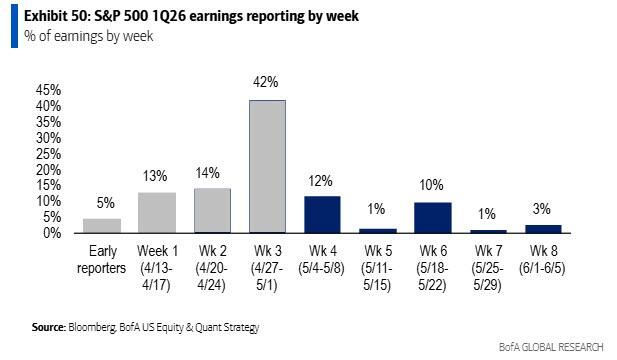

42% of the S&P 500 companies report earnings this week

Source: zerohedge, BofA

TESLA $TSLA JUST REPORTED EARNINGS

EPS of $0.41 beating expectations of $0.34 Revenue of $22.4B missing expectations of $22.64 Tesla says Cybercab, Tesla Semi and Megapack 3 are on schedule for volume production starting in 2026 Once in production, expect Cybercab to begin to replace existing Model Y fleet and will be largest volume vehicle in fleet over time Preparations for first large-scale Optimus factory will begin in Q2 Are expanding scope of manufacturing to include semiconductor fabrication in AI inference compute Source: Evan on X

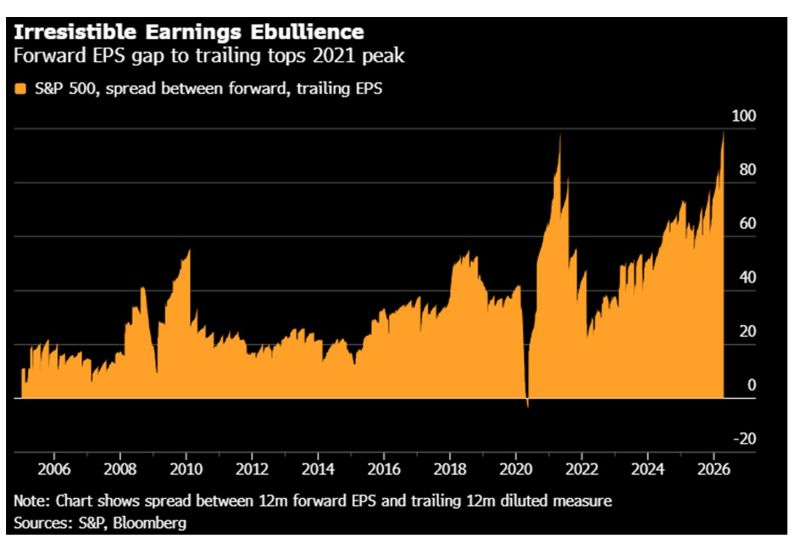

S&P 500 12 month forward earnings are going to the roof...

Below, an interesting Bloomberg chart showing the difference between forward 12 months EPS estimates and trailing 12 month EPS Source: Bloomberg

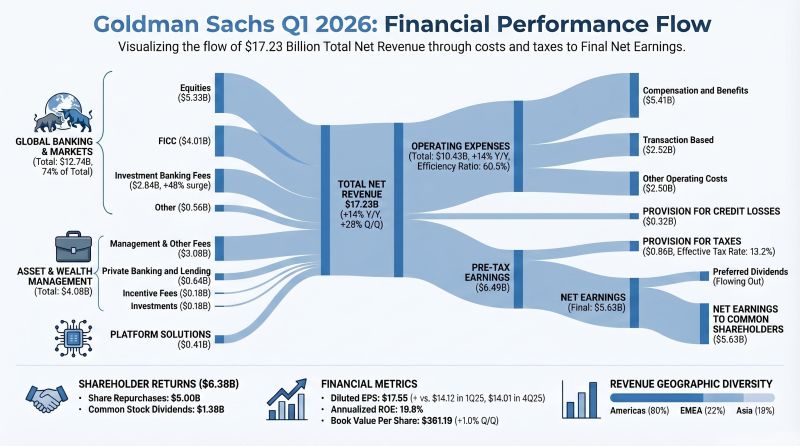

First US Banks Q1 earnings results are IN. Goldman Sachs $GS Delivers Massive Q1 2026 Beat!

GS just dropped its first-quarter results, and the numbers are impressive. With the stock currently moving 3.28%, here are the most important highlights you need to know: Net Revenues: $17.23 billion up 14% YoY and 28% vs. Q4 2025. Diluted EPS: $17.55, significantly outperforming last year's $14.12. Net Earnings: $5.63 billion for the quarter. Segment Performance: Global Banking & Markets: A powerhouse quarter with $12.74 billion in revenue (+19% YoY). Investment Banking Fees: Surged 48% to $2.84 billion, fueled by a major comeback in M&A Advisory. Equities: Jumped 27% to $5.33 billion, driven by record-level financing and intermediation. Asset & Wealth Management: Solid growth with $4.08 billion in revenue (+10% YoY). Source: Hataf Capital

