Was gold crash led by Hedge Funds?

Gold and silver prices are CRASHING: Gold is down -24% since its peak, erasing 2026 gains and falling back to December levels. Silver prices are down -47%, also down to mid-December levels. Both precious metal prices are approaching their 200-day moving averages. Massive liquidations across major assets continue. Meanwhile, a CFTC report shows hashtag#hedgefunds significantly increased their hashtag#gold hashtag#short positions, adding about $1.55–1.6 billion in new bets against gold. Around the same time, gold prices dropped sharply (from ~$4,520 to ~$4,100 in 72 hours), suggesting the selling pressure may be linked to this positioning. Hedge funds now hold a large total short position (~$23 billion), indicating strong bearish bets. Gold’s price drop may currently be driven less by fundamentals and more by positioning and coordinated behavior of large traders, meaning prices are being influenced by market pressure from leveraged players, not just underlying economic factors. Source: Wimar.X @DefiWimar

In the last 3 weeks, Gold is down -14%. Silver is down -28%. And yet… we have war, oil shocks, and extreme volatility. So what’s really going on?

This should be a perfect environment for precious metals to surge. But they’re falling. Here’s the truth most people are missing 👇 📉 Gold is NOT moving on fear (for now). It’s moving on global reserve flows. After 2022, when the US and Europe froze Russian reserves, something big changed: ➡️ Surplus countries stopped trusting Treasuries ➡️ They started buying gold instead Gold became a reserve asset of choice, not just a safe haven. 💥 Now comes the shock: The Strait of Hormuz blockade is crushing oil revenues. And that hits the exact countries that were buying gold: • Saudi Arabia • UAE • Kuwait Less oil revenue = less surplus Less surplus = less gold buying (or even selling) 🌏 The ripple effect doesn’t stop there: China — the world’s largest oil importer — is now facing slower growth. That means: ➡️ Smaller trade surpluses ➡️ Slower reserve accumulation ➡️ Less demand for gold ⚙️ And silver? It’s getting hit even harder. Why? Because ~50% of silver demand is industrial. So when global growth slows: ➡️ Demand drops ➡️ Prices fall faster than gold 🧠 The big takeaway: Gold isn’t reacting to fear right now. It’s reacting to global trade and capital flows. And those flows are weakening. 📌 The structural bull case for gold? Still intact. But in the short term… 👉 Gold follows liquidity and reserves 👉 Not headlines and fear Source: Global Markets Investor

Goldman team is coming out with higher for longer for oil prices even after the "all clear" sounds and SoH is reopened.

Source: Open Square Capital

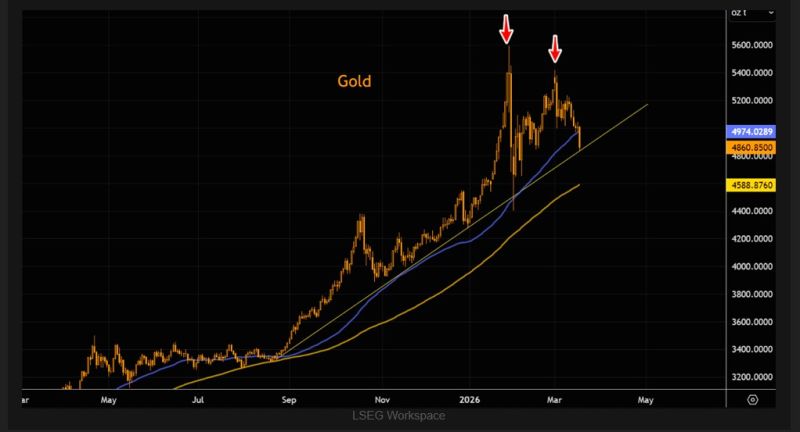

Gold is printing one of its largest down candles since the early-February

puke and breaking below the 50-day moving average, a level it hasn’t closed beneath since last summer. Key support comes in at $4800, with the 200-day moving average near $4600. Source: TME

Dr Copper ?

