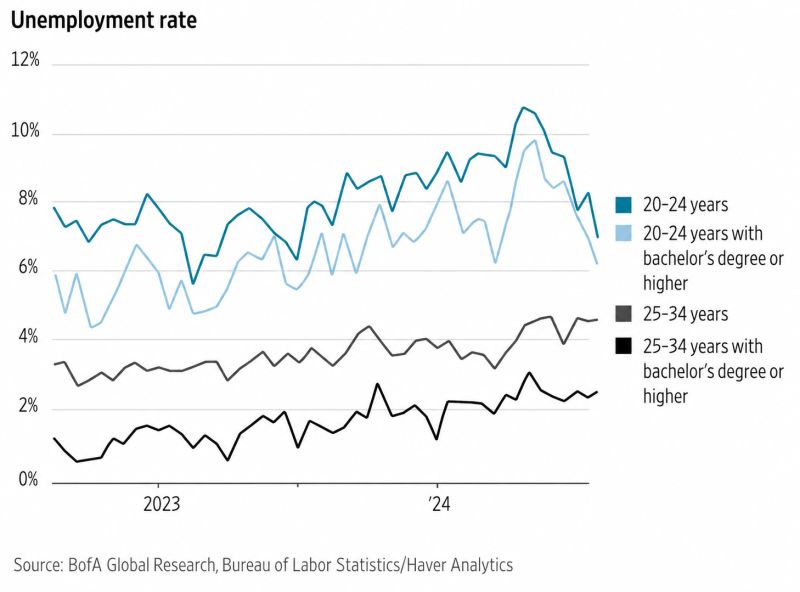

Young talents, don't believe all the negative headlines of AI killing jobs for graduates. Unemployment rate for 20-24 years in the US is actually plummeting...

Source: BofA

Yesterday was all about the OpenAi missed targets story. OpenAi ecosystem has underperformed the Google AI ecosystem (-45%) aggressively since the end of January.

Source: RBC, Bloomberg

{kind=link}

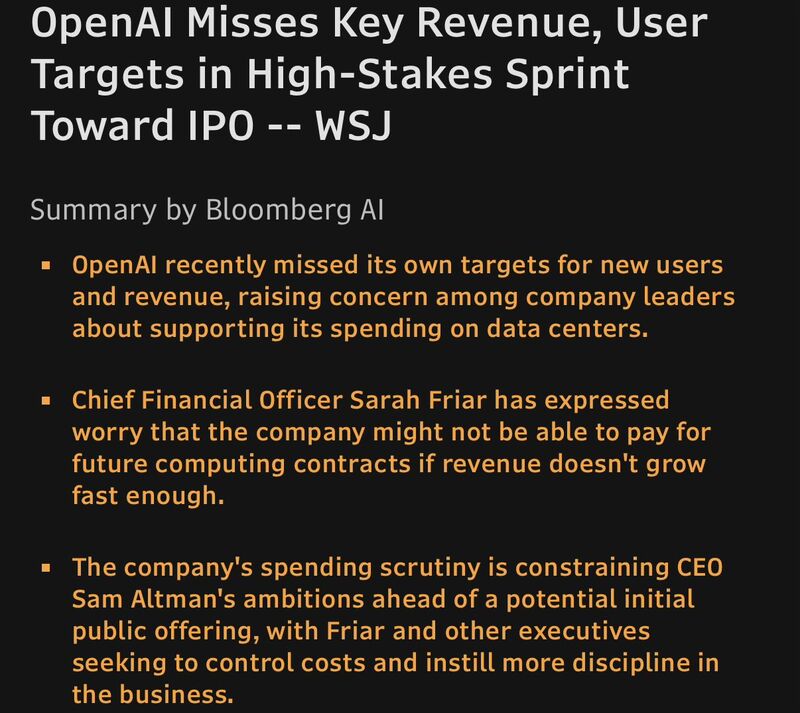

OPENAI MISSED '25 REV TARGET FOR CHATGPT: WSJ

Wow. OpenAI not only missed their 2025 revenue target, but they also missed their goal of reaching 1B weekly active users according to WSJ CFO Sarah Friar also reportedly told company leaders that she’s worried the company won’t be able to meet their spending commitments if revenue doesn’t grow faster. “OpenAI missed an internal goal of reaching one billion weekly active users for ChatGPT by the end of last year, according to people familiar with the goals. The company still hasn't announced that milestone, unnerving some investors. It also missed its yearly revenue target for ChatGPT as well after Google's Gemini saw massive growth late last year and ate into OpenAI's market share, the people said. The company has also struggled with defection rates among subscribers, according to people familiar with those figures.” Source: Bloomberg, Negligible Capital, WSJ, B,oomberg