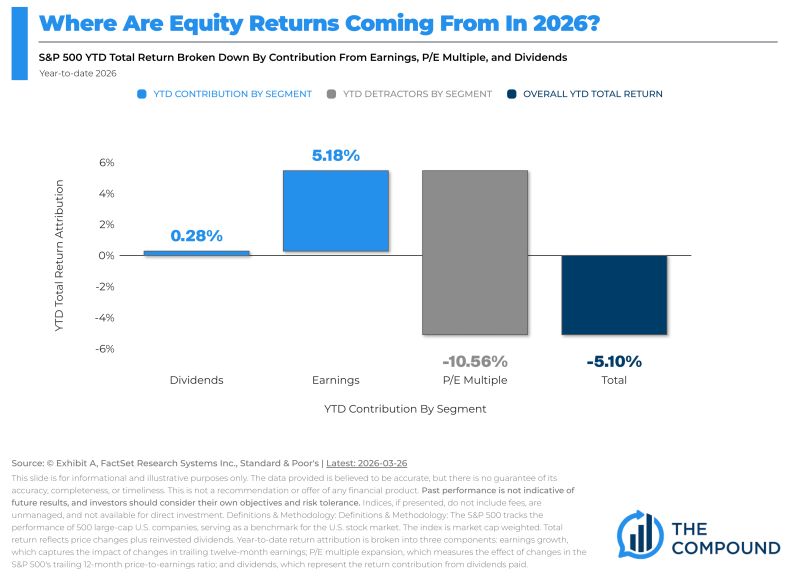

Strong earnings with multiple contraction. That’s 2026 in a nutshell.

Source: @mattcerminaro Daily Chartbook

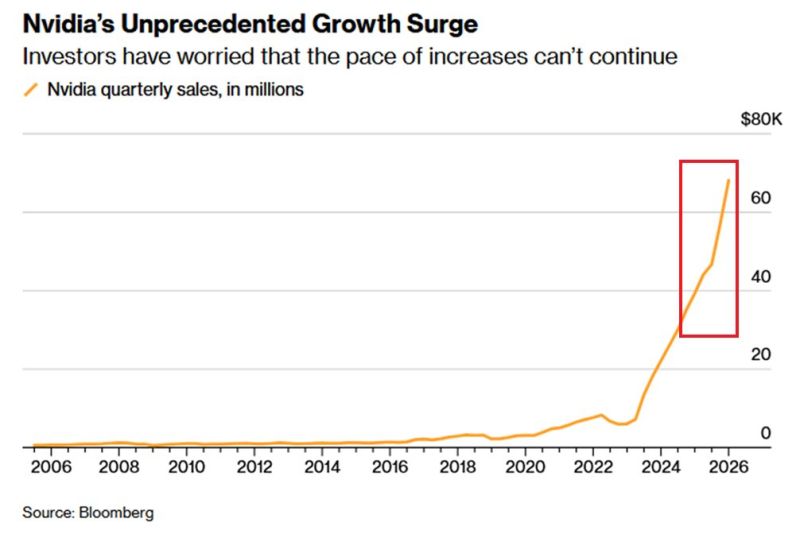

NVIDIA posted its best quarter ever

$68.1B revenue (+73% YoY) and Q1 guidance of ~$78B—but the stock fell, erasing post-earnings gains. CFO Colette Kress flagged potential long-term AI disruption from Chinese chipmakers. China exposure remains limited, with zero H200 chip sales and tariffs on U.S.-licensed shipments. The market reaction shows that when expectations are extremely high, even record results may disappoint. Source: Global Markets Investor, Bloomberg

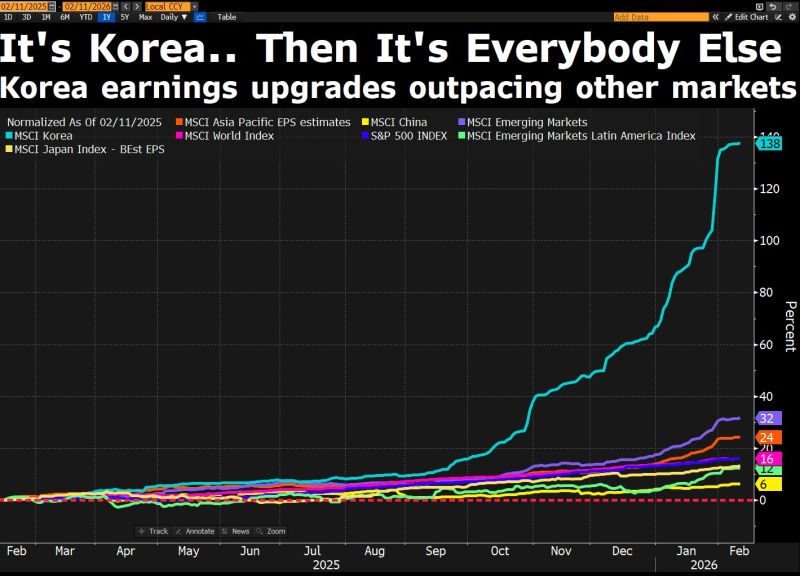

As far as the standout global earnings story is concerned, it's Korea... and then it's everybody else.

Source: David Ingles @DavidInglesTV

THE MASTER EARNINGS SEASON CALENDAR

Here are the most popular stocks that report earnings this week February 9th - February 13th. Source: Earnings Hub