Source: Bloomberg

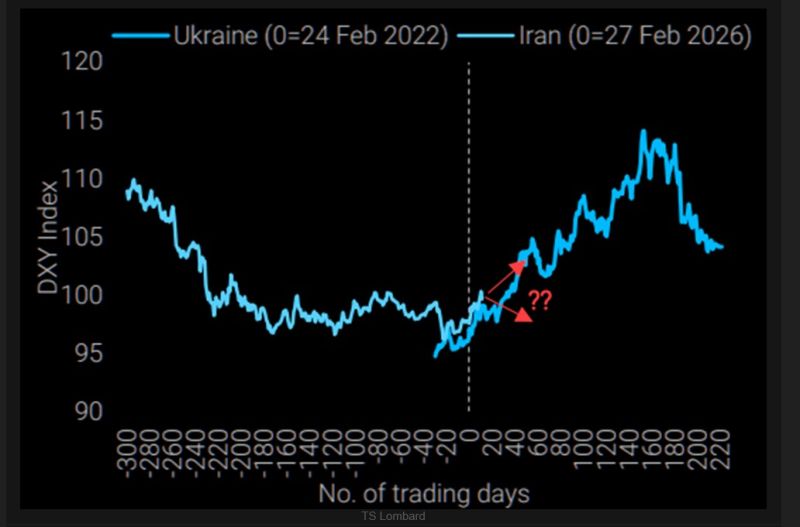

Dollar and the oil crisis

Last time it caught strong bids and squeezed for some 6 months. A similar move would tighten financial conditions quickly. Source. TS Lombard, TME

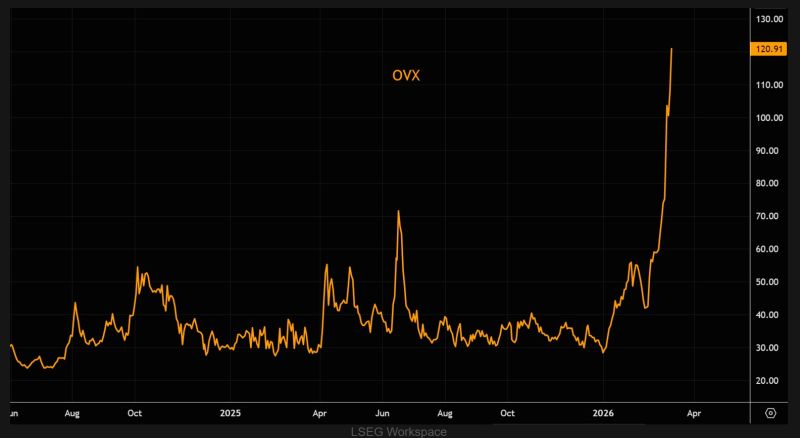

3 scenarios on Iran War by UBS

1. Quick de-escalation: Hormuz flows resume quickly; Brent averages ~$80 in March then mid-$70s, while TTF gas falls from ~€50 to high-€30s as inventories cushion short-term disruptions. 2. ~1-month Hormuz disruption: Markets tighten; Brent rises above $100 in March and TTF gas approaches €80, with faster inventory drawdowns and delayed normalization. 3. Extended disruption / infrastructure damage: Severe supply shock; Brent could reach $150+ by 2Q26 and TTF ~€80, creating a crisis similar to the 2022 European gas shock. ➡️ One thing is clear: OVX is not pricing the de-escalation scenario, closing at 121. Source. UBS, TME

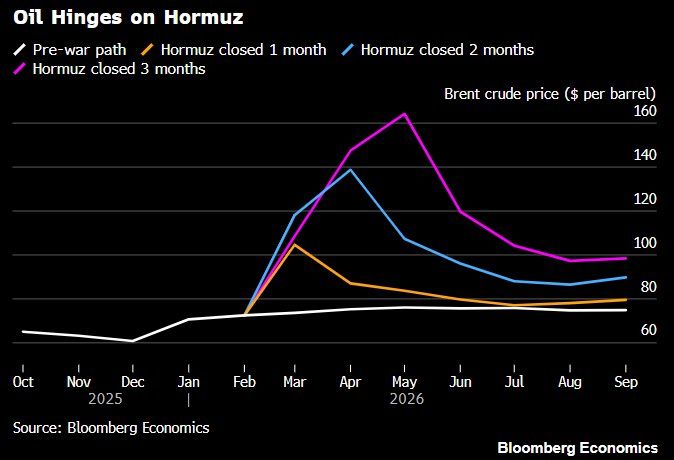

This is what Bloomberg thinks oil prices could be if the strait of Hormuz is shut for different time periods

1 month - ~$105 per barrel 2 months - ~$140 3 months - ~$165 Source: Evan Evan StockMKTNewz Bloomberg Economics