic’s business appears to have leapfrogged OpenAI, which hit $25bn in annualised revenue in February, though the companies use different accounting methods to book revenue, making direct comparison difficult. Despite raising $122bn and strong leadership confidence, OpenAI is cutting side projects and prioritizing higher-margin tools like Codex. It is also expanding infrastructure and workforce. However, strategic pivots, abandoned initiatives, and intensifying competition from Anthropic and Google raise concerns about execution and long-term valuation ahead of a potential IPO.

BESSENT SUMMONED WALL STREET CEOS TO DISCUSS ANTHROPIC’S MYTHOS

Claude Mythos is Anthropic's newest and most powerful AI model, announced just this week. It is described as "by far the most powerful AI model" Anthropic has ever developed — a step above even the Opus tier models, representing an entirely new tier of capability. Anthropic has deemed the model too dangerous for broad public release due to its extraordinary cybersecurity capabilities. It is currently only available to a select group of partners. Claude Mythos is apparently so good that Bessent and J. Powell summoned the bulge bank CEOs in a meeting to make sure they’re aware of how good Claude Mythos really is. Execs summoned include include $C Jane Fraser, $MS Ted Pick, $BAC Brian Moynihan, $WFC Charlie Scharf, and $GS David Solomon. Jamie Dimon $JPM couldn’t make it. More specifically, the meeting was about Mythos’s offensive and defensive cyber capabilities. Source: Negligible Capital