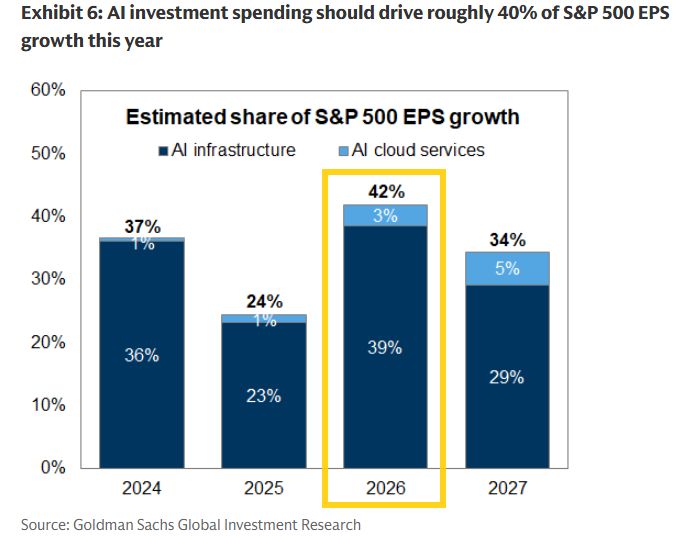

Goldman: We estimate that AI investment will drive roughly 40% of S&P 500 EPS growth this year, and just a few Tech stocks have driven the majority of recent index EPS revisions.

Our EPS forecasts this year and next are close to the top-down strategist consensus. Risks to our forecasts are two-sided, but AI skews those risks to the upside. Source: Neil Sethi

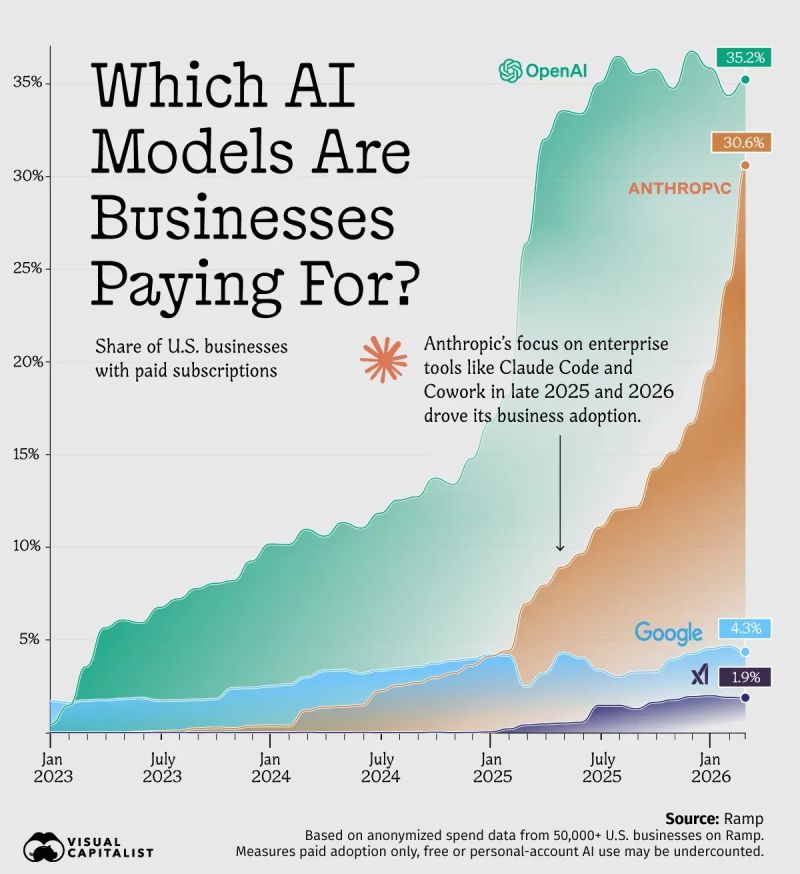

OpenAI has long been the leader for paid usage by U.S. businesses, but Anthropic has closed the gap with tools like Claude Code and Cowork 🤖

This graphic explores the share of U.S. businesses paying for AI models from different providers, with the data from Ramp. Source: Visual Capitalist

OPENAI AND MICROSOFT $MSFT JUST ANNOUNCED AN AMENDED PARTNERSHIP AGREEMENT

Here's what changes: ➡️ Microsoft will no longer pay a revenue share to OpenAI ➡️OpenAI can now serve its products to customers across any cloud provider ➡️Microsoft continues to participate in OpenAI's growth as a major shareholder and retains a license to OpenAI IP through 2032 ➡️Revenue share payments to Microsoft continue through 2030 Source Reuters / Evan on X

Meet the first clear casualty of AI disruption: Chegg.

Once a go-to platform for homework help and textbook rentals, it’s now in steep decline—its stock has collapsed nearly 99%, trading under $1 with a market cap around $100 million. Revenue has fallen dramatically from its 2022 peak, signaling a rapid unraveling of its core business. The shift is simple: tools like ChatGPT didn’t just compete with Chegg—they made it obsolete. When students can get instant, high-quality answers for free (or far less), the old model struggles to survive. This isn’t just one company’s story—it’s a turning point where AI disruption became real, fast, and unforgiving. So the real question is: who’s next?

TRILLION DOLLAR BABY...

OpenAI's pre-IPO valuation has officially hit a record $1 trillion. Pre-IPO instruments trading onchain, backed 1:1 by SPV exposure on Jupiter, are providing a real-time proxy for the company’s implied IPO valuation. OpenAI’s implied valuation is now up +163% since October 2025. This comes as Anthropic is also nearing a potential $1+ trillion IPO and SpaceX is reportedly targeting $1.7+ trillion. The world has never had this many trillion-dollar private companies... Source: The Kobeissi Letter